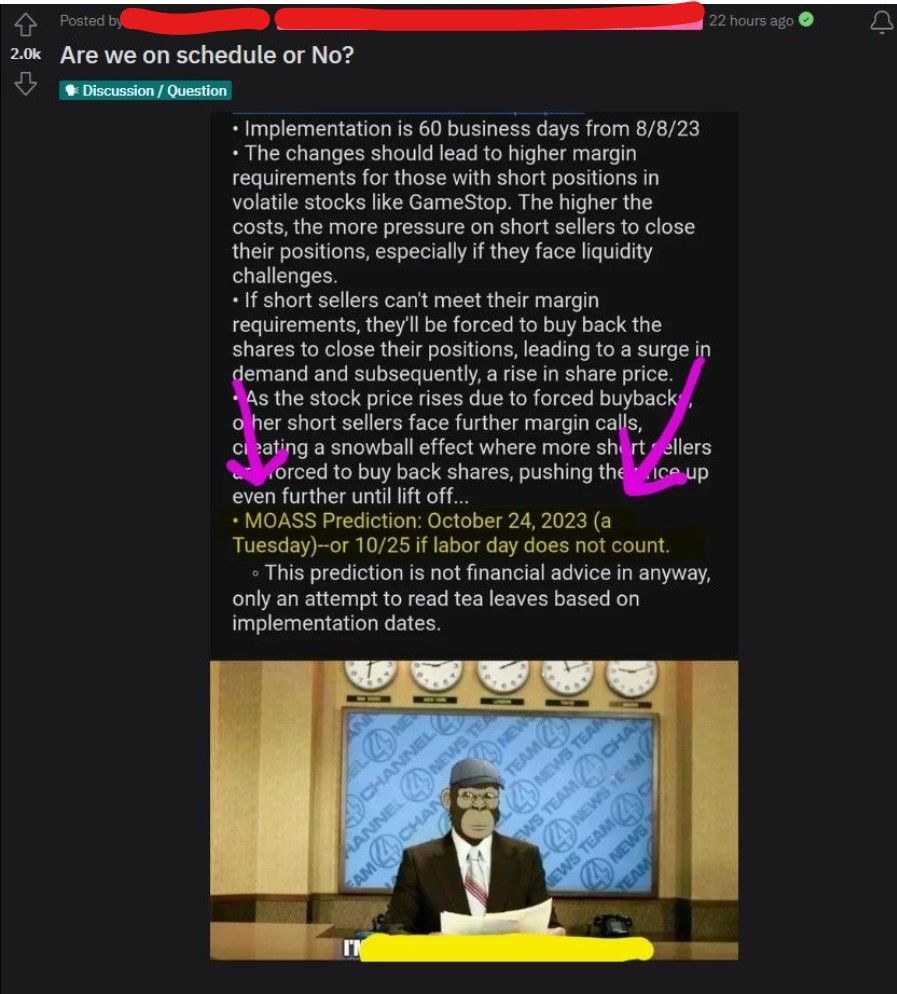

Are we on schedule or No? An update on my MOASS prediction heading into 10/24 and beyond.

I hope everyone enjoyed a wonderful and restorative weekend and that your Monday is off on the right foot!

When I first posted on this topic back in August, I thought it would probably die in 'new' as r/Superstonk does not usually appreciate anything that tries to tie any sort of date around MOASS, especially one predicated on any sort of rule changes.

If there were to be any follow up, I expected maybe needing to respond to some comments in the future. However, as the 24th has approached, comments, messages, and posts have started to ask for an update or how I am feeling about it. Talk about taking a life of its own--nuts in a fun way!

Before digging into the meat and potatoes of this post, I would like to set the table with an anecdote:

One crisp March night, while dutifully charting the skies, seeing further and clearer than you have before, you stumble upon an anomaly–a celestial body that doesn't fit the familiar patterns. While looking for it again a few days later you find it again but noticed it moved--how odd!

You note and record your observations, believing it to be a curious discovery, possibly a star, perhaps of interest to a select group of fellow astronomers and share your findings, engaging in scholarly discussions with peers.

Yet, as word spreads of this anomaly, so does the potential magnitude of its significance amongst the larger community. It might not be just another star or comet, but the Mother of all Scientific Serendipities (MOASS)--the discovery of the seventh planet (Uranus)!

Mercury, Venus, Mars, Jupiter and Saturn are all bright enough to be easily visible to the naked eye. In fact, since these planets have been known to people for millennia, this would arguably the first planet in recorded history to be ‘discovered’ at all.

You now understand and realize the enormity of your responsibility--you must share your reflecting telescope with the community and allow others to observe and confirm what you have seen for themselves.

It is critical for humanity that we expand our civilization to Uranus

— Ryan Cohen (@ryancohen) May 25, 2022

Seeing as Ryan Cohen brought up Uranus before, thought it would be fun to share the above about its discovery.

Why am I talking about the discovery of Uranus in a MOASS prediction post?

I feel I have a similar responsibility with my 'telescope' (the 10/24 prediction) and owe it to folks who are curious to provide an update and allow them to decide for themselves where things are when it comes to schedule.

Well, are we on schedule?

This is hard to say, as 'on schedule' will certainly mean something differently from person to person.

If you mean 'on schedule' in the sense that GameStop's share price on 10/24 is to the point in the Tendieman Song where folks are taking their gains and going, there is a 99.999% chance I am wrong on that, which I have tried to qualify along the way.

just a guess based on implementation of the new rules of what almost caused the whole thing to kick off 1/28/21.

What's a little good clean fun with a Tuesday night prediction, right?!?

🤞you (and everyone else) can see where I am coming from and this is not COMPLETELY out of left-field as a non-starter.

I hope this is the right blend of hopium mixed with just enough 'reality' to be plausible for this speculation/discussion and that I am not completely off my rocker.

However, if you mean 'on schedule' for MOASS in the sense that everything rules wise is is in place and set to interact with potential volatility triggering the unstoppable force (gamma ramp) meeting an immovable object (DRS'd shares) and MOASS?

I believe so.

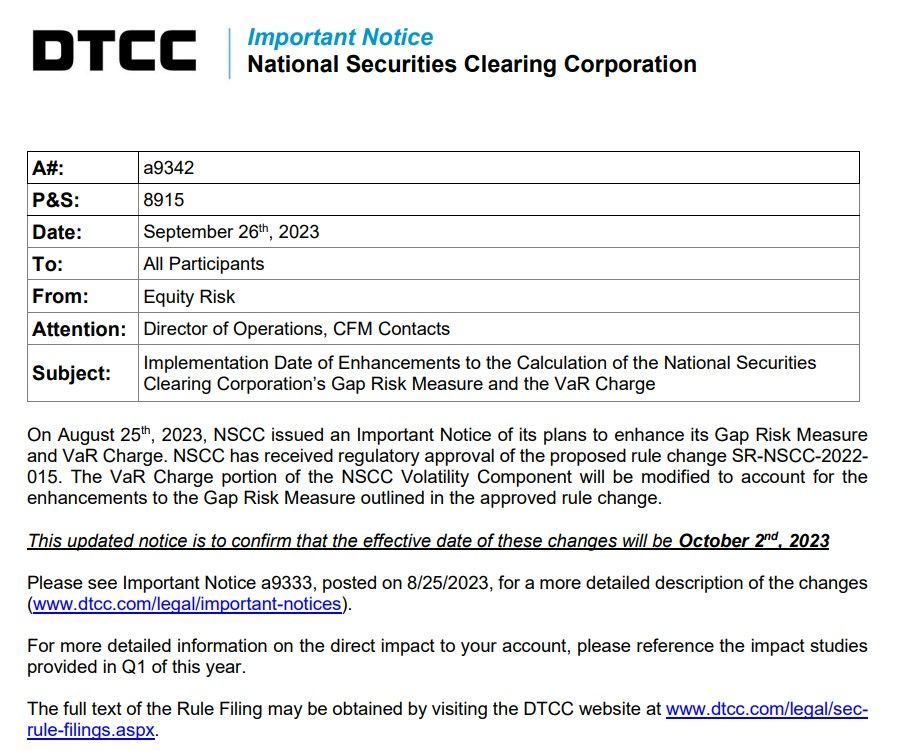

The VaR charge was pushed up in the implementation window (they could have waited until the 24th/25th but pushed it up to 10/2).

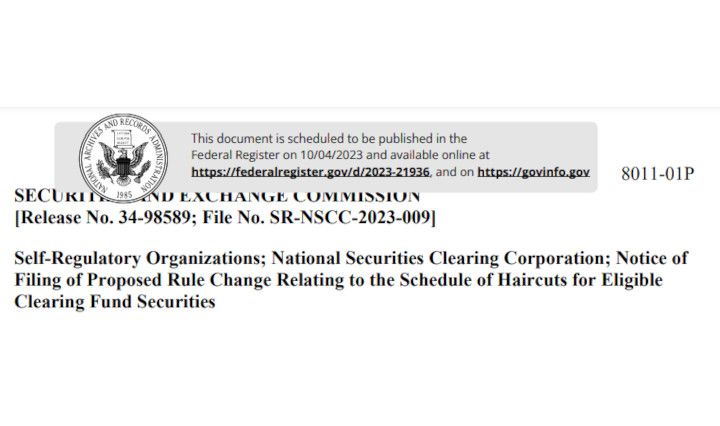

This post is about 'Haircuts' (called out in the VaR charge) that was published in the Federal Register 10/4, meaning within the next 60 business days (should before 12/22/23), it will be in effect as well.

I used this example previously and I think it is apt to use again--calling out the 24th was more akin to a tornado watch. Conditions are ripe for a storm, with the now implemented VaR soon getting 'teeth' in the form of revised haircuts.

Again, for 10/24, I am not trying to say 'MOASS' is that day but rather that conditions are ripe for it with all these changes--starting with 10/2 and VaR going into effect.

I will turn back to the rules further below but for now I would like to take a moment to review some events and statements since the prediction post back on August 8th.

Since August 8th we have also learned:

Options Clearing Corporation Order Approving Proposed Rule Change Concerning Collateral Haircuts and Standards for Clearing Banks and Letters of Credit

The OCC plans to modify its rules in three main ways concerning collateral management and banking relationships.

- Update the method for adjusting haircuts (reductions) to certain collateral types, shifting from the current method to a fixed schedule.

- Clearly define in the rules the minimum standards for banks involved in clearing and for those issuing letters of credit, aiming to provide more clarity on essential banking relationships for OCC's services.

- Allow OCC to set tighter limits for letters of credit than what's currently in the rules.

- Became effective 9/24/23

NSCC/OCC propose changes to keep NSCC netting for OCC

- The Clearing Agencies want to update the existing arrangement and related rules.

- Without NSCC, there's no netting, so Clearing Members would need to directly coordinate with each other for settlements.

- This update would permit OCC, in the event of a default by a Common Member (a firm part of both OCC and NSCC or one that designates an NSCC member to act for it), to make a cash payment to NSCC.

- Such a payment would guarantee NSCC oversees the settlement of that member's transactions.

- In 2022, netting through NSCC's CNS system decreased CNS settlement obligations by about 98%, turning $519 trillion to just $9 trillion.

- A historical study revealed that, in a worst-case scenario, OCC would need about $384.6 billion for gross broker-to-broker settlement.

- Section 14 of the Existing Accord would be modernized to provide that notices between the parties would be provided by e-mail rather than by hand, overnight delivery service or first-class mail.

Congressman French Hill on Treasury's previous $700 million bailout of Yellow: “I think the Treasury is undercollateralized. I’ll leave it at that” Treasury owns 15.94 million shares

- The loan was broken up into two tranches, with the $300 million tranche A dedicated to YRC’s “near-term contractual obligations and non-vehicle capital expenditures.”

- Tranche B provided “$400 million for capital investments made pursuant to capital plans subject to approval by Treasury,” the summary said, noting that both tranches mature on Sept. 30, 2024.

- As taxpayer compensation, the Treasury Department also received shares, equal to 29.6% of YRC’s common stock on a fully diluted basis, to be held in a voting trust. With its stake of 15.94 million shares, the U.S. Treasury is Yellow’s second-largest shareholder.

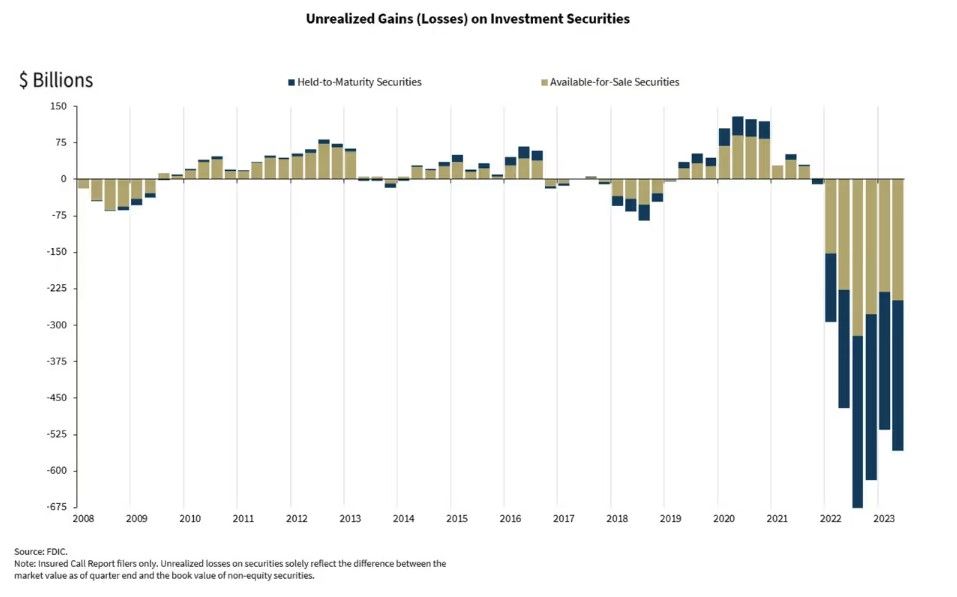

FDIC 2023 Risk Review: "Unrealized losses present a significant risk should banks need to sell investments & realize losses to meet liquidity needs."

- "Unrealized losses present a significant risk should banks need to sell investments & realize losses to meet liquidity needs."

- In Q1 2023, unrealized losses at $515.5 billion.

- "banking industry is increasingly exposed to the broad & varied risks from nonbank activities"

- High interest rates remain a significant source of liquidity risk for banks.

DTC is issuing debt to cover risk of member default

- "The proposed Debt Issuance would provide DTC with an additional source of default liquidity, which would allow it to diversify its sources of default liquidity and mitigate risks to DTC that it is unable to secure default liquidity resources in an amount necessary to meet its liquidity needs."

Silvergate Capital CEO Alan Lane to Exit as Crypto Bank Winds Down

- Citadel Securities is the owner of roughly 1.73 million shares or a 5.5% stake in Silvergate

An affiliate of Ken Griffin’s Citadel has acquired roughly $485 million in Yellow Corp. debt previously owned by Apollo Global Management Inc. & other senior lenders to the bankrupt trucking firm

- With its stake of 15.94 million shares, the U.S. Treasury is Yellow’s second-largest shareholder.

July FOMC: "Various participants commented on risks that could affect some banks, including unrealized losses on assets resulting from rising interest rates, significant reliance on uninsured deposits, and increased funding costs."

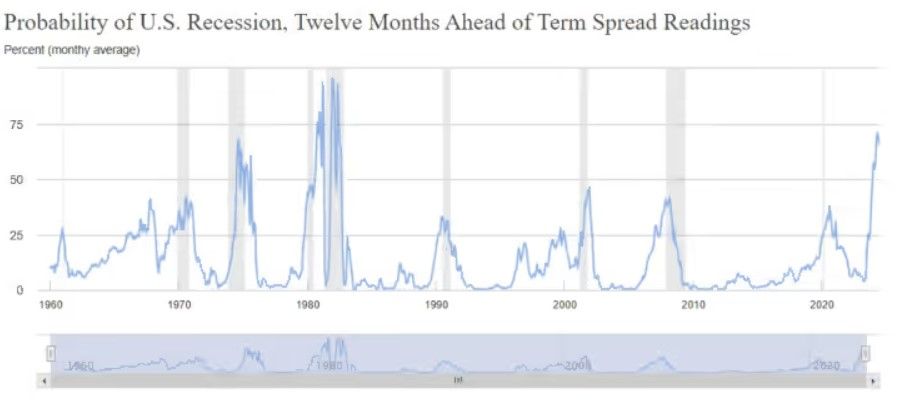

New York Fed Yield Curve as a Leading Indicator U.S. recession probability showing highest level since 1980's for May '24

- This model uses the slope of the yield curve, or “term spread,” to calculate the probability of a recession in the United States twelve months ahead.

- "The yield curve has predicted essentially every U.S. recession since 1950 with only one "false" signal, which preceded the credit crunch and slowdown in production in 1967."

"From the start of its Consolidated Audit Trail (CAT) reporting obligation on June 22, 2020, through the present, Instinet failed to timely and accurately report data for tens of billions of order events to the CAT."

- From the start of its Consolidated Audit Trail (CAT) reporting obligation on June 22, 2020, through the present, Instinet failed to timely and accurately report data for tens of billions of order events to the CAT.

- Instinet ignored warning signs of its CAT reporting issues.

- They knew about the problems in 2020 but only acted after FINRA expressed concerns in 2021.

- Even then, their attempts to rectify the issues were delayed and are STILL incomplete.

- Penalty? Censure & $3.8 million fine while not admitting wrong doing.

Fitch Ratings lowered the operating environment score for U.S. banks in June to ‘aa-‘ from ‘aa’

- 'Strong and resilient', huh?

- "The failure of three U.S. banks earlier this year brought into focus several vulnerabilities in the regulatory framework that failed to address significant asset/liability mismatches, deposit concentrations/outflow vulnerabilities and regulatory lapses, which our recent downgrade of the OE incorporates."

- "We expect a number of regulatory changes related to capital and liquidity requirements to be implemented. These changes are likely to be phased in over a number of years, which means these vulnerabilities will remain for some time."

- "Further action on the OE would be informed by the interplay between inflation, interest rates and implications from the Fed’s quantitative tightening (QT). This would ultimately influence bank fundamentals such as mix and cost of deposits, greater reliance on wholesale borrowing and lending capacity."

The Fed Brings Enforcement Action Against FTX-Linked Farmington State Bank, and its holding company, FBH Corporation

- Farmington State Bank and its holding company FBH Corp. received a cease-and-desist Thursday for violating commitments to state and federal regulators, by engaging in digital asset activity.

- Farmington and FBH will voluntary liquidate.

- Alameda, (the hedge fund arm of FTX) invested $11.5 million in Farmington and had a stake.

- Had just 3 employees until FTX investment.

China Evergrande collapse shows need for $1 trillion Beijing rescue plan, says Clocktower strategist

- Since mid-2021, companies accounting for 40% of Chinese home sales have defaulted, including Evergrande in late 2021, stoking fears about the resilience of the world’s second-largest economy.

- This analyst said China may need to absorb some $1 trillion in soured real-estate assets from the private sector, in a move similar to the Federal Reserve’s takeover of toxic mortgage and related derivatives off banks’ balance sheets in the wake of the 2007-2008 global financial crisis.

FINRA Names Bill St. Louis as New Head of Enforcement

- St. Louis will be responsible for the management of approximately 350 enforcement staff in 11 offices across the United States and will report directly to FINRA CEO Robert Cook.

- Steps into the ongoing Instinet enforcement matter...

SEC Adopts Amendments to Exemption that will enhance FINRA oversight

- The rule changes specify tighter exemptions and the REQUIREMENT of brokers or dealers to join a national securities association (should mean greater oversight, but it is FINRA...).

- Under current rules, proprietary trading firms that are solely members of an exchange are subject to less rigorous oversight and operate in a less transparent manner than firms that are current FINRA members and that are required to report their Treasury trades.

- These limited exemptions apply if a broker or dealer, without customer accounts and belonging to at least one exchange, conducts securities trades that:

- Stem solely from order routes by its member national securities exchange to meet regulatory order protection requirements.

- Are exclusively for completing the stock component of a stock-option order.

- Is effective 60 days after being published in the Federal Register.

- Gary Gensler stated "monthly trading volume valued in the hundreds of billions of dollars" has led to a "regulatory gap" these amendments aim to close this gap.

- Hester Peirce: "Because today’s recommendation rejects a common sense approach, I cannot support it."

- Mark Uyeda: "Given the lack of evidence supporting this mandatory extension of FINRA membership, coupled with the clear potential for the unintended negative consequence of a reduction in liquidity, I am unable to support it"

NY Fed Survey: Expected likelihood of becoming unemployed rises

- Wages on offers up over 14% since July 2022, Inflation fuel!

SEC Enhances the Regulation of Private Fund Advisers

- "The final rules will restrict certain other private fund adviser activity that is contrary to the public interest and the protection of investors."

- Will require private fund advisers registered with the Commission to provide investors with quarterly statements detailing certain information regarding fund fees, expenses, and performance.

- Will require a private fund adviser registered with the Commission to obtain and distribute to investors an annual financial statement audit of each private fund it advises and, in connection with an adviser-led secondary transaction, a fairness opinion or valuation opinion.

- Prohibit all private fund advisers from providing investors with preferential treatment regarding redemptions and information if such treatment would have a material, negative effect on other investors.

- Caroline Crenshaw: "I want to address the critique that the SEC should play no part in the negotiations between sophisticated investors. To me these arguments ring hollow."

- Mark Uyeda: "Today, the Commission seeks to impose rules for private funds – which are generally available only for sophisticated investors – that are far more burdensome and restrictive than those products for retail investors."

- Hester Peirce: "The rulemaking is ahistorical, unjustified, unlawful, impractical, confusing, and harmful. Accordingly, I cannot support it."

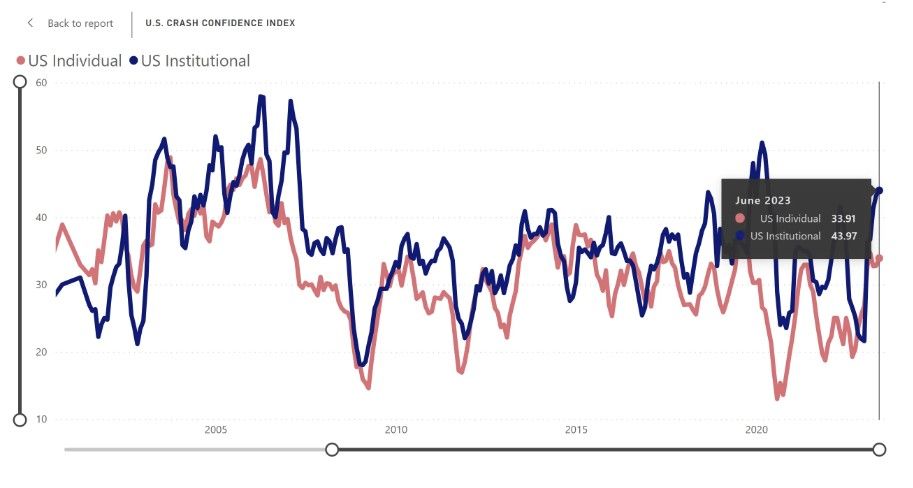

Yale University: 66.1% of retail investors and 56.03% of institutional investors believe the probability of a catastrophic stock market crash in the U. S., like that of October 28, 1929 or October 19, 1987, in the next six months is above 10%

Fed Chair Jerome Powell: "We have tightened policy significantly over the past year." "Inflation has moved down from its peak...it remains too high"

Credit Suisse posted $4 billion loss in second quarter, Sonntagszeitung reports, which cited insiders at the bank

Azher Abassi, the Federal Reserve’s Executive Vice President Supervision + Credit and head of bank supervision in San Francisco, which had oversight of Silicon Valley Bank and First Republic, will retire effective October 31st

- Guy who got thrown under the bus in report is now resigning effective October 31

- Azher Abassi, the Federal Reserve’s Executive Vice President Supervision + Credit and head of bank supervision in San Francisco, which had oversight of failed lender Silicon Valley Bank, will retire effective October 31st.

Abbasi will be succeeded by Niel Willardson

- Willardson, who was formerly a Minneapolis Fed official, started on Oct. 1.

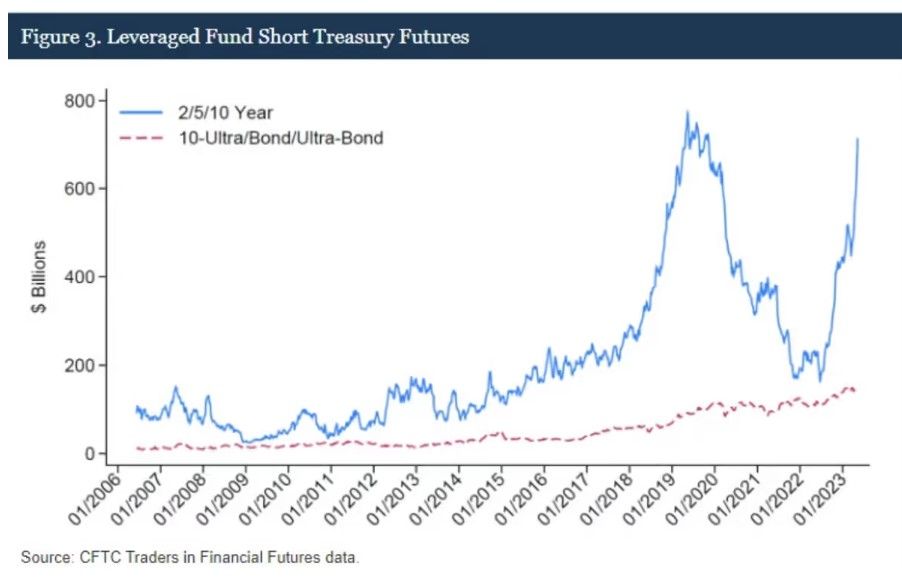

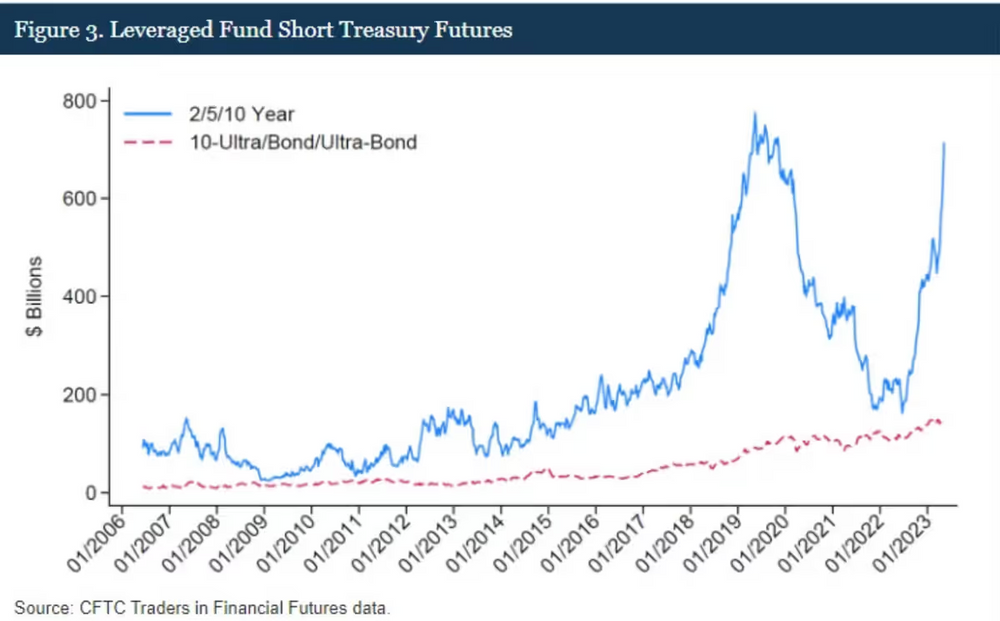

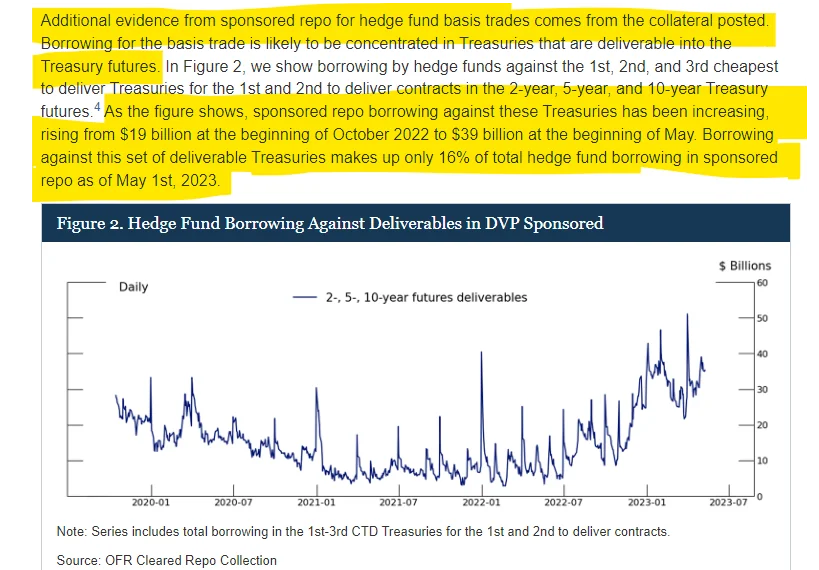

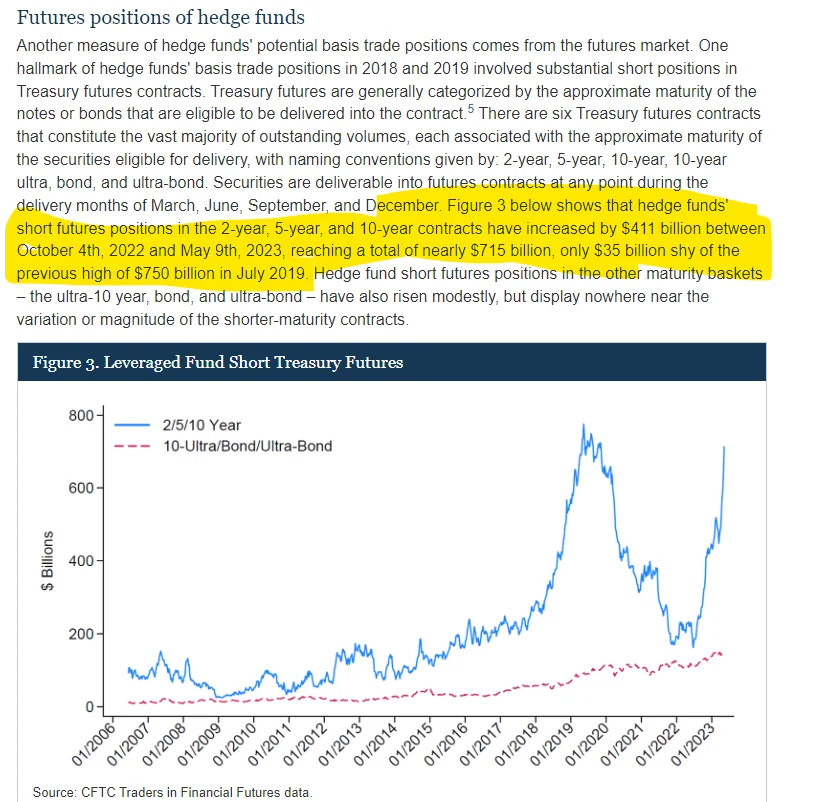

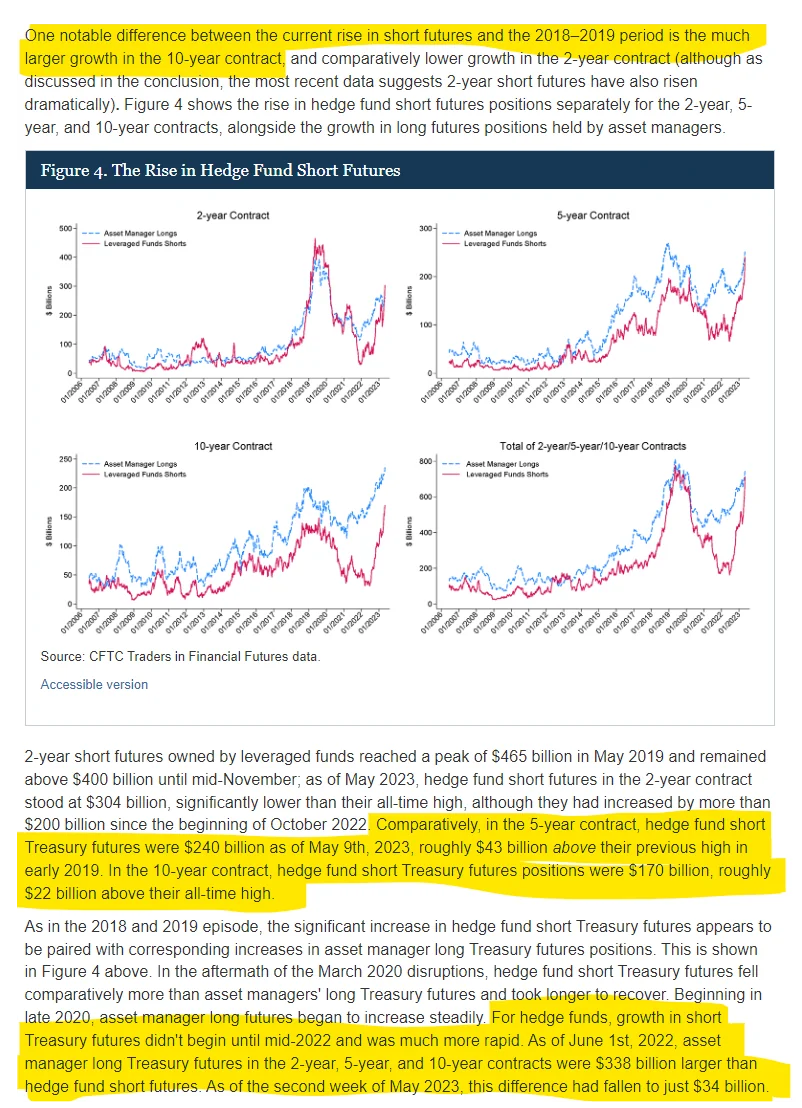

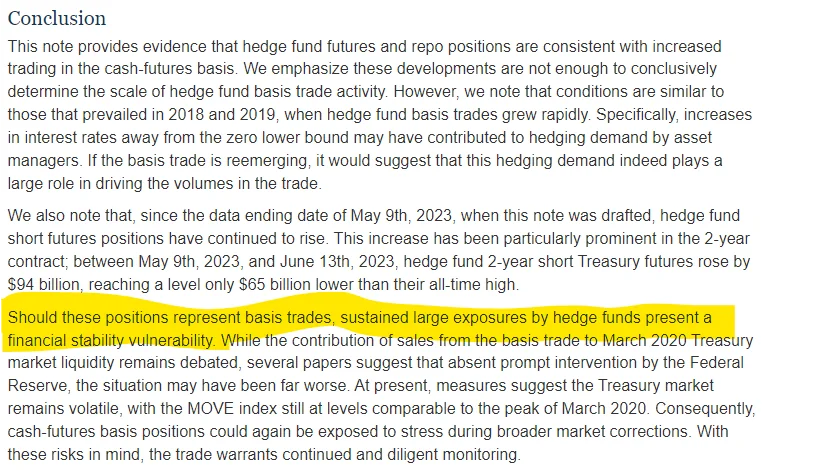

"We also note that, since the data ending date of May 9th, 2023, when this note was drafted, hedge fund short futures positions have continued to rise"

- "We also note that, since the data ending date of May 9th, 2023, when this note was drafted, hedge fund short futures positions have continued to rise"

- "Should these positions represent basis trades, sustained large exposures by hedge funds present a financial stability vulnerability."

In June, the total amount of money owed to finance companies (Consumers, Real Estate, Business) increased 17.7%

Proposed 944 page rule "that would substantially revise the capital requirements applicable to large banking organizations and to banking organizations with significant trading activity."

SEC Directs Equity Exchanges and FINRA to Improve Governance of Market Data Plans

- SEC Directs Equity Exchanges and FINRA to Improve Governance of Market Data Plans.

- SEC instructs equity exchanges and the Financial Industry Regulatory Authority (FINRA) to create a new National Market System (NMS) plan.

- This new plan will replace the existing three NMS plans that currently govern how real-time, consolidated equity market data is publicly disseminated.

- Calls out Conflicts of Interest.

US private funds, Hedge Funds sues securities regulator over new rules. New disclosure rules have hedgies big mad!

- Six private equity and hedge fund trade groups on Friday sued the SEC, arguing the agency overstepped its statutory authority when adopting sweeping new expenses and fees rules last week.

- "The rules exceed the Commission's statutory authority, were adopted without compliance with notice-and-comment requirements, and are otherwise arbitrary, capricious, an abuse of discretion, and contrary to law, all in violation of the Administrative Procedure Act," the associations wrote in the lawsuit.

- They asked the court to vacate the rules.

Fed's Beige Book August 2023: "Some Districts highlighted reports suggesting consumers may have exhausted their savings and are relying more on borrowing to support spending."

- "Some Districts highlighted reports suggesting consumers may have exhausted their savings and are relying more on borrowing to support spending."

- "Bankers from different Districts had mixed experiences with growth in loan demand. Most indicated that consumer loan balances rose, and some Districts reported higher delinquencies on consumer credit lines."

- "Agriculture conditions were somewhat mixed, but reports of drought and higher input costs were widespread."

- "Many contacts suggested "the second half of the year will be different" when describing wage growth."

- "Growth in labor cost pressures was elevated in most Districts, often exceeding expectations during the first half of the year."

- "Contacts in several Districts indicated input price growth slowed less than selling prices, as businesses struggled to pass along cost pressures."

- "As a result, profit margins reportedly fell in several Districts.

Unrealized losses on securities totaled $558.4 billion in the 2nd quarter, up $42.9 billion (8.3%) from the prior quarter

- Unrealized losses on securities totaled $558.4 billion in the 2nd quarter, up $42.9 billion (8.3%) from the prior quarter. Unrealized losses on held-to-maturity securities totaled $309.6 billion in the 2nd quarter, while unrealized losses on available-for-sale securities totaled $248.9 billion.

July was the 14th consecutive month of net outflows for the hedge fund industry

- July was the 14th consecutive month of net outflows for the hedge fund industry. Investors removed an estimated net $5.6 billion from hedge funds in July.

- From 1/1/2022-7/31/23, Investors have removed $163.58 billion from hedge funds.

"Similar to the role of securitization during the GFC, tokenization can potentially disguise riskier or illiquid reference assets as safe and easily tradeable, possibly encouraging higher leverage and risk-taking."

NY Fed August 2023 Survey of Consumer Expectations: "job loss expectations rose sharply to its highest level since April 2021."

- Income growth perceptions declined in August, and job loss expectations rose sharply to its highest level since April 2021.

- Perceptions about current credit conditions and expectations about future conditions both deteriorated.

- Households’ perceptions about their current financial situations and expectations for the future also deteriorated.

In July, consumer credit (AKA DEBT) increased at a seasonally adjusted annual rate of 2.5 percent. Revolving credit (Credit cards) increased at an annual rate of 9.2 percent

- Total consumer credit increased at an annual rate of 2.5% in July 2023.

- Revolving credit (which includes credit cards) grew at an annual rate of 9.2% in July 2023.

- Nonrevolving credit (which includes loans for things like cars and education) increased at .2%.

- Regarding the total outstanding consumer credit as of July 2023:

- The total outstanding consumer credit was $4,984.7 billion (NEW ALL TIME HIGH, SO FAR)

- Revolving credit accounted for $1,270.7 billion of the total outstanding consumer credit. (NEW ALL TIME HIGH, SO FAR)

- Nonrevolving credit constituted $3,714.5 billion of the total outstanding consumer credit. (JUST OFF LAST MONTH'S ALL TIME HIGH)

Banking Trade Associations are BIG mad at proposal by U.S. banking regulators to require lenders to hold more capital on their balance sheets, send letter calling on banking agencies to Re-Propose Basel Rule

26 banking trade associations send letter AGAINST the SEC's proposed Custody Rule

- "The segregation of client assets requirement would effectively prohibit prime brokers from providing margin financing by rehypothecating client assets"

- "Requiring qualified custodians to hold client cash in segregated, off-balance sheet accounts would fundamentally disrupt the core banking model of taking deposits, providing credit, and facilitating payments."

SEC alleges Virtu Financial Inc. "Failed to Adequately Establish, Maintain, and Enforce Reasonably Designed Information Barriers to Prevent Proprietary Traders from Misusing Nonpublic Customer Post-Trade Information"

- Virtu provided access to this information, regardless of whether the employee had a valid business need for such information. Such trading information, when collected in this form, constitutes MNPI, and access to such MNPI could be valuable to a trader.

- For example, a trader could observe that VAL had executed the orders of a large institutional customer throughout the day, understand that the same customer may follow a similar trading pattern over the next day or days, and take advantage of such information by trading ahead of the customer’s subsequent orders.

In August, the Consumer Price Index for All Urban Consumers increased 0.6 percent, seasonally adjusted, and rose 3.7 percent over the last 12 months, not seasonally adjusted

- Corporate media will try and say this is a last 'summer hoorah' of spending. Compared to August 2022, this is just inflation GROWING unabated.

SEC Proposes Improvements to better secure EDGAR access. Current requirements see one login per company shared for access

FINRA is proposing to extend, to May 22, 2024, the implementation date of the amendments to FINRA Rule 4210 (Margin Requirements) set to go into effect October 25, 2023

Wholesale inflation posts largest increase in 14 months as producer price index jumped .7% (economists predicted .4%) in August

- The PPI report captures what companies pay for supplies such as fuel, packaging, shipping, etc.

- These costs are usually passed on to the consumer, so is a good barometer for which way inflation is going--the number came in double what was expected.

- Paired with recent CPI data, inflation is nowhere near under control!

The Fed's Enhanced Financial Accounts (EFAs) on Hedge Funds: Hedge Fund liabilities hit new all time high in 2023:Q1

- Hedge Fund exposure from derivatives grew 4.47% or $354.91 Billion from 2022:Q4 to 2023:Q1

- Leveraged Loans hit a new all-time high.

- Security repurchase agreements also hit an all-time high

Treasury: "We believe buybacks can play an important role in helping to make the Treasury market more liquid and resilient by providing liquidity support. The buyback program will also help Treasury to better achieve our debt management objectives."

August 2023 Money Stock Measures: M1 shrinks $126.6B (-.69%), M2 shrinks $40B (-.19%)

- August 2023 Money Stock Measures: M1 shrink $126.6B (-.69%), M2 shrink $40B (-.19%).

- Currency: Down $4.7 billion (-.21%)

- Demand Deposits: Down $43.8 billion (-.89%)

- Other Liquid Deposits: Down $57.9 billion (-.52%)

Fed OIG Report on SVB: Officials considered removing SVB’s CEO from FRB San Francisco’s board of directors after discussions to downgrade SVB’s rating but chose not to for fear of spooking markets

- The supervisory approach of the Board and the Federal Reserve Bank of San Francisco did not adapt to SVB’s growing complexity, with insufficient resources and expertise, contributing to the oversight failure.

- A senior official did note that a Reserve Bank does not want a CEO of a bank whose ratings are falling serving as a board member at that Reserve Bank.

- "We also learned that FRB San Francisco and Board senior officials considered removing SVB’s CEO from FRB San Francisco’s board of directors following the discussions to downgrade SVB’s ratings; they ultimately decided that the CEO should remain on the board of directors to avoid revealing confidential supervisory information and potentially signaling to the market the bank’s declining condition."

- "We believe that the CEO’s service on the FRB San Francisco board of directors created an appearance of a conflict of interest for the System."

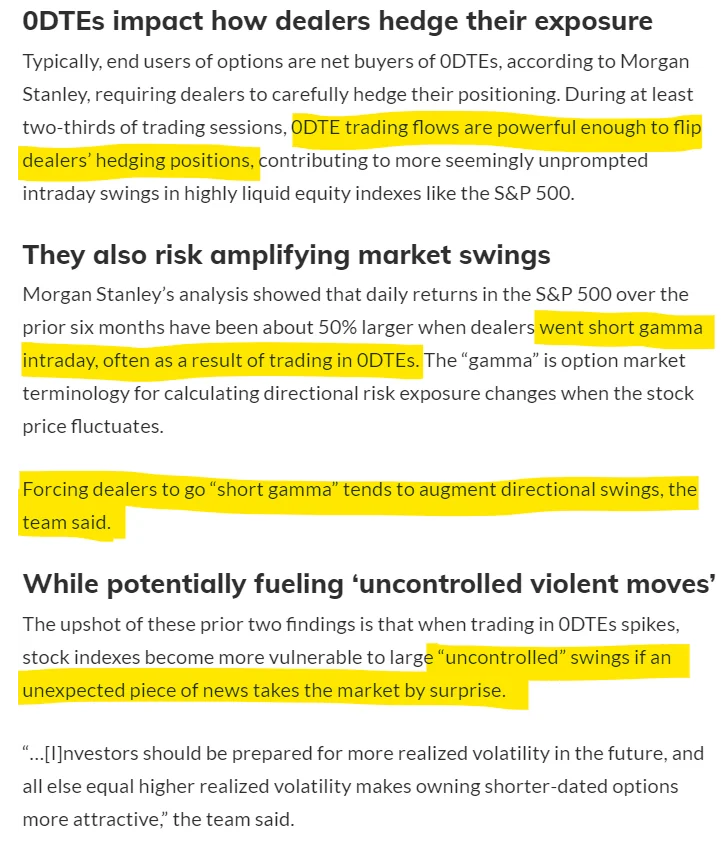

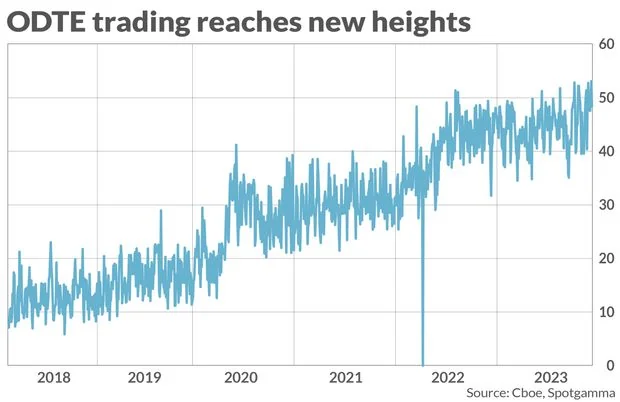

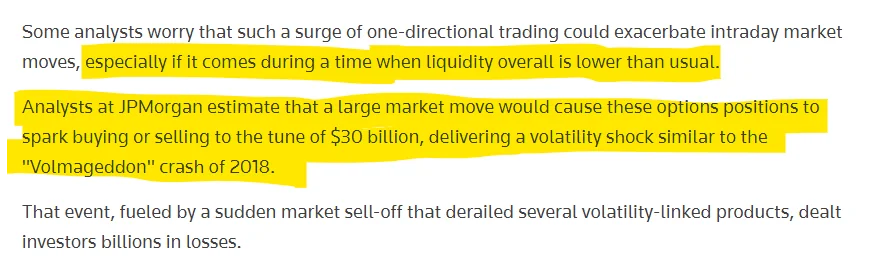

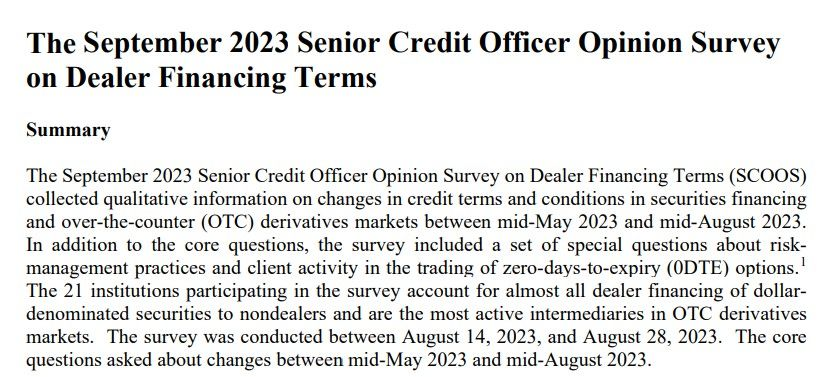

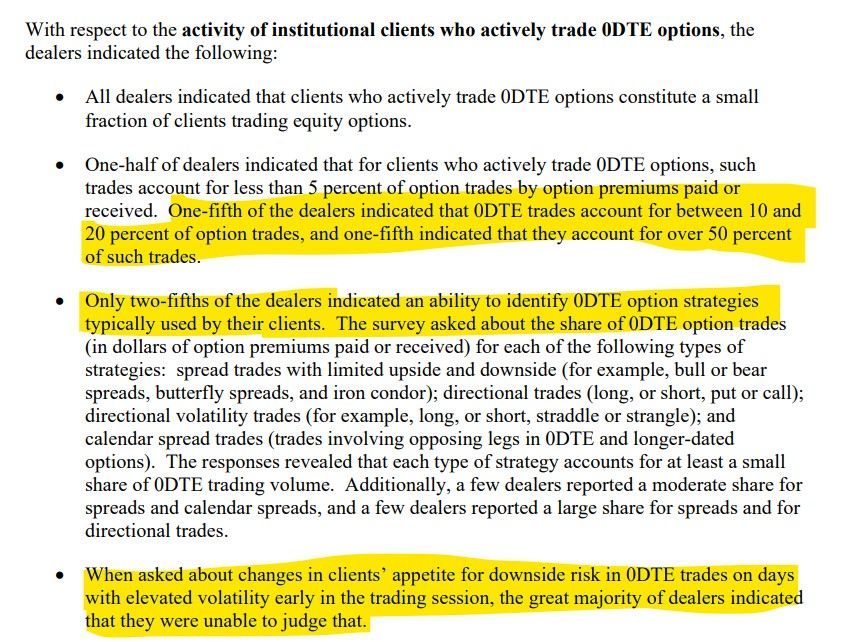

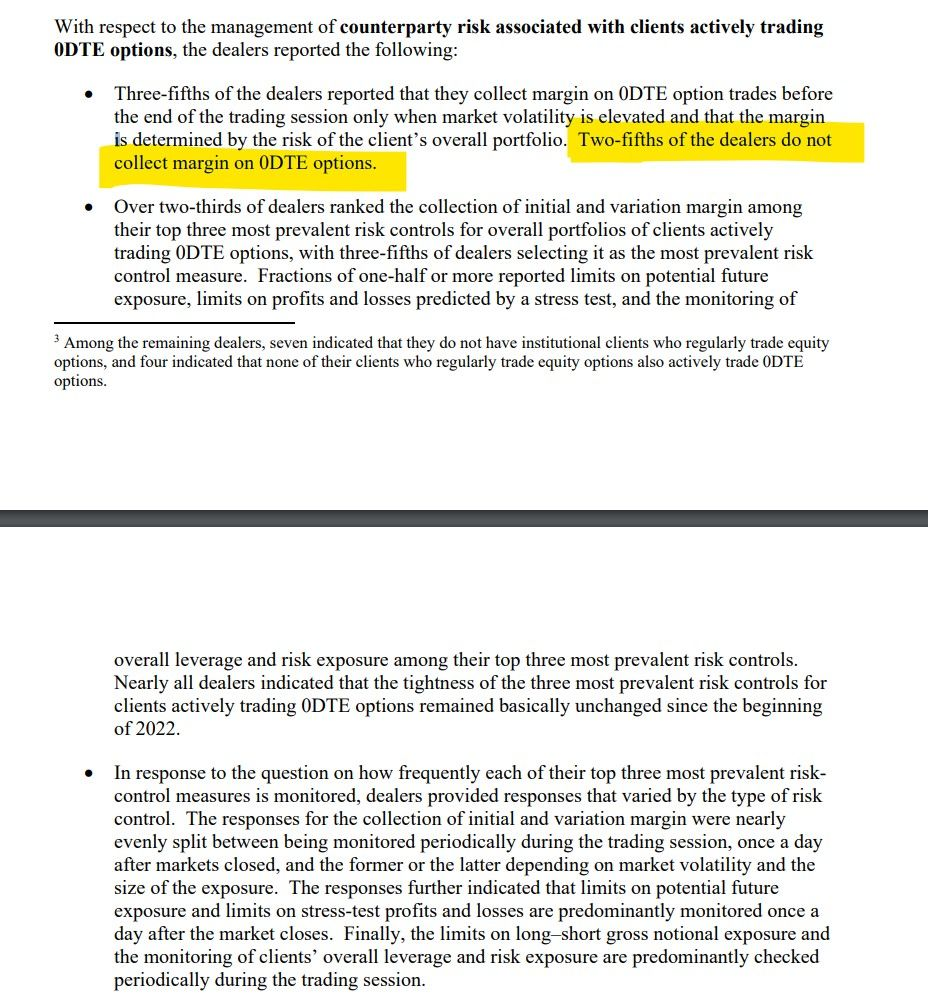

September 2023 Senior Credit Officer Opinion Survey, special questions about trading of zero-days-to-expiry (0DTE) options: "Two-fifths of the dealers do not collect margin on 0DTE options."

- Approximately two-fifths of dealers, on net, reported that they had increased the resources and attention they devoted to managing their concentrated credit exposure to other dealers and other financial intermediaries over the past three months--highest since June 2020.

- Approximately one-fourth of dealers, on net, indicated increased funding demand for equities (including through stock loans) over the past three months.

Vice Chair for Supervision Michael S. Barr: "I expect that the full effects of past tightening are yet to come in the months ahead."

- "While inflation has been moderating, incoming data on economic activity have shown considerably more resilience than I had expected."

- "I expect that the full effects of past tightening are yet to come in the months ahead."

- "In my view, the most important question at this point is not whether an additional rate increase is needed this year or not, but rather how long we will need to hold rates at a sufficiently restrictive level to achieve our goals. I expect it will take some time."

- "major portions of the financial sector are not subject to federal prudential regulation."

- "As I noted in a speech on bank capital earlier this year, we also need to worry about how risk outside the banking sector can threaten financial stability, as stress in broader financial markets is often transmitted to the banking system. So we need to take a broad view of financial stability."

Fed Governor Michelle Bowman: "more than 65 percent of banking markets, as currently defined, would be considered noncompetitive or "concentrated" in the language of antitrust"

- "In our current analytical framework, more than 65 percent of banking markets, as currently defined, would be considered noncompetitive or "concentrated" in the language of antitrust, yet the intense competition for banking products and services has only grown, principally from nonbanks. We need to reconcile that."

- "In our current framework, only 5 percent of the currently defined banking markets are considered highly competitive or "unconcentrated.""

- "In fact, today there are 19 states in the U.S. that do not have a single market that would be classified as highly competitive, and only 2 states have one-quarter or more of their markets designated as highly competitive."

- "The top three mortgage lenders in the country are nonbanks."

Bureau of Labor Statistics: Employment rose by 336,000 in September. Average hourly earnings up .2% for the month and 4.2% for the year. More inflation fuel!

U.S. Revolving credit (credit cards) grew by $14.7 billion (13.9%) in August, up from the $10.4 billion gain recorded in July

Fed Governor Michelle Bowman: "Inflation continues to be too high, and I expect it will likely be appropriate for the Committee to raise rates further and hold them at a restrictive level for some time"

Fed's Michael Barr: The rise in required capital is for activities that have generated outsized losses at large banks & areas where current rules have shortcomings

- "The proposal is projected to raise capital for large banks. This may result in higher funding costs. But this is only half the story. Capital also enables banks to absorb more losses without risking their ability to repay their creditors."

- "The bulk of the rise in required capital anticipated in the proposed rule is attributed to trading and other activities besides lending—activities that have generated outsized losses at large banks and areas where our current rules have shortcomings."

- "Large banks have experienced significant losses due to operational weaknesses over the past two decades. Experience shows that operational risk is inherent in all banking products, activities, processes, and systems and that losses at the largest banking organizations can be substantial."

- "The Basel Committee has published analysis illustrating the variability of credit-risk-weighted assets across banking organizations. See https://www.bis.org/publ/bcbs256.pdf and https://www.bis.org/bcbs/publ/d363.pdf. One result of these analyses is that across banking organizations, for an identical portfolio of wholesale loan exposures, required capital based on banks' internal models could vary by as much as 15 percent in either direction around a benchmark level."

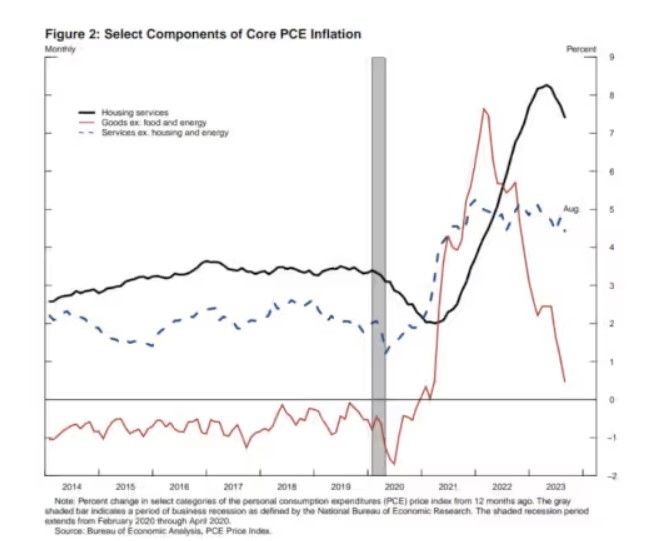

Fed's Jefferson on core nonhousing services inflation: "Since this segment accounts for more than 50% of the overall core PCE index, we will need to see further slowing in this area to meet our inflation objective."

- "Even though recent inflation data have been encouraging, inflation remains too high.

- "In contrast, price increases for the third category, core nonhousing services, the blue line, have yet to show a significant slowdown."

- "Since this segment accounts for more than 50 percent of the overall core PCE index, we will need to see further slowing in this area to meet our inflation objective."

- "Nevertheless, I believe that core PCE prices will moderate further as the labor market comes into better balance."

Financial Stability Board calls out Swiss Government handling of Credit Suisse, stating they ignored accepted resolution frameworks. I argue they did it for the 50 years of secrecy

SEC Adopts Amendments to Rules Governing Beneficial Ownership Reporting. The amendments also clarify the disclosure requirements of Schedule 13D with respect to derivative securities

- SEC Adopts Amendments to Rules Governing Beneficial Ownership Reporting.

- The amendments also clarify the disclosure requirements of Schedule 13D with respect to derivative securities.

- Gensler supports, Peirce opposes.

September Survey of Consumer Expectations: Inflation expectations 1yr 3.7%, 3yr 3.0% >2%. Households’ perceptions & expectations for credit conditions deteriorated

Fed Governor Michelle Bowman: "I am also monitoring the potential financial stability implications of nonperforming CRE loans that are packaged as part of commercial mortgage-backed securities (CMBS)."

Producer Price Index Rises 0.5% in September, 2.2% for year. This is the largest increase since April. Inflation still raging

As of 9/30/23 total outstanding amount of all advances from the liquidity fairy under the Bank Term Funding Program was $121,234,139,000. $2,645,685,000. in interest to survive another day...

Minutes of the Federal Open Market Committee, September 19-20, 2023: A few participants observed that there were challenges in assessing the state of the economy because some data continued to be volatile & subject to large revisions

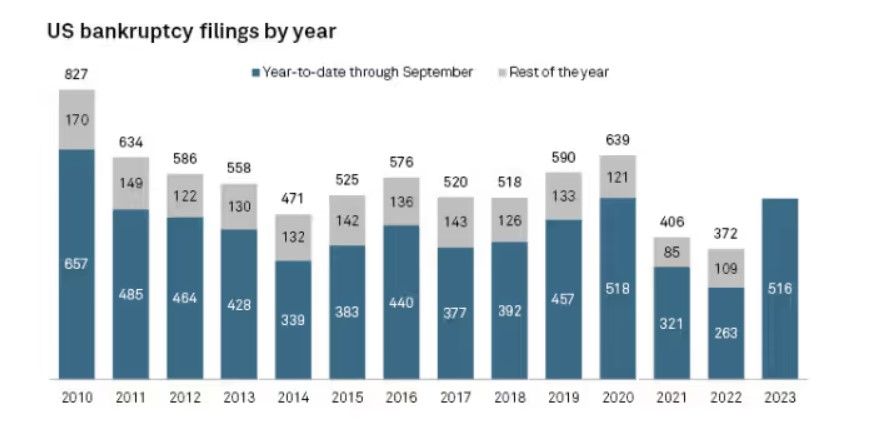

S&P Global Market Intelligence: US corporate bankruptcies showed no signs of slowing in September, closing out the quarter with the most bankruptcies (62) so far in 2023

- S&P Global Market Intelligence: US corporate bankruptcies showed no signs of slowing in September, closing out the quarter with the most bankruptcies (62) so far in 2023 (516 total).

- 114 bankruptcies since the end of July!

The acceleration of inflation continues: CPI for all items rises 0.4% in September and rose 3.7% over the last 12 months

- (CPI) rose by 0.4% in September from August.

- With month-to-month inflation continuing to grow, over the last 12 months, the all items index increased 3.7%.

- This is all on the heels of a red-hot August (.6% month-to-month, 3.7% year-over-year).

- Inflation is not slowing down!

Canada's Financial System Regulator: "we now consider CRE to be a higher risk item" "Elevated inflation puts pressure on retail, corporate, & commercial borrowers' ability to service debt."

SEC Adopts Rule to Increase Transparency in the Securities Lending Market

- Rule 10c-1a will require any “covered person” who agrees to a “covered securities loan” to provide specified information to an RNSA.

A covered person refers to:

- Any person that agrees to a covered securities loan on behalf of the lender (intermediary) other than a clearing agency when providing only the functions of a central counterparty or a central securities depository.

- Any person that agrees to a covered securities loan as the lender when an intermediary is not used.

- The broker or dealer when borrowing fully paid or excess margin securities.

A covered securities loan refers to

- A transaction in which one person – either on that person’s own behalf or on behalf of one or more other persons – lends a “reportable security” to another person, with exclusions for:

- positions at a registered clearing agency that result from central counterparty services or central depository services.

- the use of margin securities by a broker or dealer unless such broker or dealer lends such securities to another person.

Rule 10c-1a will require covered persons to provide certain terms of the covered securities loans to an RNSA, if applicable, including the:

- Legal name of the issuer of the securities to be borrowed;

- Ticker symbol of those securities;

- Time and date of the covered securities loan;

- Name of the platform or venue, if one is used;

- Amount of reportable securities loaned;

- Rates, fees, charges, and rebates for the loan;

- Type of collateral provided for the covered securities loan and the percentage of the collateral to the value of the reportable securities loaned;

- Termination date of the covered securities loan; and

- Borrower type, e.g., broker, dealer, bank, customer, bank, clearing agency, custodian. Additional loan terms that will be provided to the RNSA but will not be made public include:

- The legal names of the parties to the loan;

- When the lender is a broker-dealer, whether the security loaned to its customer is loaned from the broker-dealer’s inventory; and

- Whether the loan will be used to close out a fail to deliver pursuant to Rule 204 of Regulation SHO or whether the loan is being used to close out a fail to deliver outside of Regulation SHO.

- Effective within 60 days of publishing in the Federal Register

- Gary Gensler: "as relates to the reporting to regulators, the final rule will require lenders to report loan data to a registered national securities association—i.e., FINRA—by the end of each trading day."

- Hester Peirce: "While providing transparency regarding securities lending is a worthy & statutorily mandated objective, the approach we are voting on today is not the right way to achieve that objective. Accordingly, I cannot support this recommendation."

- Mark Uyeda "when these changes from the proposal are taken together, to what extent can the resulting information be used to estimate particular short selling positions & is that acceptable?"

SEC Adopts Rule to Increase Transparency Into Short Selling and Amendment to CAT NMS Plan for Purposes of Short Sale Data Collection

- Rule 13f-2 and Form SHO: Rule 13f-2 will require a Manager to file a Form SHO report via the Commission’s EDGAR system within 14 calendar days after the end of each calendar month with regard to:

- Each equity security that is of a class of securities that is registered pursuant to Section 12 of the Exchange Act or for which the issuer of that class of securities is required to file reports pursuant to Section 15(d) of the Exchange Act (“Reporting Company Issuer”) over which the Manager and all accounts over which the Manager (or any person under the Manager’s control) has investment discretion with respect to a monthly average gross short position that meets or exceeds a prescribed reporting threshold

- Each equity security that is of a class of securities of an issuer that is not a Reporting Company Issuer over which the Manager and all accounts over which the Manager (or any person under the Manager’s control) has investment discretion with respect to a gross short position that meets or exceeds a prescribed reporting threshold.

For each reported equity security, a Manager will be required to report on Form SHO certain information, including:

- The Manager’s end-of-month gross short position in the equity security at the close of regular trading hours on the last settlement date of the calendar month

- For each individual settlement date during the calendar month, the Manager’s “net” activity in the reported equity security, which includes activity in derivatives, such as options.

- The Commission will then publish, through EDGAR, and on a slightly delayed basis, certain aggregated short sale related information regarding each equity security reported by Managers on Form SHO.

- Gary Gensler: "Today, I’m pleased that, based upon public comment, we’re adopting a rule fulfilling that Congressional mandate. Today’s adoption will promote greater transparency about short selling both to regulators and the public."

- Lizárraga: "Although this rule imposes some recordkeeping obligations on broker-dealers, it does not require market participants to track whether short-sellers cover their short sales or report bona fide market-making information on a regular basis."

- Hester Peirce Statement on SEC's Short Sale Disclosure: "Because a narrower rule leveraging existing reporting requirements could have brought more meaningful transparency at lower costs, I cannot support this recommendation."

- Mark Uyeda on 'NO' for (Rule 13f-2): "Public knowledge of their short positions would render them susceptible to a short squeeze & also reduce the incentives to engage in this beneficial activity."

- Caroline Crenshaw: "This could help the SEC reconstruct market events & design responses to events that take place during times of volatility similar to the “meme” stock episode that might happen in the future."

SEC Division of Examinations Announces 2024 Priorities. SEC to probe transparency of fees, compliance with derivatives rules, & liquidation procedures amid market volatility

SEC Commissioner Mark Uyeda on SEC's agenda: "Have I tired you all out yet? The volume and breadth of these rules is staggering, but there are more proposed rules in the pipeline affecting asset managers and financial advisors."

"The past two years have been marked by a large number of proposed and adopted Commission rules. Many of these rules affect asset managers, including some that originated outside of the Commission’s Division of Investment Management. Let’s take a look back at some of these adopted rules, in chronological order:"

- November 2021: The Commission adopted amendments requiring a universal proxy card in all non-exempt solicitations involving contested director elections. [12] While the amendments do not apply to solicitations by registered investment companies and business development companies, the adopting release notes that an investment adviser’s fiduciary duty applies when it votes for the nominees listed on the universal proxy cards.[13] The practical effect of switching to universal proxy cards is a potentially increased workload for advisers. No longer is it a binary choice between one slate of directors or another, but now it involves selecting from a potential mix of candidates from both slates. If the dissident nominates four candidates, does an adviser vote for one, two, three, four, or none of them? If the adviser choses one or more dissident nominees, who does the adviser select from management’s candidates?

- July 2022: The Commission amended the rules governing proxy voting advice businesses.[14] The Commission also rescinded certain guidance to investment advisers about the use of proxy advisors when voting proxies.[15] This reversed amendments and guidance that the Commission had adopted a mere two years earlier in 2020 and that generally were effective for only one proxy season prior to reversal.[16]

- October 2022: The Commission adopted rule and form amendments that require mutual funds and ETFs to transmit summary shareholder reports.[17] Summary shareholder reports have the potential to provide investors with a more user-friendly and engaging presentation of key information about their fund investments. However, developing the form and style of new reports will require careful attention.

- November 2022: The Commission adopted amendments to Form N-PX to increase the amount of information about investment company proxy votes, including the categorization by subject matter of the votes.[18] The Commission also voted to require institutional investment managers to report on Form N-PX how they voted proxies for say-on-pay votes for executive compensation.[19] Thus, institutional investment managers that file Form 13F will now submit a form that previously was reserved only for investment companies. Non-investment company advisers will need to develop policies and procedures for submitting Form N-PX.

- February 2023: The Commission shortened the standard settlement cycle for equity transactions from two business days after the trade date ("T+2”) to one business day after the trade date ("T+1”).[20] A footnote in the adopting release makes clear that “an adviser that transacts with a broker-dealer that has policies and procedures pursuant to [new] Rule 15c6-2 may wish to evaluate whether its own policies and procedures are sufficient to ensure compliance with obligations requested by the broker-dealer.”[21] The footnote further advises that “the broker-dealer’s policies and procedures may provide that it generally should seek written assurances from the adviser that [the adviser’s] policies and procedures are sufficient to ensure compliance with obligations requested by the broker-dealer.”[22] Under the amendments, an adviser also will be required to make and keep books and records regarding certain transactions. The adopting release estimates that – of the 15,160 advisers registered with the Commission – close to 13,000 are likely to facilitate transactions that are subject to the new recordkeeping requirements.[23]

- May 2023: The Commission required new disclosures regarding share repurchases for issuers required to file periodic reports under the Securities Exchange Act of 1934 (“Exchange Act”).[24] This includes listed closed-end funds filing annual and semi-annual reports on Form N-CSR. These funds will now need to disclose daily, instead of aggregated monthly, quantitative repurchase data. Additionally, the adopting release highlights that – with respect to corporate issuers – “newly available data may incentivize intermediaries, such as investment advisers, to develop the capacity to analyze the data and provide their analysis to retail or other clients.”[25] In other words, the Commission is now suggesting that investment advisers may need to build out the capacity to put those disclosures to use.

- Also May 2023: The Commission amended Form PF to impose additional reporting requirements on large hedge fund advisers and private equity fund advisers.[26] While the adopting release claims that “the reporting requirements were…designed not to be overly burdensome,” it concedes that “at the margin, the heightened compliance costs for smaller advisers…may negatively affect competition.”[27]

- July 2023: The Commission amended the money market fund rules, adding a new liquidity fee for institutional prime and tax-exempt funds when net redemptions exceed 5% of net assets.[28] The adopting release explains that this new framework “will require [funds] to update policies and procedures, implement operational and systems changes, and coordinate with third party vendors, among other things.”[29]

- August 2023: The Commission adopted new rules for private funds and their advisers.[30] The Commission also changed Rule 206(4)-7 to require that the annual compliance review be documented in writing, which applies to all advisers and not just private fund advisers. The adopting release explains that “the availability of written documentation of the annual review should allow the Commission and the Commission staff to determine if the adviser is regularly reviewing the adequacy of the adviser's policies and procedures.”[31] This documentation “should promptly be produced upon request,”[32] which – in many cases – means “immediately or within a few hours of request.”[33]

- September 2023: The Commission amended the “names rule” under the Investment Company Act.[34] The amendments significantly broaden the scope of funds required to adopt a policy to invest at least 80 percent of their assets in accordance with the investment focus of the fund's name. The amendments also update the rule's notice requirements and establish recordkeeping requirements. The adopting release notes that fund compliance officers are required to discuss any material compliance matter involving the names rule in annual reports to the board on the operation of funds' compliance policies and procedures.[35]

- October 2023: The Commission adopted amendments that generally shorten the filing deadlines for initial and amended beneficial ownership reports filed on Schedules 13D and 13G,[36] which are required to be filed by investment advisers when they exceed specified ownership thresholds. Asset managers will need to update systems for monitoring ownership levels on a more frequent basis. In particular, the monitoring for a Schedule 13G filing currently is an annual exercise, but asset managers will need to monitor on a quarterly basis under the amendments.

- Also October 2023: The Commission adopted a new rule under the Exchange Act that requires certain persons to report information about securities loans to a registered national securities association.[37] To the extent that an investment company uses an agent for its securities lending program, the agent can file the reports under the rule. However, these costs could be passed on to lenders and beneficial owners,[38] so the ultimate costs to funds and advisers remains to be seen.

- Finally in October 2023: The Commission adopted a new rule that requires institutional investment managers that meet or exceed certain specified reporting thresholds to report short position data and short activity data for equity securities.[39] The new rule applies to investment advisers exercising investment discretion over client assets, including investment company assets.

"Have I tired you all out yet? The volume and breadth of these rules is staggering, but there are more proposed rules in the pipeline affecting asset managers and financial advisors."

"Put simply, the upcoming compliance calendar is daunting. Here are some deadlines to which you can look forward:"

- November 2023: Investment advisers must comply with the new requirement to document annual compliance reviews in writing.

- Early 2024: Beneficial owners must comply with the shortened Schedule 13D filing deadline and amended disclosures. The final date is triggered off of publication in the Federal Register – which has not yet occurred – but when it is published, affected persons will have 90 days to comply.

- April 2024: Firms must comply with certain provisions of the new money market fund rule, including the increased daily liquid asset and weekly liquid asset minimum liquidity requirements, as well as the discretionary liquidity fee framework for non-government money market funds.

- May 2024: Firms must comply with the transition to a T+1 settlement cycle, including the various rules related to that transition. Market participants asked for an implementation date in September 2024, so hopefully the technological and other changes will be fully tested and ready to be put in place.

- June 2024: Private fund advisers must comply with the amendments to Form PF. Firms must comply with other aspects of the new money market fund reforms, including the amendments to Forms N–MFP and N–CR. At the same time, firms will need to comply with an amendment regarding how money market funds categorize their portfolio investments on their websites.

- July 2024: Investment companies must comply with the new summary fund shareholder report rule.

- August 2024: Institutional investment managers and funds will be required to file their first reports on amended Form N–PX.

- September 2024: Listed closed-end funds must comply with the new disclosure and tagging requirements regarding share repurchases. Advisers with more than $1.5 billion in private fund assets must comply with portions of the new private fund advisers rule, including the adviser-led secondaries rule, the preferential treatment rule, and the restricted activities rule. Beneficial owners, including investment advisers with investment or voting discretion, must comply with the revised Schedule 13G filing deadlines, which will be required on a quarterly, not annual, basis.

- October 2024: Institutional prime and institutional tax-exempt money market funds must comply with the new mandatory liquidity fee framework.

- December 2024: Private fund advisers will need to comply with the new sections that have been added to Form PF.

- March 2025: All private fund advisers, including those with assets under $1.5 billion, must comply with all provisions of the new private fund advisers rule.

- December 2025: Larger investment companies, meaning those in fund families with at least $1 billion of collective assets, must comply with the amended fund names rule, while smaller funds must comply by June 2026.

"If any of the pending proposals are adopted, the compliance dates for those rules likely will overlap with these existing obligations. You have your work cut out for you."

Senior officials from the Bank of England, FDIC, CFTC, SEC, & the Fed convened a hybrid meeting today "to discuss certain issues relating to the resolution of a central counterparty (CCP)."

CFTC Releases Enforcement Advisory on Penalties, Monitors and Admissions: "In negotiations, respondents should no longer assume that no-admit, no-deny resolutions are the default."

- "If penalties are not sufficiently high, entities may choose to continue to behave unlawfully, viewing penalties as a cost of doing business."

- "Higher penalties may, in particular, empower compliance professionals at entities to make the business case to senior management for the resources they need to do their jobs effectively. Further, without sufficient penalties, entities may be less inclined to cooperate with the Division, believing that any penalty ultimately imposed will be acceptable and bearable."

- "Going forward, the Division is recalibrating how it is assessing proposed CMPs to ensure that the CMPs are at the level necessary to achieve general and specific deterrence, which may result in the Division recommending higher penalties in resolutions than may have been imposed in similar cases previously."

- "These considerations are especially salient in cases involving recidivism—i.e., repeated violations of law by the same person, for example where the proposed respondent has been the subject of previous Commission actions."

- "In negotiations, respondents should no longer assume that no-admit, no-deny resolutions are the default."

SEC Proposes Rule to Address Volume-Based Exchange Transaction Pricing for NMS Stocks

Proposed Rule 6b-1 would:

- Prohibit exchanges from offering volume-based transaction pricing in connection with the execution of agency or riskless principal orders in NMS stocks.

- Require exchanges that offer volume-based transaction pricing in connection with the execution of proprietary orders in NMS stocks for the account of a member to have anti-evasion measures, including rules requiring members to engage in practices that facilitate the exchange’s ability to comply with the prohibition, and written policies and procedures reasonably designed to detect and deter members from receiving volume-based pricing in connection with the execution of agency related orders in NMS stocks.

- Require exchanges that offer volume-based transaction pricing in connection with the execution of proprietary orders in NMS stocks for the account of a member to submit electronic, machine-readable structured data tables of certain information about their volume-based transaction pricing tiers and the number of members that qualify for each tier in an Interactive Data File in accordance with Rule 405 of Regulation S-T, which the public would be able to access through the Commission’s EDGAR system.

- OPEN FOR COMMENT!

- Gary Gensler on proposed Rule 6b-1: "Currently, the playing field upon which broker-dealers compete is unlevel." "we request public comment regarding whether volume-based discounts should be prohibited, & if so to what degree."

- SEC Commissioner Mark Uyeda on Proposed Rule 6b-1 (Volume-Based Exchange Transaction Pricing): "Ultimately, given the anticompetitive harms likely associated with the proposal—which will harm smaller entities and retail investors—I cannot support it."

- SEC Commissioner Hester Peirce in statement on Proposed Rule 6b-1 (Volume-Based Exchange Transaction Pricing): "This rulemaking appears to be the product of fear that is not rooted in reality. Accordingly, I cannot support it."

- Caroline Crenshaw: "While routing to that exchange would result in an economic benefit for the member in the form of reduced fees or increased rebates, it may be costly to the customer if it comes at the expense of execution quality."

Fed's Beige Book October 2023: "Wage growth remained modest to moderate in most Districts." "firms struggled to maintain desired profit margins"

Government in the Sunshine Meeting Notice! 10/18 the Fed held a CLOSED meeting as it was determined the public interest did not require opening the meeting for Discussion on Financial Markets, Institutions, & Infrastructure

Treasury International Capital Data for August: China sells the most U.S. securities in 4 years

- China sold nearly $14.867 billion in long-dated Treasuries in August, along with $5.113 billion in U.S. stocks.

- China sold $1.34 billion mortgage bonds.

- All told, Chinese institutions and funds sold $21.1 billion in U.S. assets.

- China has sold $235 billion in Treasuries since early 2022.

Fed Vice Chair for Supervision Michael S. Barr: "It is particularly important for us to consider a range of market shocks because some concentrated counterparty exposures may be revealed only under certain scenarios."

- "As we move forward, we must remain cognizant that none of us can predict future stressful events and their consequences with confidence."

- "It is particularly important for us to consider a range of market shocks because some concentrated counterparty exposures may be revealed only under certain scenarios."

- "A single scenario cannot cover the range of plausible risks faced by all large banks. This has been confirmed time and time again, including in recent experience."

- "We also do not take into account second-order effects of stress within the financial system, which are channels that amplify the effects of the shocks hitting bank's balance sheets, leading to losses spreading throughout the financial system."

National Association of Realtors: Sales of previously owned homes in the US fell by 2% from August to a seasonally adjusted annualized rate of 3.96 million units in September of 2023, the lowest since October 2010

- The median existing-home sales price grew 2.8% from one year ago to $394,300, marking the third consecutive month of year-over-year price increases.

- The inventory of unsold existing homes climbed 2.7% from the prior month to 1.13 million at the end of September, or the equivalent of 3.4 months' supply at the current monthly sales pace.

- NAR Chief Economist Lawrence Yun. "The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains."

U.S. Department of Treasury: IRS Launches New Initiatives Using Inflation Reduction Act Funding to Ensure Large Corporations Pay Taxes Owed

The Fed's October 2023 Financial Stability Report: Three-fourths of survey participants cite persistent inflation and potential residential and commercial real estate losses as top concerns

Unless my count is off (totally possible), the above are 75 items pointing to things teetering and this is before the rules are even fully in effect yet.

What are these rules about again?

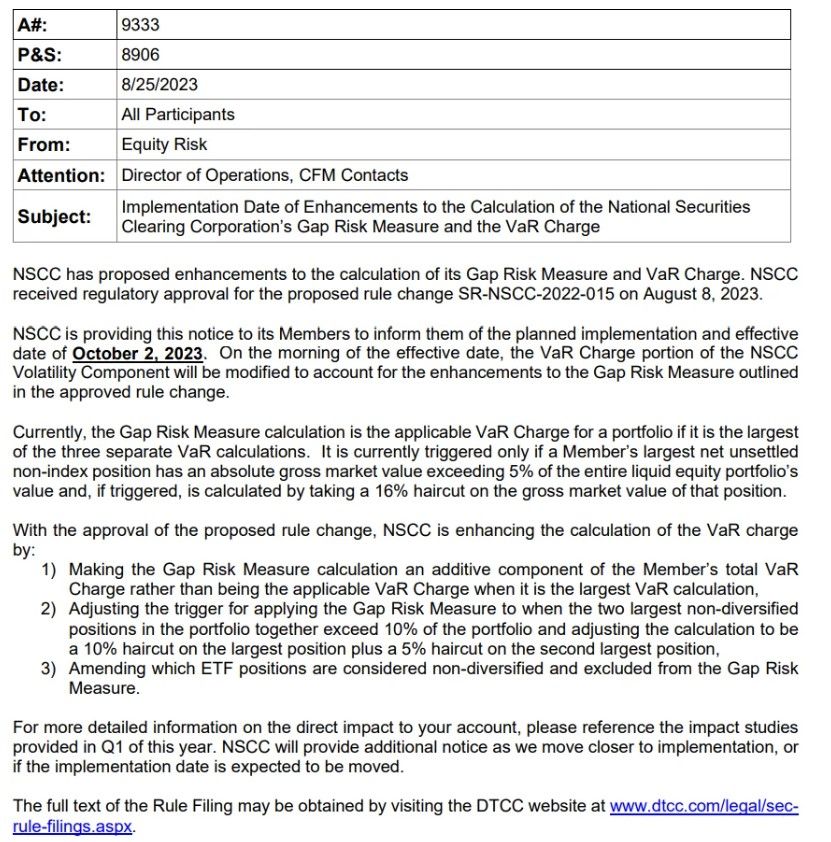

NSCC VaR Charge (effective 10/2):

- The NSCC approved Enhancements to the Gap Risk Measure & the VaR Charge.

- VaR tinkers with the mechanics that would have defaulted Robinhood & Others 1/28/21.

- The NSCC, previously saved them by sacrificing retail, in allowing Robinhood and others to alter their margin charges and freezing the buy button.

Wut Mean?:

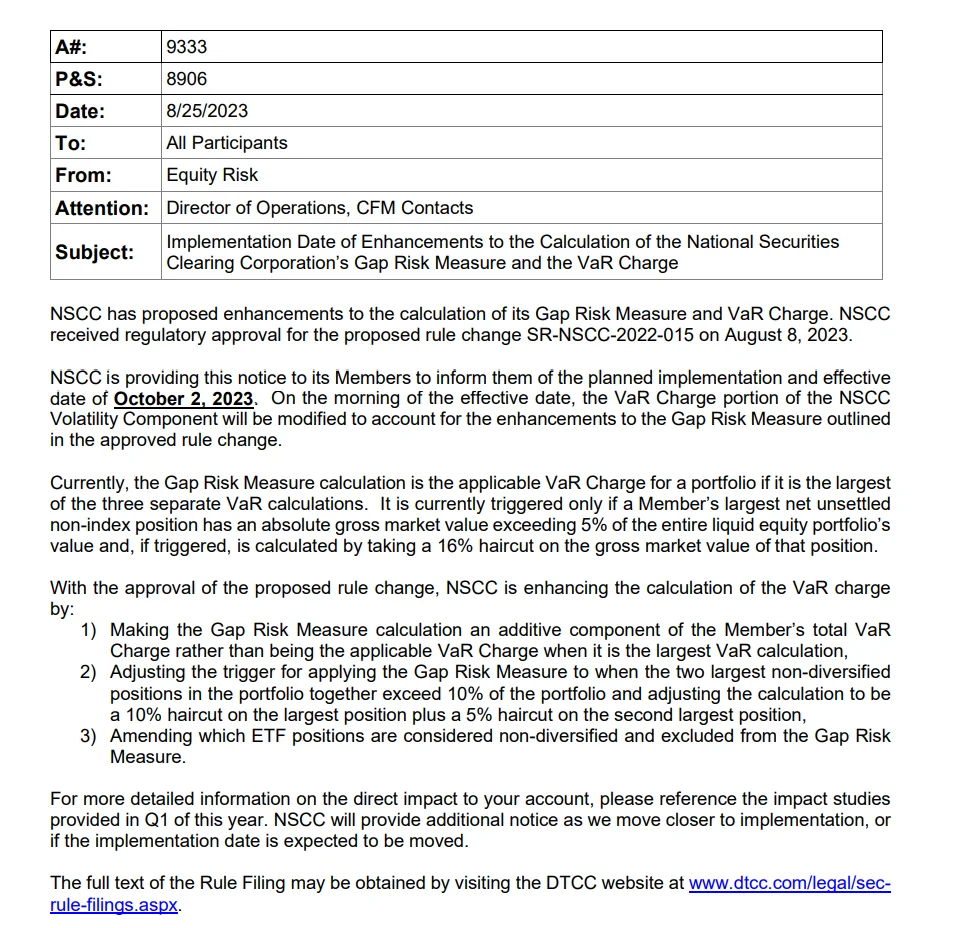

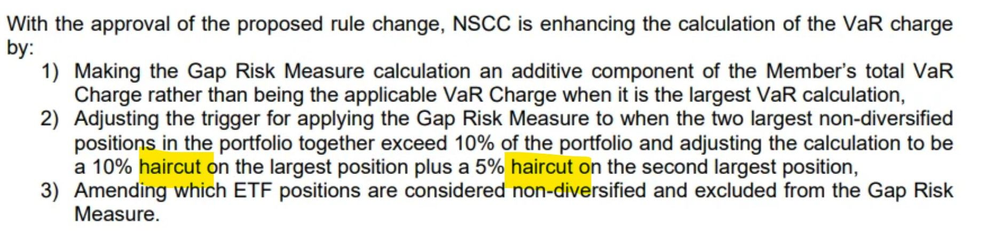

- The gap risk charge will now be added to a member's total VaR Charge whenever it applies. Previously, it only replaced the VaR Charge when it was the largest of three calculations. This addition improves the ability to handle unique risks.

- The gap risk charge will now consider the two largest positions in a portfolio instead of just the single largest one. This means the charge could apply when the combined value of these two largest positions exceeds a certain concentration threshold. This change offers better coverage for potential concurrent gap events in two major positions.

- The way the gap risk haircut (a percentage reduction) is determined will be revised. The minimum haircut for the largest position will be reduced from 10% to 5%, and a new minimum of 2.5% will be set for the second-largest position. This change in methodology is to ensure an appropriate margin level.

- NSCC will modify the criteria for ETF positions that are excluded from the gap risk charge. Instead of just excluding "non-index" positions, NSCC will exclude "non-diversified" positions, factoring in characteristics like the nature of the index the ETF tracks or whether the ETF is unleveraged. This change aims to be more precise about which ETFs are prone to gap risk and should improve transparency for members.

- Regarding the gap risk charge for securities financing transactions cleared by NSCC, the methodology of which already includes the gap risk charge as an additive component to margin and which would not change as a result of this proposal, (ii) to make clear that the gap risk charge applies to Net Unsettled Positions, (iii) to remove an unnecessary reference, (iv) to reflect that NSCC considers impact analysis when determining and calibrating the concentration threshold and gap risk haircuts, and (v) to make other technical changes for clarity).

Why is it changing? It's all about the idiosyncratic risk!:

- NSCC's proposed changes approved for the gap risk charge, ensuring the collection of adequate margin to address risks from members’ portfolios.

- Based on provided confidential data and impact study, the changes offer better margin coverage than the current methodology.

- Making the gap risk charge additive should help NSCC address more idiosyncratic risk scenarios in concentrated portfolios compared to the existing methodology.

- Adjusting the gap risk calculation for the two largest positions with two separate haircuts, based on backtesting and impact analysis, allows NSCC to cover risks from simultaneous gap moves in multiple concentrated positions.

- Changing criteria for ETFs in the gap risk charge (from non-index to non-diversified) enhances NSCC's precision in determining which ETFs are susceptible to gap risk events, improving risk exposure accuracy.

- The Proposed Rule Change equips NSCC to better manage its exposure to portfolios with identified concentration risk, hence limiting its risk exposure during member defaults.

- NSCC's rule ensures uninterrupted operation in its critical clearance and settlement services, even during a member default, by having adequate financial resources.

- The changes minimize the chance of NSCC tapping into the mutualized clearing fund, thereby reducing non-defaulting members' risk exposure to shared losses.

- The Commission believes these proposed changes will help NSCC safeguard securities and funds in its custody or control, aligning with Section 17A(b)(3)(F) of the Act.

The approved rule aims to address the potential increased idiosyncratic risks NSCC might face, especially regarding the liquidation of a risky portfolio during a member default.

- After reviewing NSCC’s analysis, the Commission agrees that the new rule would result in improved backtesting coverage, reducing credit exposure to members.

- The Commission asserts that this rule will empower NSCC to manage its credit risks more effectively, allowing it to adapt to backtesting performance issues, market events, structural changes, or model validation findings.

- This proactive management ensures NSCC can consistently collect enough margin to cover potential exposures to its members.

- The goal is to produce margin levels that align with the risk attributes of these concentrated holdings, especially securities more vulnerable to gap risk events.

- The rule would enhance NSCC's ability to recognize and produce margins that match the idiosyncratic risks and attributes of portfolios that meet the concentration threshold.

- Broadening the gap risk charge to an additive feature and focusing on the two largest non-diversified positions will help NSCC better manage the idiosyncratic risks tied to concentrated portfolios.

- Given the additive nature of the gap risk charge, the Commission agrees that the adjustments to its calculation, like establishing floors for gap risk haircuts for the two largest positions, are aptly designed to handle NSCC’s idiosyncratic risks exposure during member defaults.

- Introducing specific criteria to determine which securities fall under the gap risk charge will enable NSCC to pinpoint those more prone to idiosyncratic risks, ensuring ETFs identified as non-diversified are included.

So what should these changes mean?:

- Increased Margin Requirements: With the changes in the methodology, members should face higher margin requirements. The addition of the gap risk charge to the VaR Charge (as opposed to it only replacing the VaR charge when it's the largest of three calculations) would mean that members should be required to deposit more funds to NSCC to cover this risk.

- Multiple Significant Positions Impact: Previously, the gap risk charge considered only the largest non-index position. By considering the two largest positions in a portfolio, the margin requirements should rise for members who have significant short positions in multiple securities, especially if those securities are prone to volatile price movements....

- Revised Haircut Percentages: The change in haircut percentages implies concerns about the risk. The lowered percentages (from 10% to 5% for the largest position and a new 2.5% for the second-largest position) mean the gap risk charge should be applied more frequently.

- New Criteria for ETFs: By moving from "non-index" to "non-diversified" as the criteria for exclusion from the gap risk charge, there's a more refined approach to evaluating which ETFs are prone to gap risk. This should impact members who previously used certain ETF positions as a strategy to manage their margins...

- Increased Transparency: Improved transparency in terms of which ETFs are prone to gap risk means that members can make more informed decisions. However, it also implies that any loopholes or strategies that were previously employed might no longer be valid, leading to strategy changes or potential increased costs for some members.

Oh yeah:

- They are REALLY concerned about idiosyncratic risk:

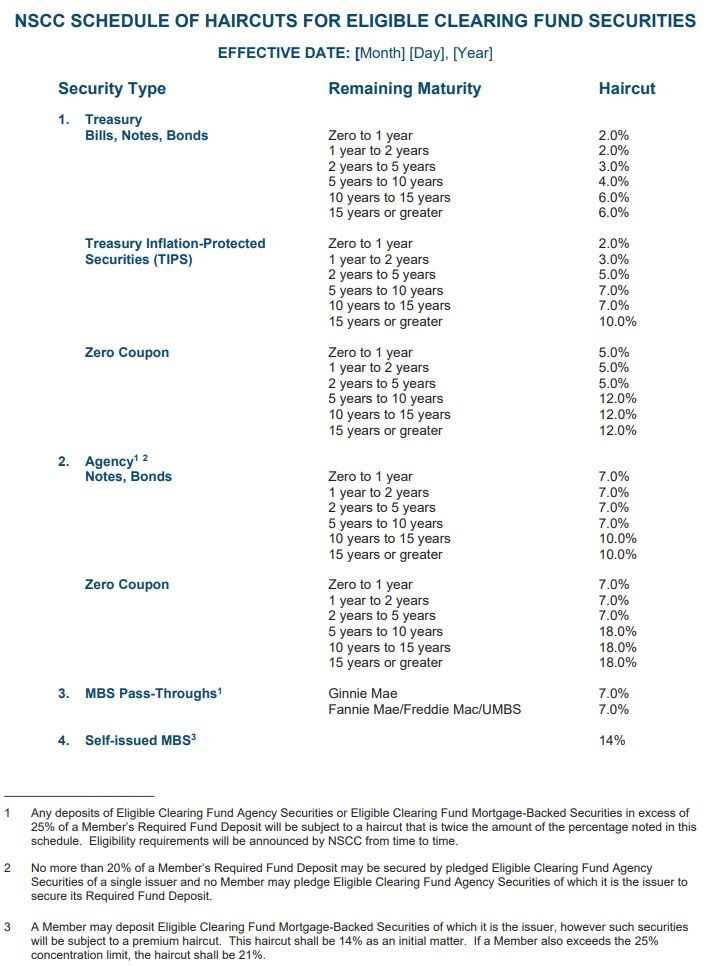

New NSCC Haircut schedule (effective within 60 business days of 10/4/23):

"Haircuts"

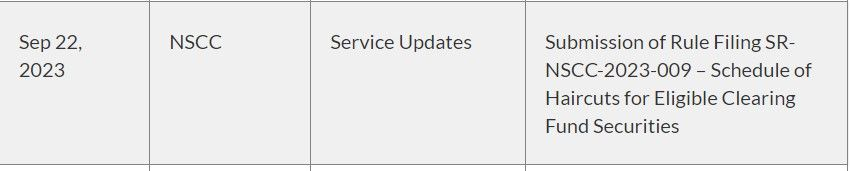

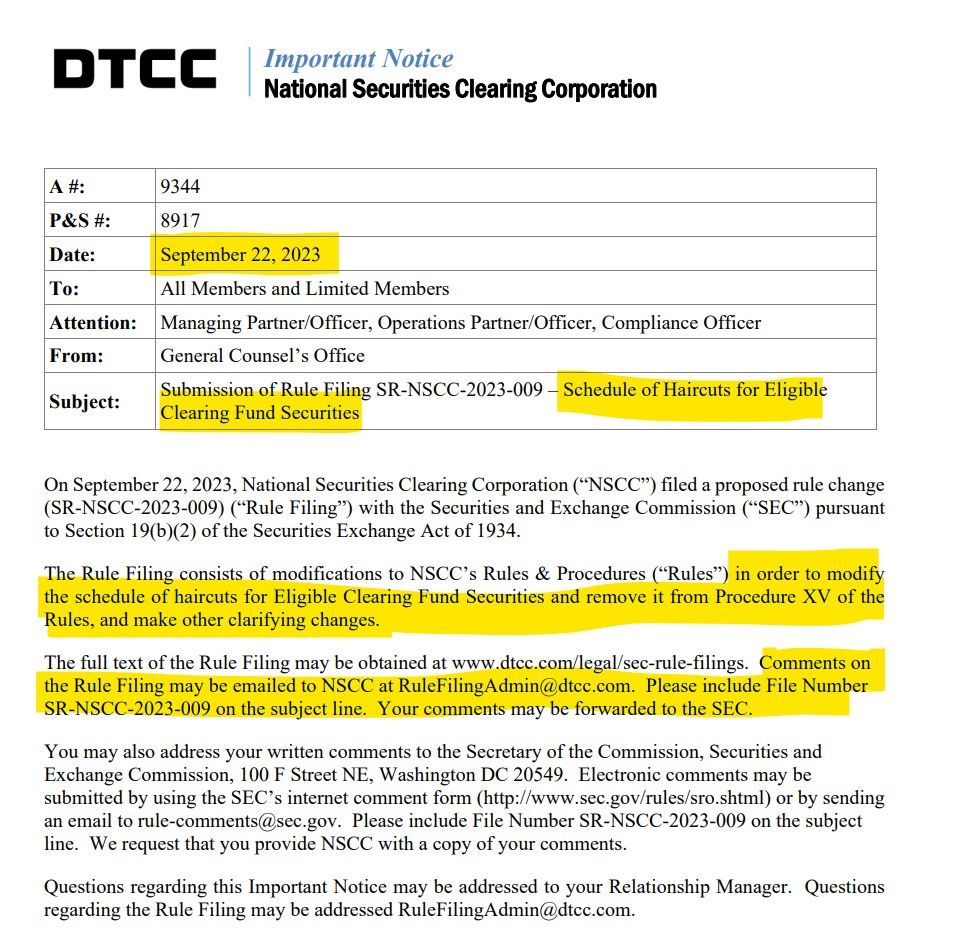

Recall, it was on 9/22 NSCC submitted to update the definition around "Haircuts":

This is a whopper of a statement:

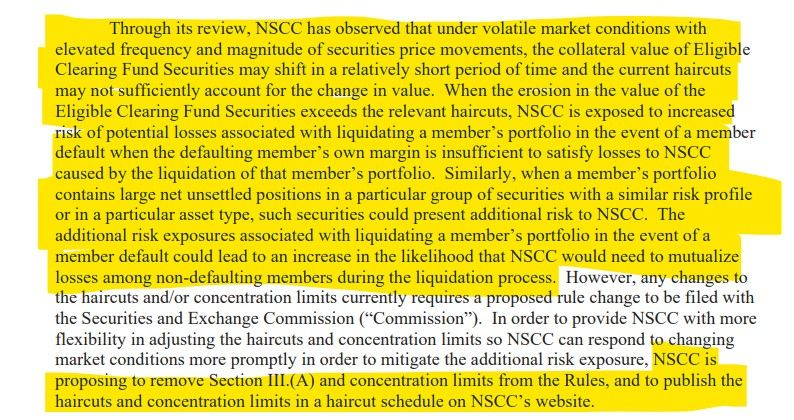

- Through its review, NSCC has observed that under volatile market conditions with elevated frequency and magnitude of securities price movements, the collateral value of Eligible Clearing Fund Securities may shift in a relatively short period of time and the current haircuts may not sufficiently account for the change in value."

- "When the erosion in the value of the Eligible Clearing Fund Securities exceeds the relevant haircuts, NSCC is exposed to increased risk of potential losses associated with liquidating a member’s portfolio in the event of a member default when the defaulting member’s own margin is insufficient to satisfy losses to NSCC caused by the liquidation of that member’s portfolio."

- "Similarly, when a member’s portfolio contains large net unsettled positions in a particular group of securities with a similar risk profile or in a particular asset type, such securities could present additional risk to NSCC."

- "The additional risk exposures associated with liquidating a member’s portfolio in the event of a member default could lead to an increase in the likelihood that NSCC would need to mutualize losses among non-defaulting members during the liquidation process."

So why are they keen on doing all of this?

It seems they are looking to speed up the process by which haircut changes are implemented--1 business day notices on the website vs having to go through the rules process.

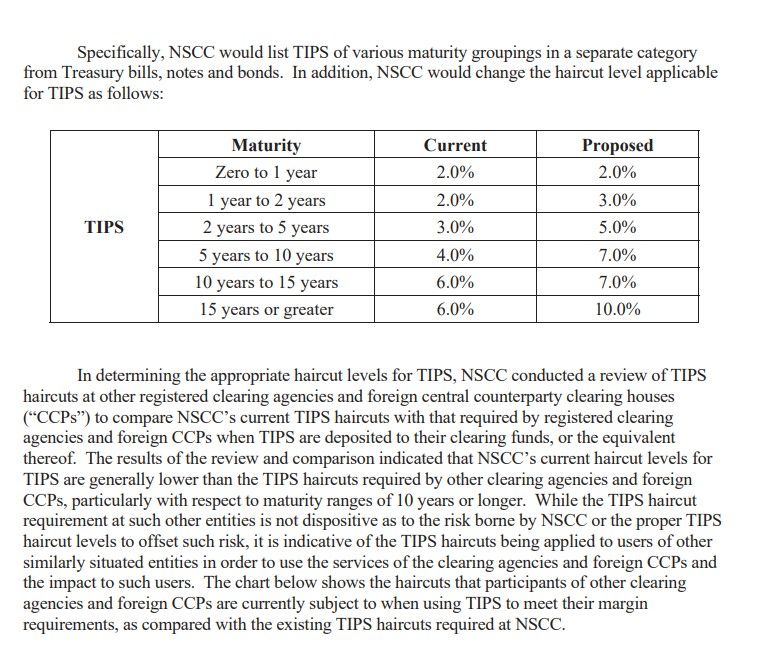

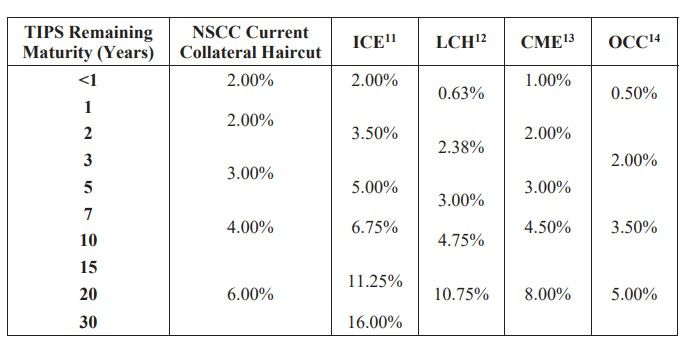

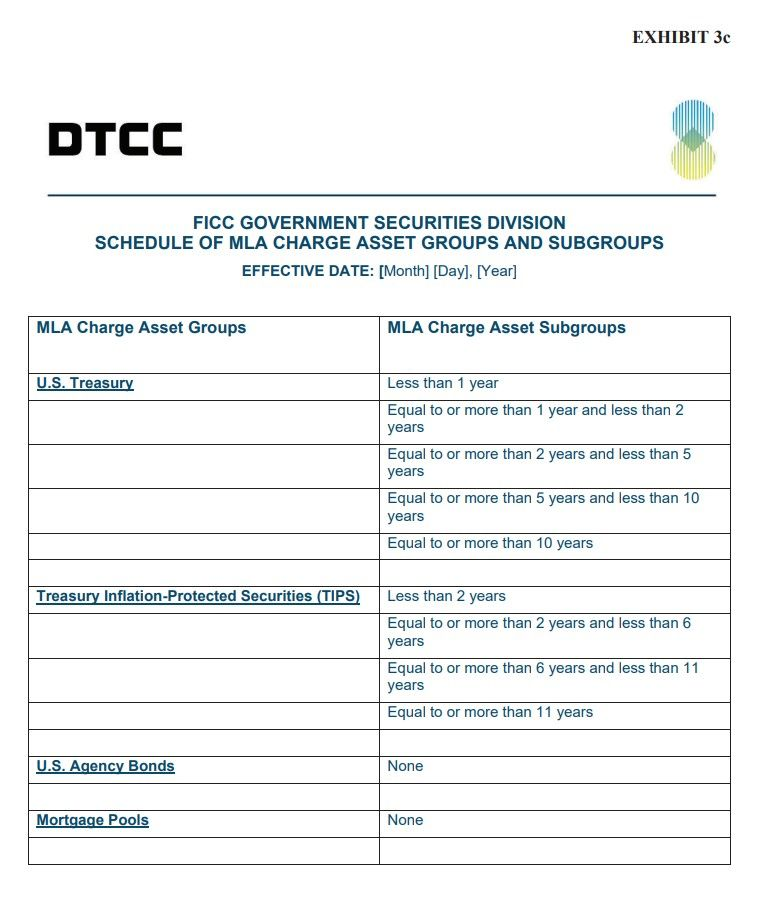

"Concurrent with moving the haircuts and concentration limits from the Rules to the website, NSCC is also proposing to reconfigure the categories relating to Treasury securities haircuts by moving the Treasury Inflation-Protected Securities (“TIPS”) to a separate category and increasing the haircut levels for TIPS."

Bloomberg a month ago:

The market for Treasury Inflation-Protected Securities is teaching investors a harsh lesson about interest-rate risk, ramping up the focus on this week’s auction of the debt.

Despite sticky price pressures, long-maturity TIPS are on track for their biggest monthly loss this year. Investors have driven up yields on all manner of long-dated bonds this month amid concern over the Treasury’s swelling borrowing needs and — ironically for TIPS — the risk that inflation may spike again or not decline smoothly.

NSCC is changing the haircut level applicable for TIPS as follows:

Side note, notice how the NSCC has previously DRASTICALY under collected on haircuts compared to other SROs?:

NSCC SCHEDULE OF HAIRCUTS FOR ELIGIBLE CLEARING FUND SECURITIES:

This is an interesting tidbit:

Wut Mean?

- It seems they are looking to speed up the process by which haircut changes are implemented--1 business day notices on the website vs having to go through the rules process.

- NSCC is also proposing to reconfigure the categories relating to Treasury securities haircuts by moving the Treasury Inflation-Protected Securities (“TIPS”) to a separate category and increasing the haircut levels for TIPS.

- This will be in effect within 60 days of the rule being approved.

So, why does this matter? 9/26:

This Follows up the planned implementation announcement from 8/25/23:

I'd like to call folks attention to something called out in the 8/25 announcement but not 9/26's:

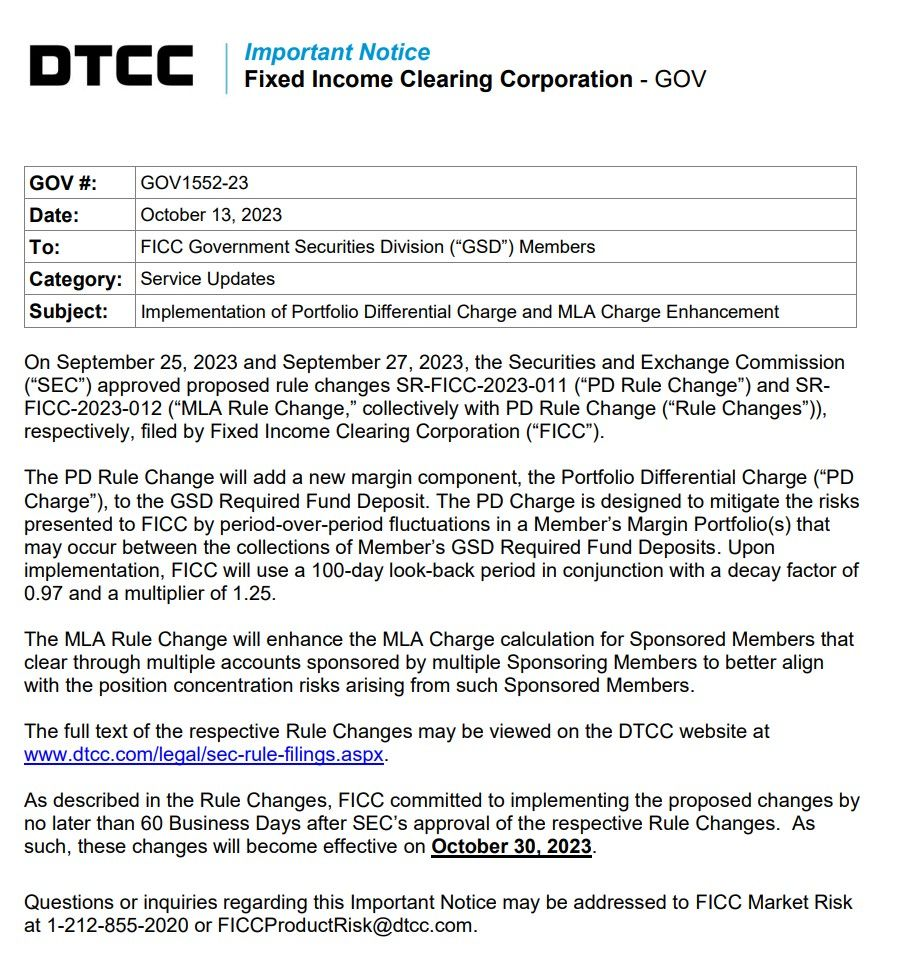

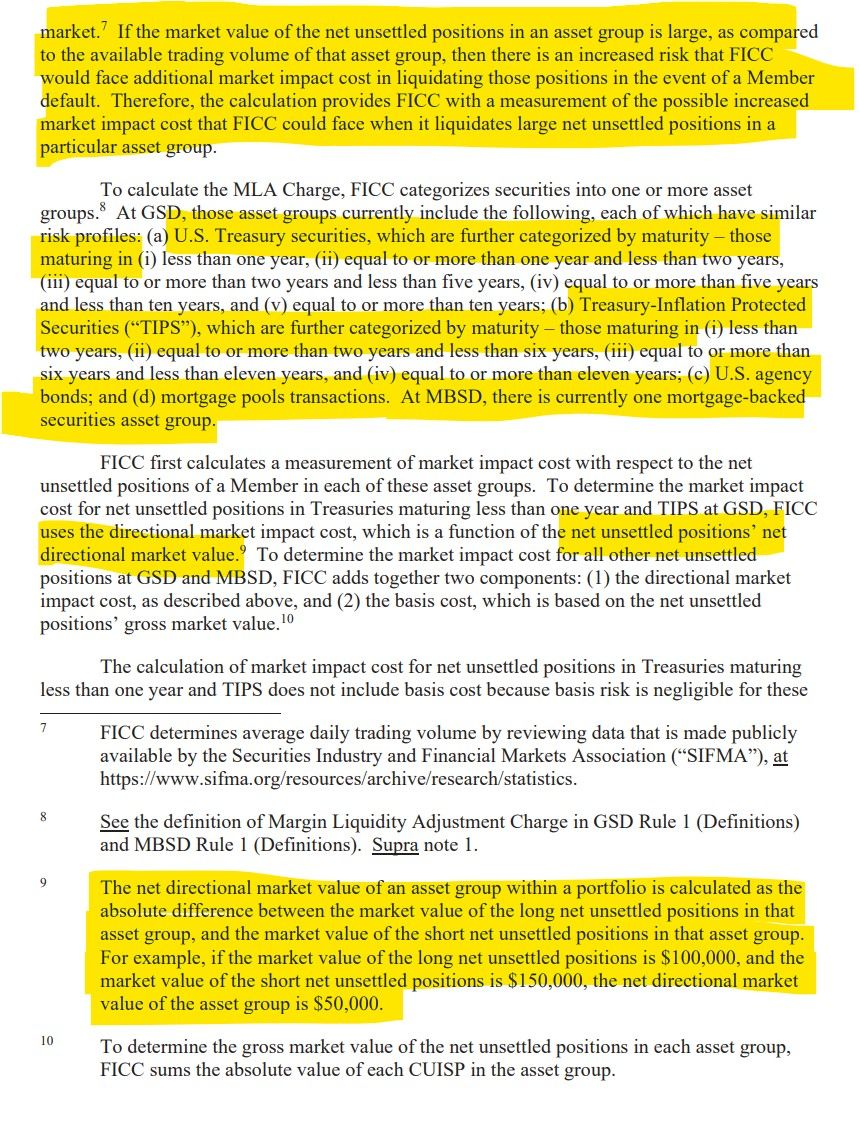

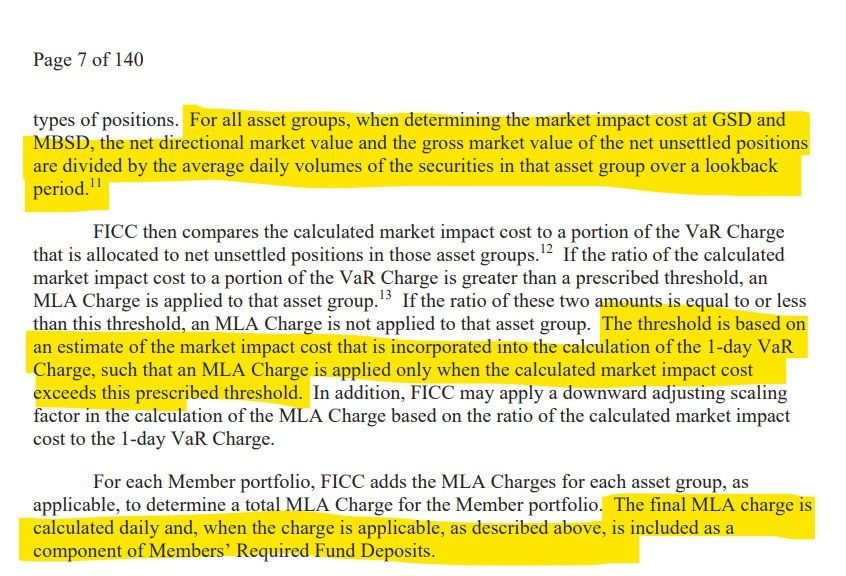

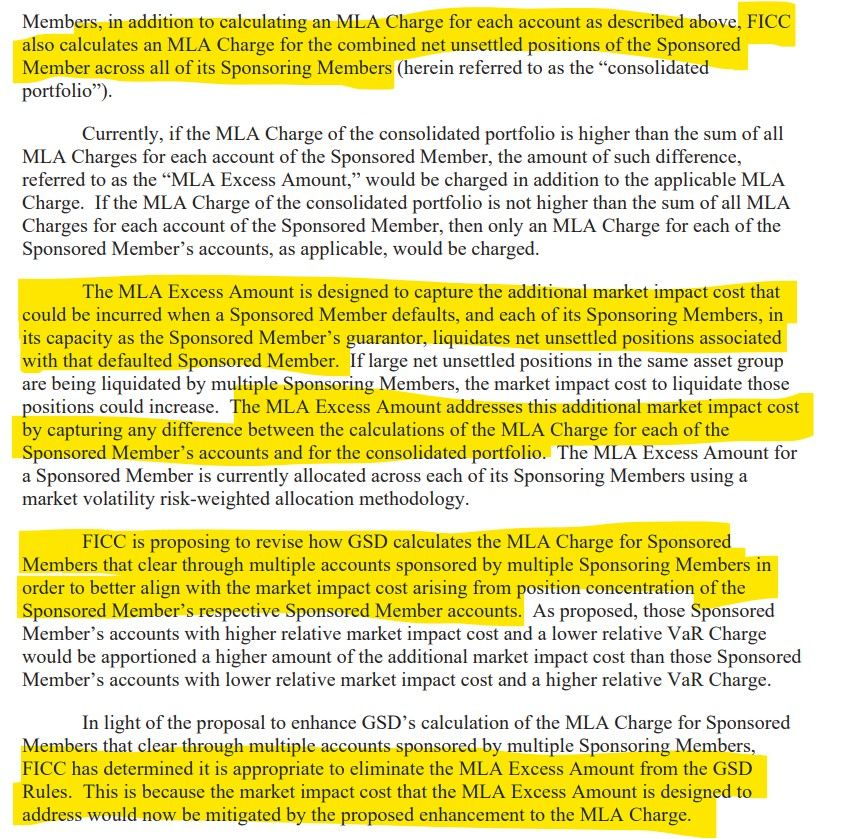

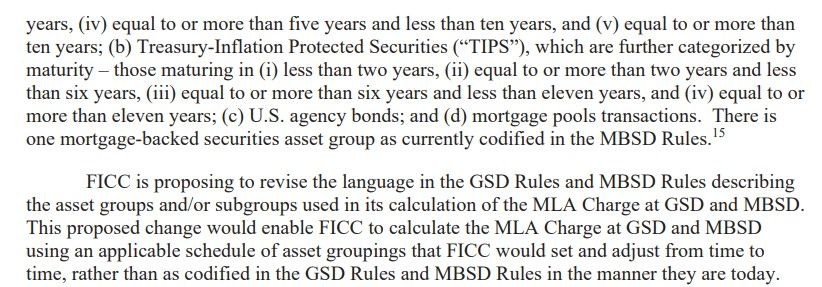

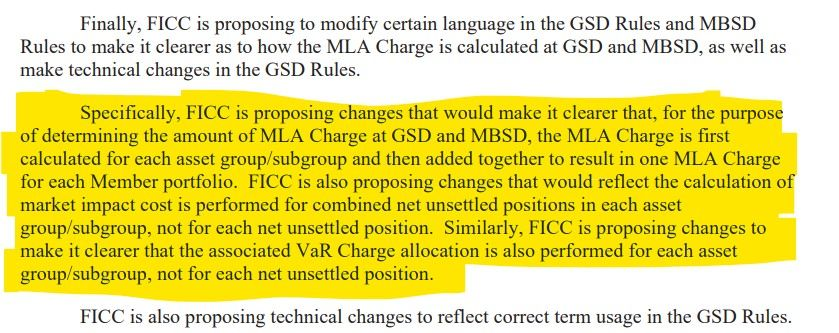

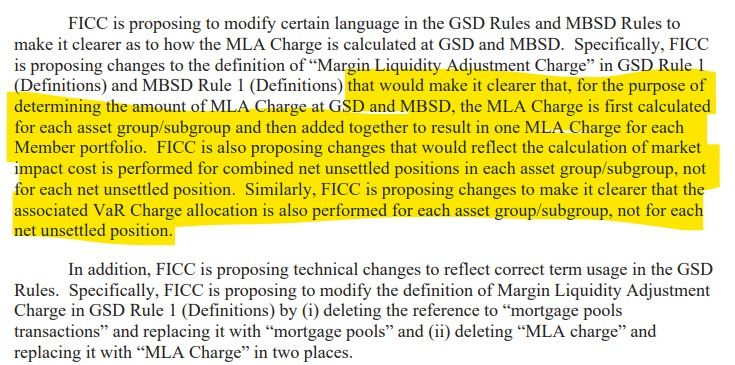

FICC's PD & MLA Rule changes:

What is happening?:

- The SEC approved proposed rule changes SR-FICC-2023-011 (PD Rule Change - 9/25/23) and SRFICC-2023-012 (MLA Rule Change - 9/27/23) filed by Fixed Income Clearing Corporation (FICC).

- The PD Rule Change will add a new margin component, the Portfolio Differential Charge (PD Charge), to the Government Securities Division (GSD) Required Fund Deposit.

- The PD Charge is designed to mitigate the risks presented to FICC by period-over-period fluctuations in a Member’s Margin Portfolio(s) that may occur between the collections of Member’s GSD Required Fund Deposits.

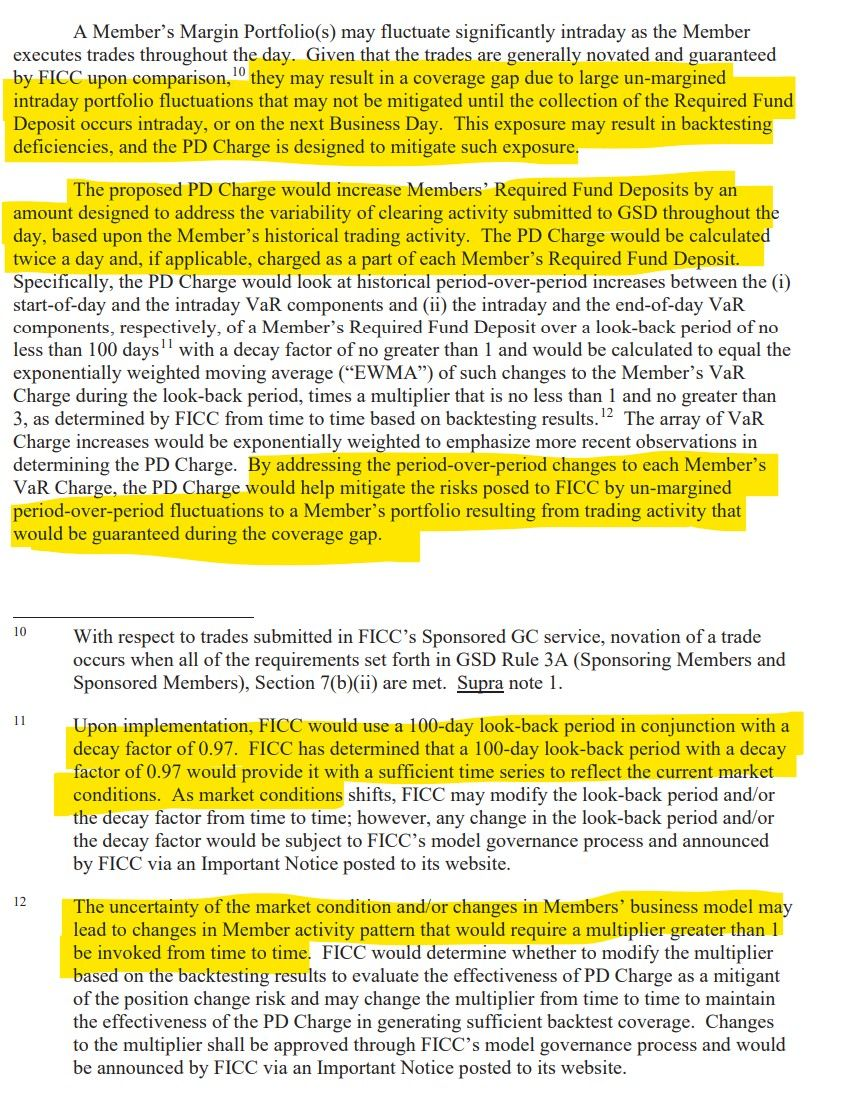

- Upon implementation, FICC will use a 100-day look-back period in conjunction with a decay factor of 0.97 and a multiplier of 1.25.

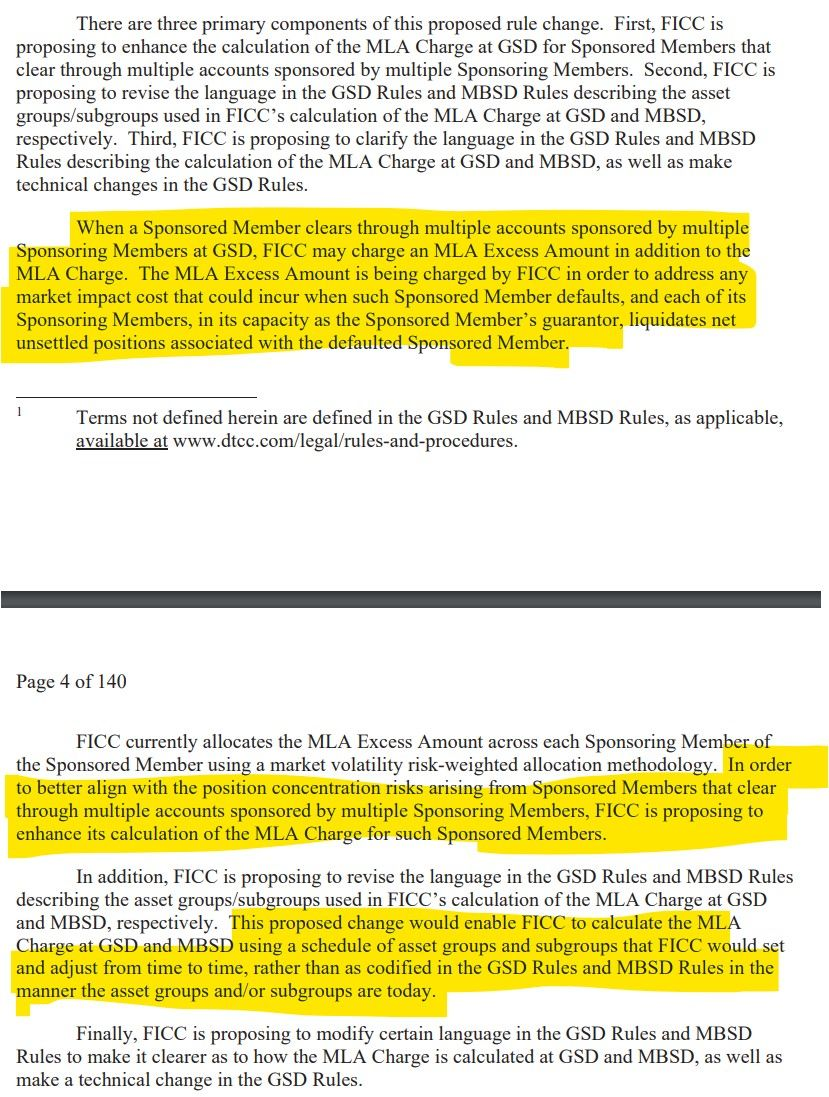

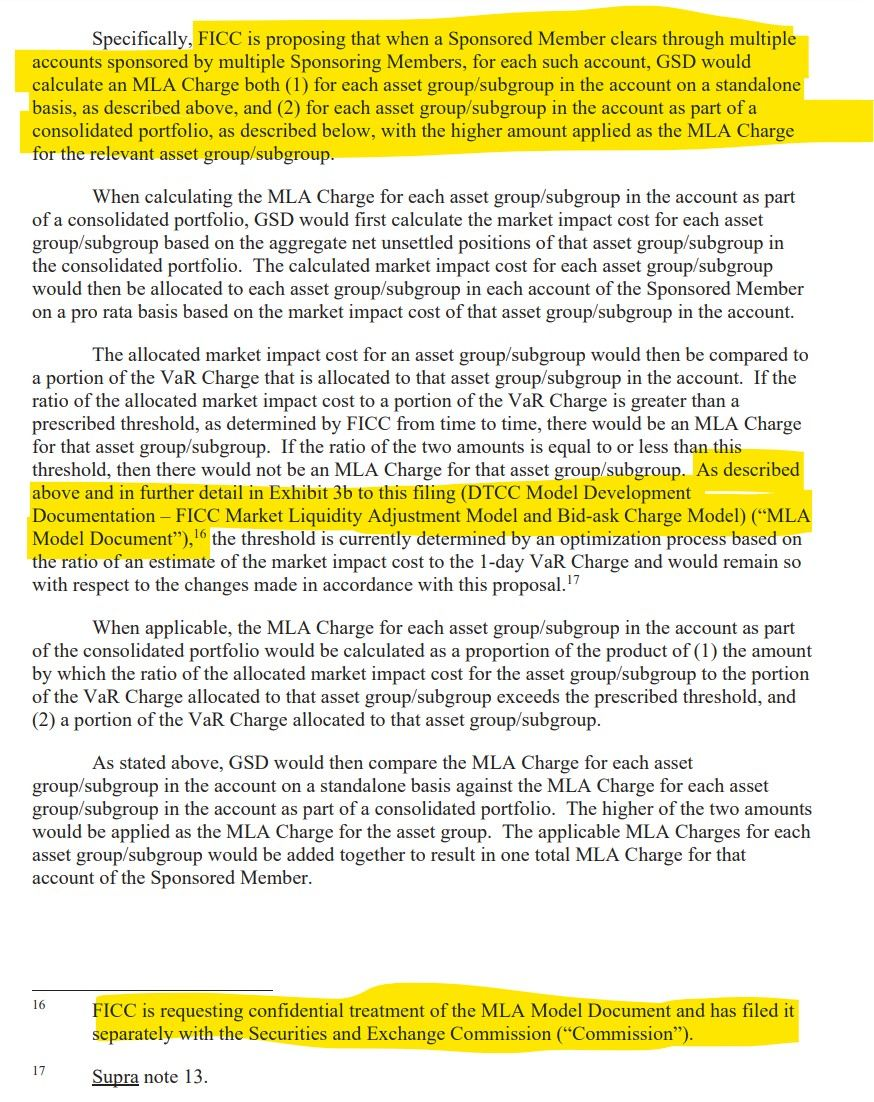

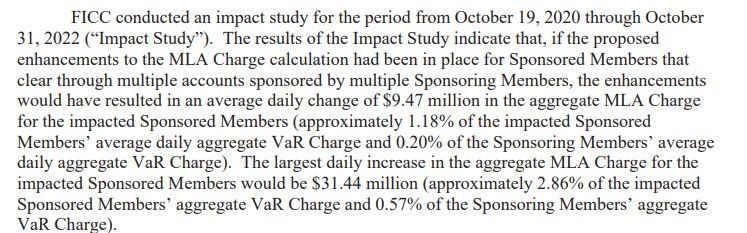

- The MLA Rule Change will enhance the MLA Charge calculation for Sponsored Members that clear through multiple accounts sponsored by multiple Sponsoring Members to better align with the position concentration risks arising from such Sponsored Members.

- FICC committed to implementing the proposed changes by no later than 60 Business Days after SEC’s approval of the respective Rule Changes.

- These changes will become effective on October 30, 2023.

SR-FICC-2023-011 (PD Rule Change):

Wut Mean?:

- FICC intends to improve its Required Fund Deposit calculation method for the GSD Clearing Fund via the PD Charge.

- This charge is designed to address the risks FICC faces from variations in a Member’s Margin Portfolio between collection periods of the Member's Required Fund Deposits.

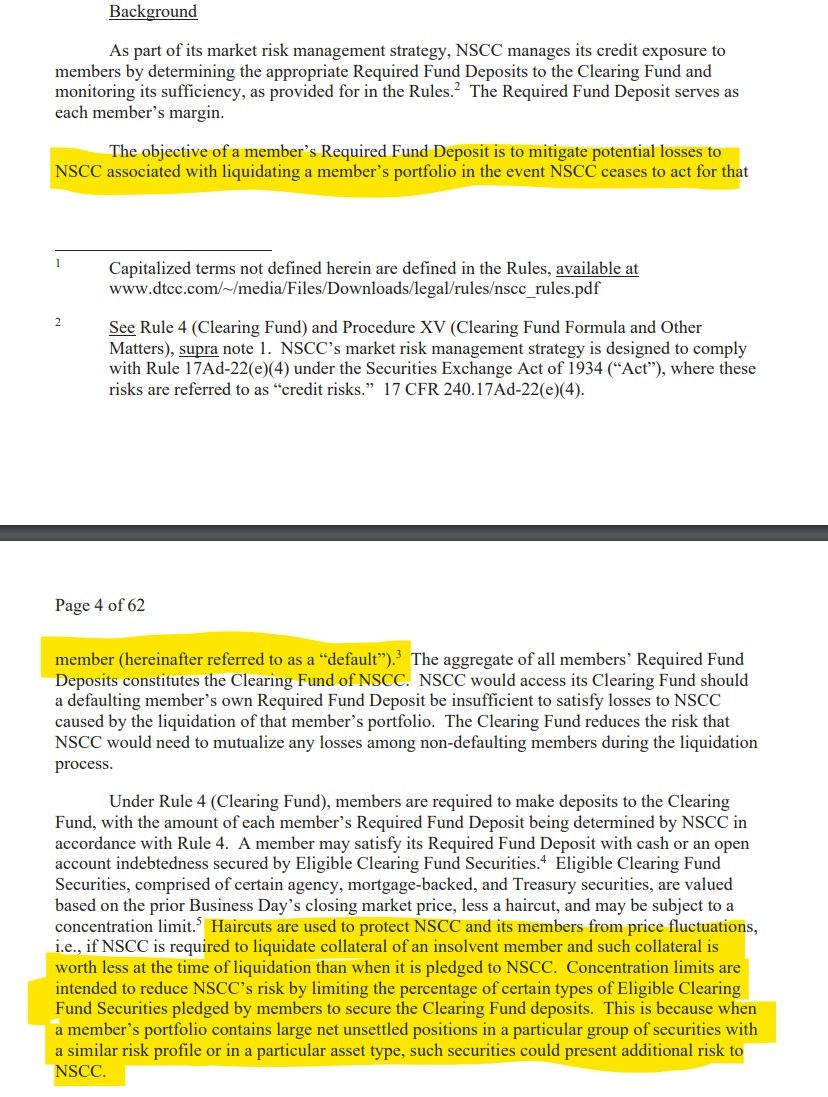

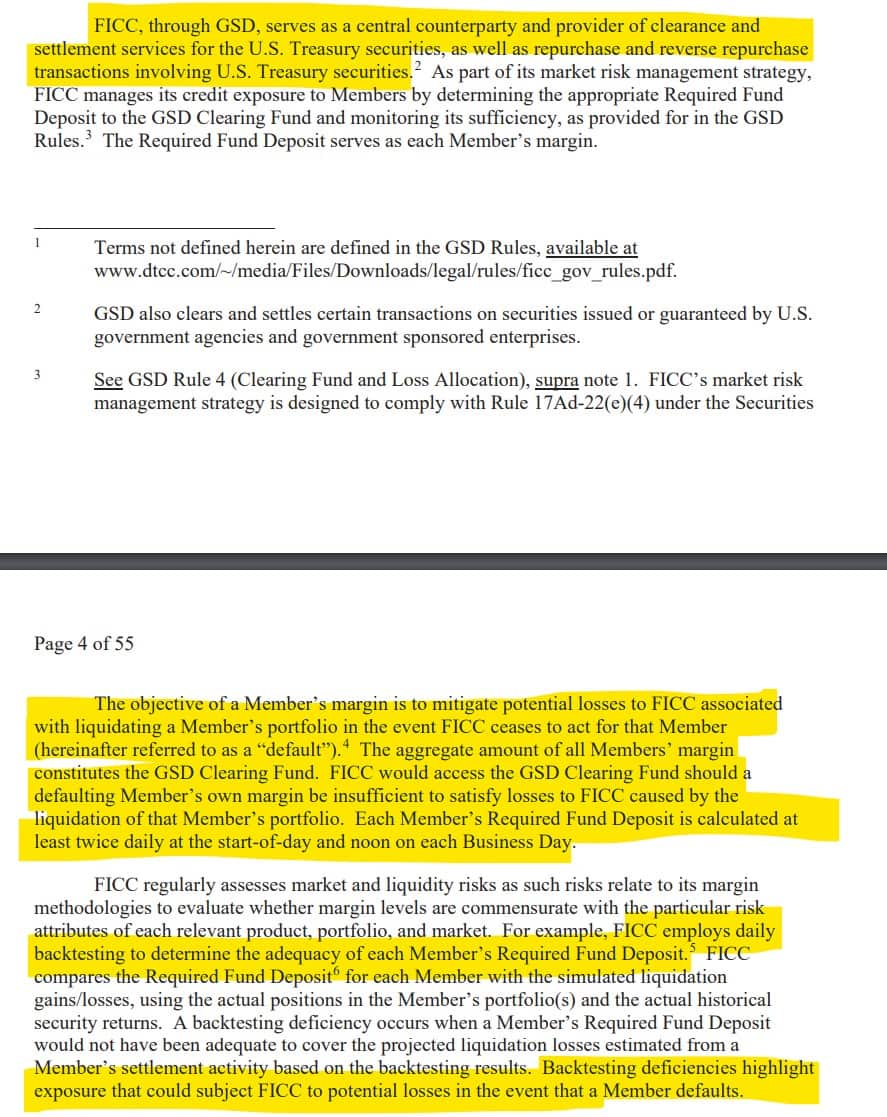

Background:

Wut Mean?:

- FICC, via Government Securities Division (GSD), acts as a central counterparty and offers clearance and settlement services for U.S. Treasury securities and related transactions. GSD also handles certain transactions for securities backed by U.S. government agencies and sponsored enterprises.

- FICC uses Required Fund Deposits to the GSD Clearing Fund as a measure to manage its credit exposure to members. This deposit acts as a margin for each member.

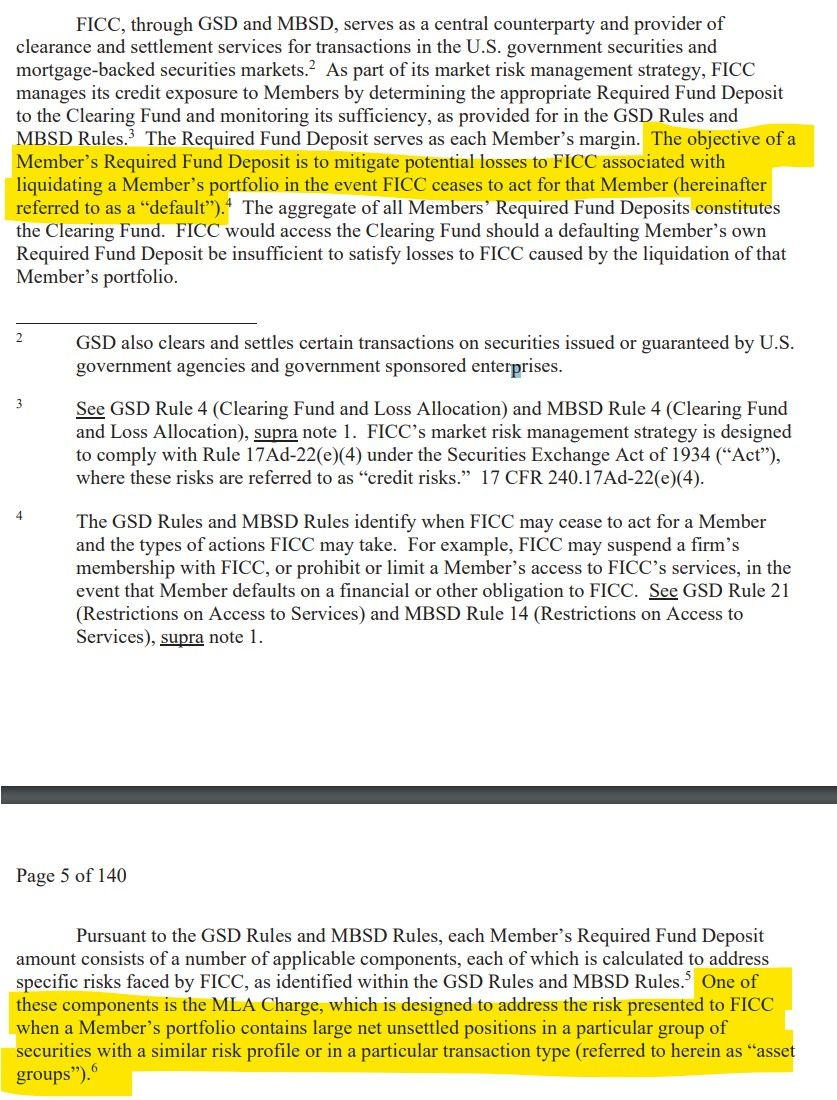

- The primary goal of this margin is to cushion potential FICC losses if they need to liquidate a Member's portfolio due to a default. All members' margins together make up the GSD Clearing Fund. If a defaulting member's margin isn't enough to cover losses, FICC would utilize the GSD Clearing Fund.

- FICC updates the Required Fund Deposit for each member at least twice a day. They employ backtesting to check the deposit's adequacy. In instances where the deposit isn't enough to cover hypothetical liquidation losses based on historical data, it's seen as a deficiency. FICC examines causes of repeated backtesting deficiencies and checks if multiple members face deficiencies due to similar reasons.

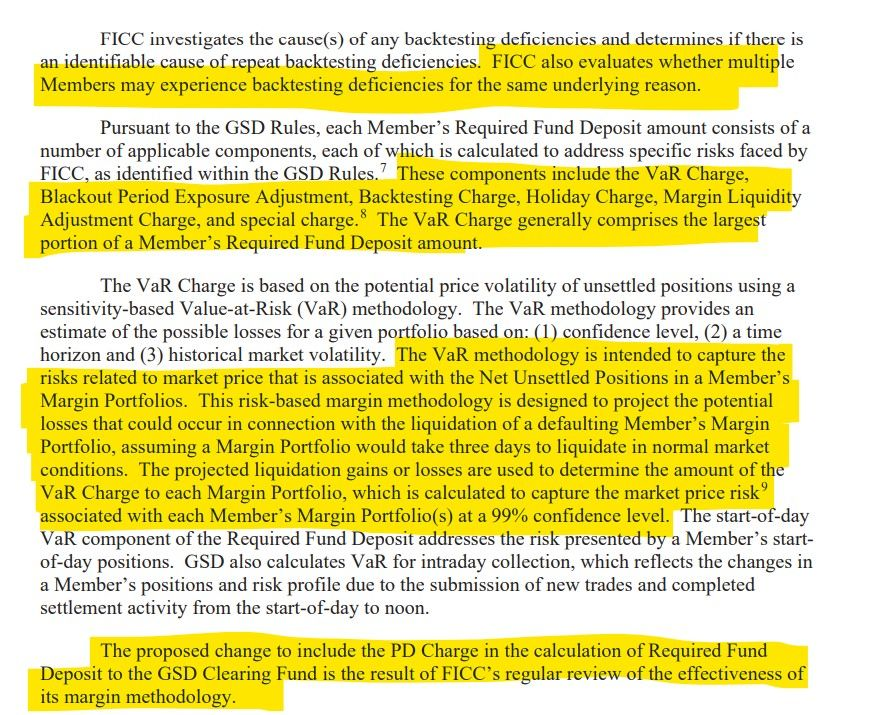

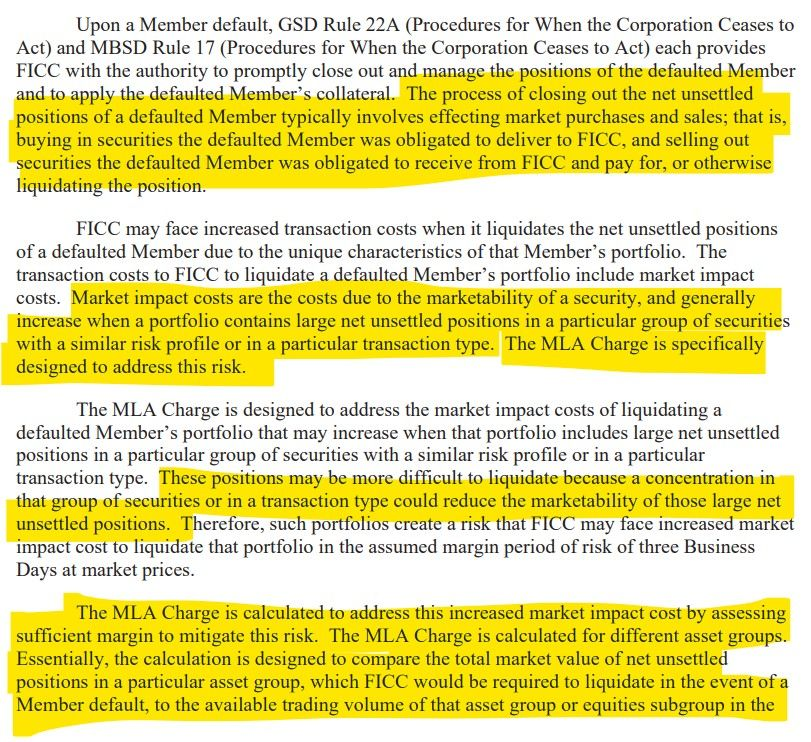

- The GSD Rules outline various components for calculating each Member's Required Fund Deposit, addressing specific risks FICC may face. Components include the VaR Charge, Blackout Period Exposure Adjustment, and others. The VaR Charge, a significant portion of the deposit, is based on the sensitivity-based Value-at-Risk (VaR) methodology. This methodology aims to predict possible losses from liquidating a defaulting member's portfolio within normal market conditions in three days.

- FICC's addition of the PD Charge to the Required Fund Deposit calculation is a result of its ongoing review to ensure its margin methodology's efficacy.

What is changing:

The PD Charge is designed to capture variability in the VaR Charge collected from the Member over the look back period. FICC believes the proposed PD Charge would help mitigate the risks posed to FICC by the variability of clearing activity submitted to GSD throughout the day by measuring the historical period-over-period increases in the VaR Charge of a Member over a given time period.

Wut Mean?:

Introduction of the PD Charge:

- The Portfolio Differential (PD) Charge is a new measure proposed by FICC to address the variability in the Value-at-Risk (VaR) Charge collected from Members.

- The PD Charge aims to cover the potential exposure to FICC from trades executed throughout the day by considering the historical fluctuations in the VaR Charge over a given period.

Reason for the PD Charge:

- A Member’s Margin Portfolio can change significantly intraday due to trades they execute.

- These trades, once guaranteed by FICC, could lead to a gap in coverage because of large un-margined intraday fluctuations in the portfolio.

- The PD Charge is designed to bridge this gap and reduce exposure, helping to prevent backtesting deficiencies.

How the PD Charge Works:

- The charge increases a Member’s Required Fund Deposits based on their historical trading activity.

- It's calculated twice a day and, if applicable, is included in each Member’s Required Fund Deposit.

- Specifically, the PD Charge examines historical changes in a Member’s VaR Charge over a minimum of 100 days and uses an exponentially weighted moving average (EWMA) to stress more recent changes. A multiplier between 1 and 3, determined by FICC based on backtesting, is applied.

- This charge is designed to tackle the risks FICC might face from un-margined changes in a Member’s portfolio due to trading activities that occur during coverage gaps.

Definition and Rule Changes:

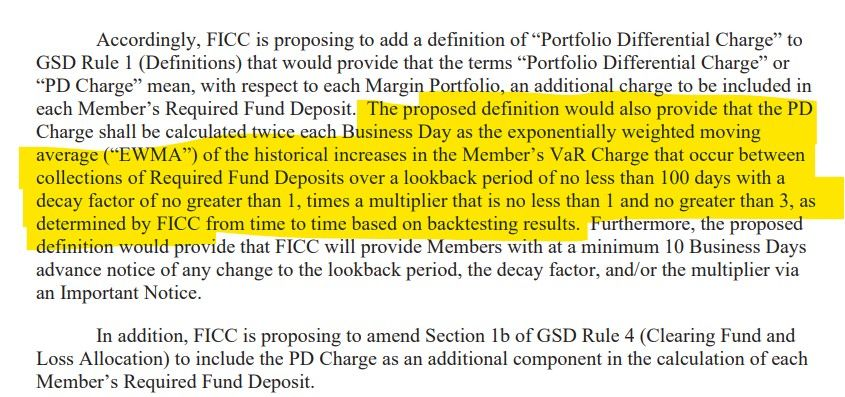

- FICC plans to add a definition for “Portfolio Differential Charge” or “PD Charge” to the GSD Rule 1 (Definitions). This definition explains that the PD Charge is an additional amount to be added to each Member’s Required Fund Deposit, calculated twice daily.

- FICC also proposes to adjust Section 1b of GSD Rule 4 (Clearing Fund and Loss Allocation) to include the PD Charge as an added component in the computation of each Member’s Required Fund Deposit.

Notices and Adjustments:

- FICC will inform Members at least 10 business days in advance about any modifications to the lookback period, decay factor, or the multiplier through an Important Notice.

- Initially, FICC will use a 100-day look-back period with a decay factor of 0.97. Adjustments might be made based on market conditions, but any such changes will undergo FICC's model governance process and be announced.

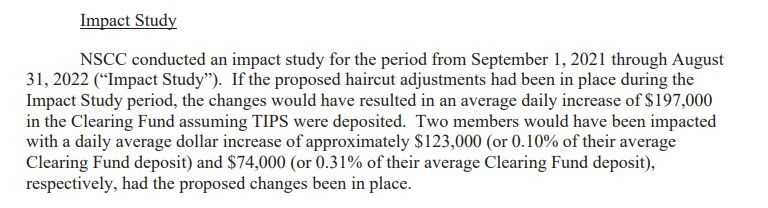

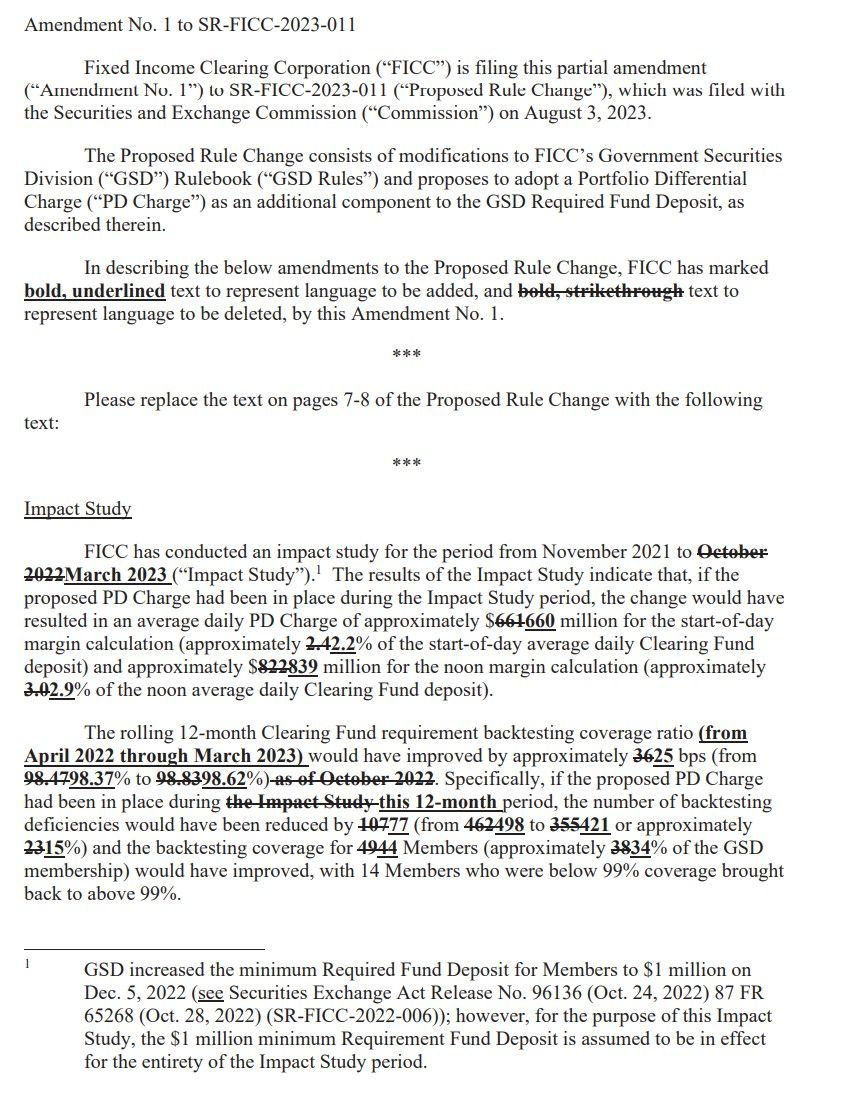

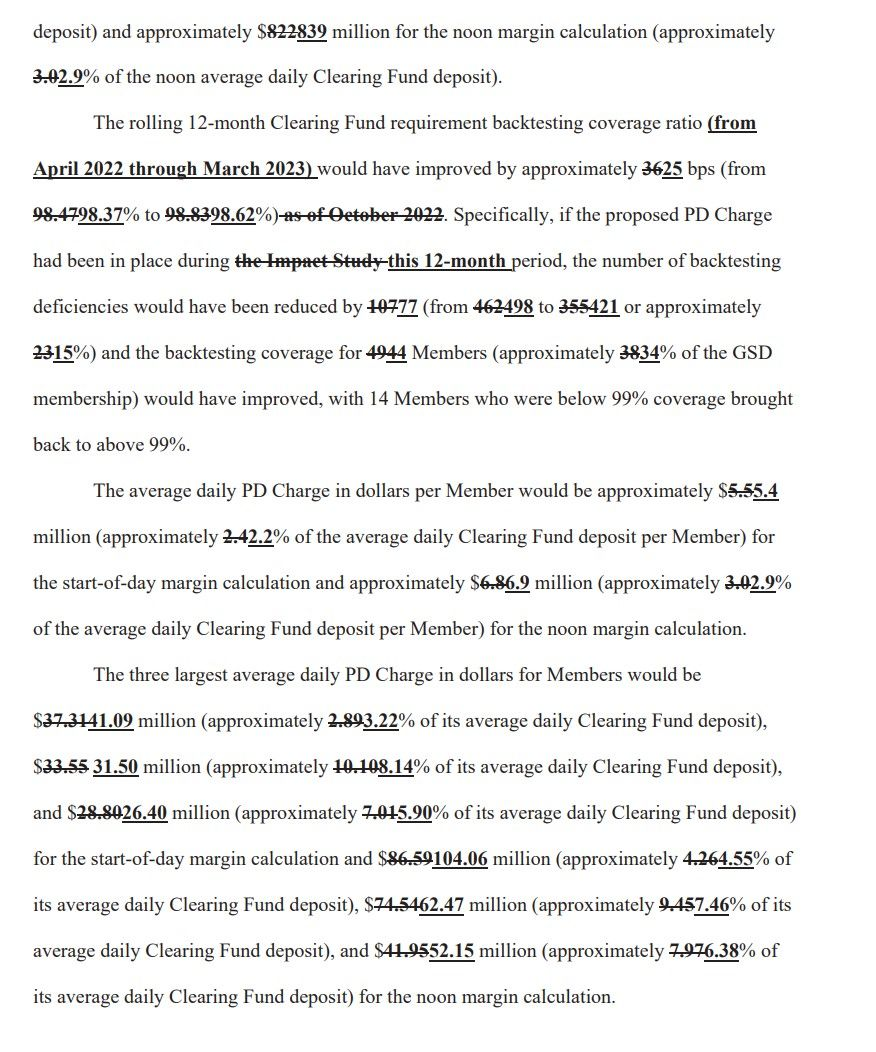

Impact Study:

Amendment No. 1 to SR-FICC-2023-011 (they had to revise the impact study):

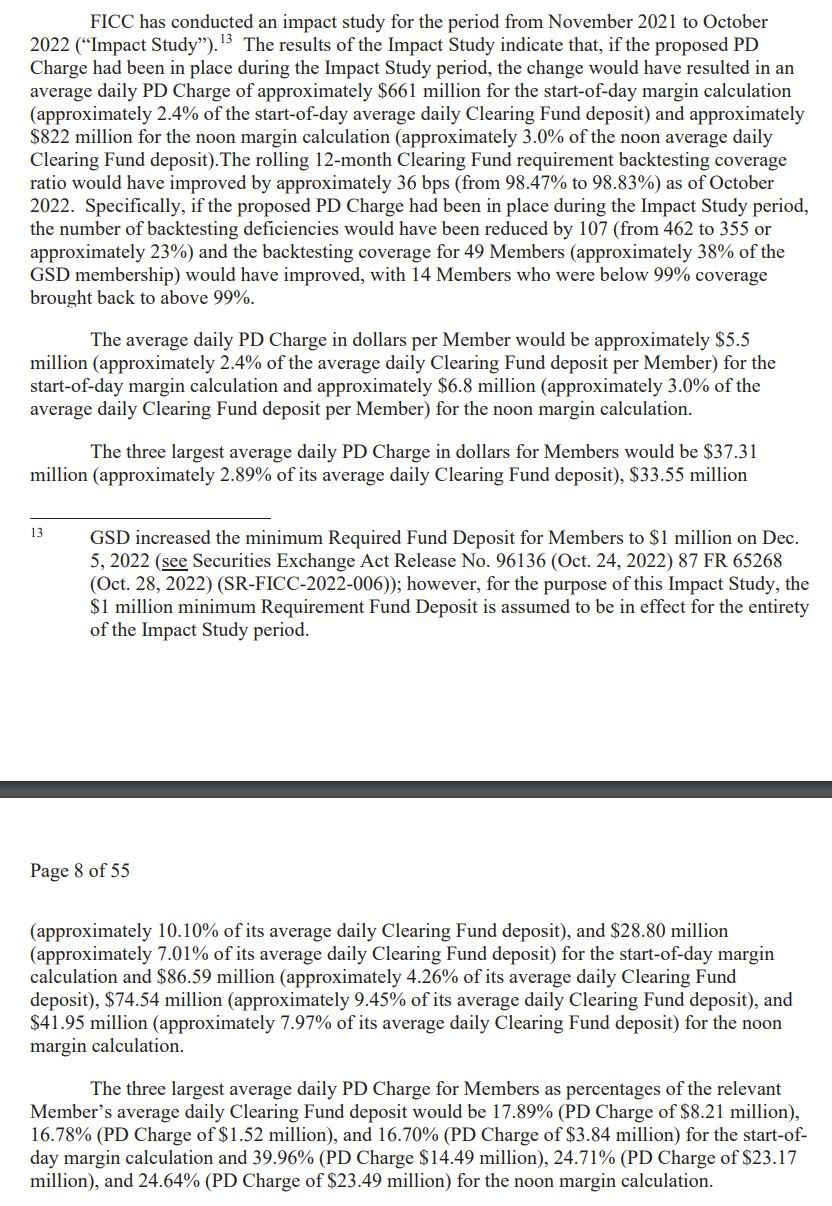

1. Average daily PD Charge:

- Start-of-day: $661 million (2.4% of average daily Clearing Fund deposit).

- Noon: $822 million (3.0% of noon average daily Clearing Fund deposit).

2. Clearing Fund backtesting improvement: 36 bps (from 98.47% to 98.83%).

3. Backtesting deficiencies reduced by 107 (23% reduction, from 462 to 355).

4. 49 Members (38% of GSD membership) had improved backtesting coverage, with 14 brought back to above 99% coverage.

5. Average daily PD Charge per Member:

- Start-of-day: $5.5 million (2.4%).

- Noon: $6.8 million (3.0%).

6. Three largest average daily PD Charges for Members in dollars:

- Start-of-day: $37.31 million, $33.55 million, and $28.80 million.

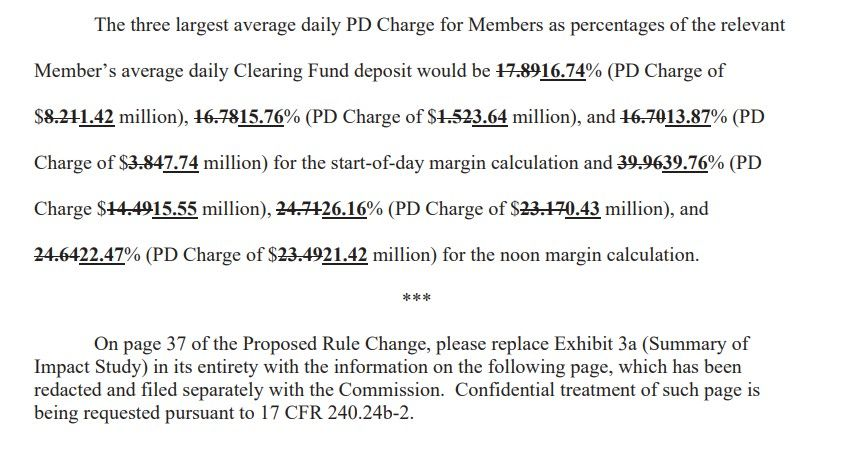

7. Three largest PD Charges as percentages of Member’s deposit:

- Start-of-day: 17.89%, 16.78%, and 16.70%.

- Noon: 39.96%, 24.71%, and 24.64%.

1. Average daily PD Charge:

- Start-of-day: $660 million (2.2%).

- Noon: $839 million (2.9%).

2. Clearing Fund backtesting improvement: 25 bps (from 98.37% to 98.62%).

3. Backtesting deficiencies reduced by 77 (15% reduction, from 498 to 421).

4. 44 Members (34% of GSD membership) had improved backtesting coverage, with 14 brought back to above 99% coverage.

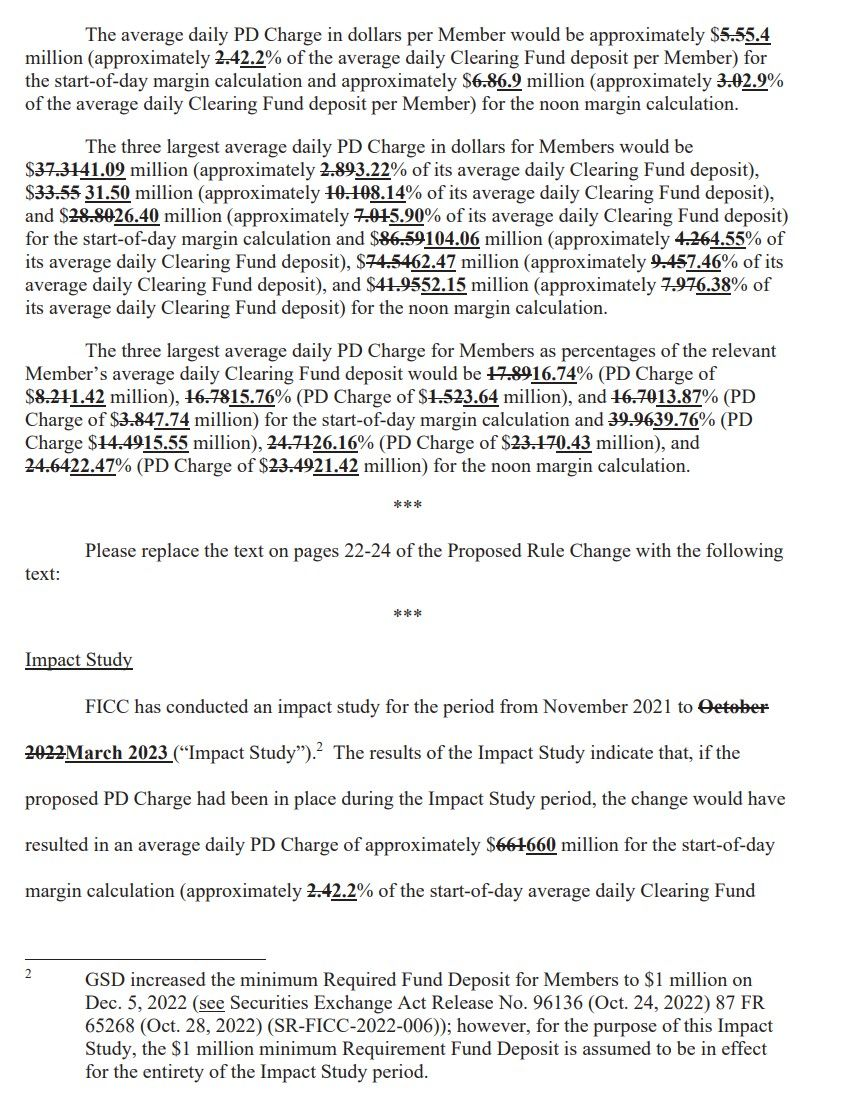

5. Average daily PD Charge per Member:

- Start-of-day: $5.4 million (2.2%).

- Noon: $6.9 million (2.9%).

6. Three largest average daily PD Charges for Members in dollars:

- Start-of-day: $41.09 million, $31.50 million, and $26.40 million.

- Noon: $104.06 million, $62.47 million, and $52.15 million.

7. Three largest PD Charges as percentages of Member’s deposit:

- Start-of-day: 16.74%, 15.76%, and 13.87%.

- Noon: 39.76%, 26.16%, and 22.47%.

Notable Differences

Duration of the Studies:

- The original Impact Study covered a period from November 2021 to October 2022, making it a 12-month study.