Hester Peirce Statement on SEC's Short Sale Disclosure: "Because a narrower rule leveraging existing reporting requirements could have brought more meaningful transparency at lower costs, I cannot support this recommendation."

Source: https://www.sec.gov/news/statement/peirce-statement-short-sale-101323

Thank you, Mr. Chair. In 2010, Congress directed the Commission to prescribe rules providing for the public disclosure of aggregate short sale position data on at least a monthly basis.[1] The final rule that we are considering today, however, goes well beyond what Congress requires. Because a narrower rule leveraging existing reporting requirements could have brought more meaningful transparency at lower costs, I cannot support this recommendation.

Enhancing the quality and quantity of short sale information available in the market can be beneficial and is something I support. The issue with this rule is that it does not adequately consider all the costs associated with its implementation. The costs are not merely the operational and financial costs to providers of the information, but also the potential costs to market quality. Short selling is important to the healthy functioning of our markets: It allows investors to hedge risks; it enables market participants to be compensated for their vigilance in spotting negative behavior in the markets, including wrongdoing by issuers; and it allows market makers to hedge their positions so they can provide consistent liquidity to investors. Increasing transparency of short-selling activity can help investors better understand market sentiment, but it also can raise the cost for market participants to engage in short-selling in the first place. The result could be bad for the markets: unhedged risks, more fraud, and less liquidity.

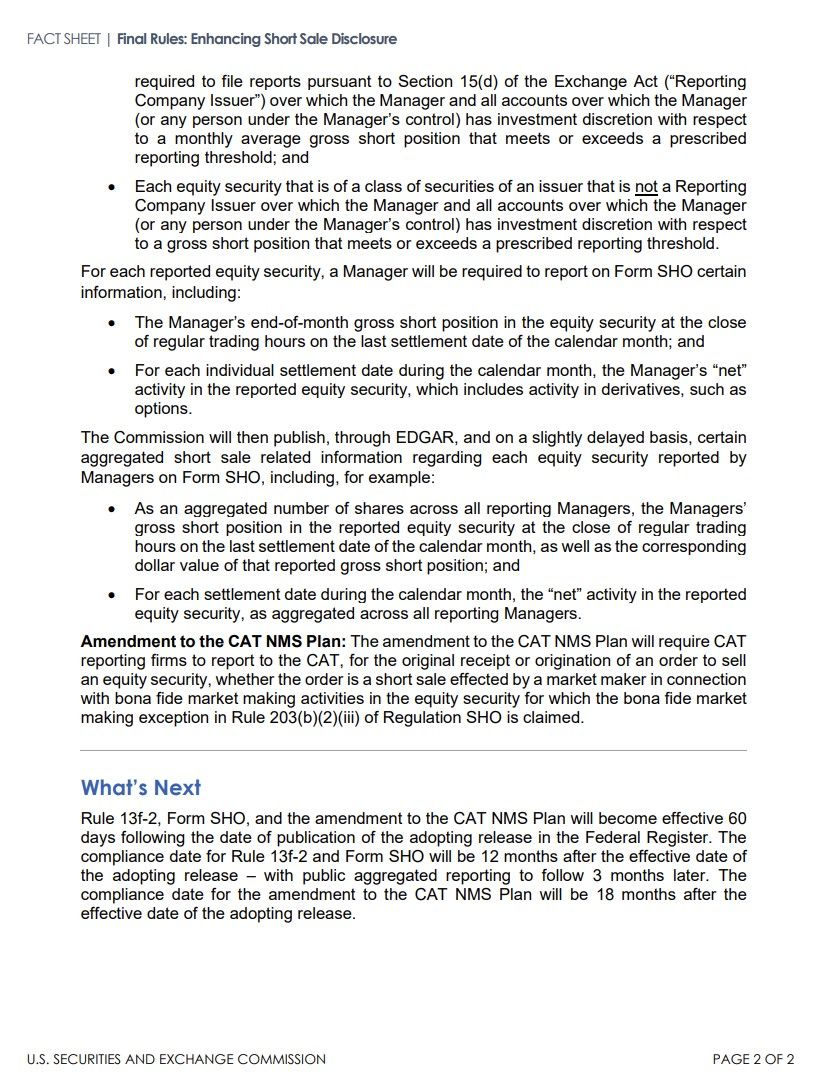

The final rule requires institutional investment managers who exceed at least one of the rule’s thresholds for short positions in a particular security in the preceding month to file new Form SHO, which consists of basic information about the reporting entity and two tables. Table 1 requires, for each security where the manager’s short position exceeded the relevant threshold, that the manager report the end of month gross short position in both number of shares and in dollar amount. On Table 2, for each security reported on Table 1, the Manager must report the net change in its short position for each trading day of the month. Managers will be required to file Form SHO within fourteen days of the end of the calendar month, after which the Commission will aggregate and publish the data, generally by the end of the month in which it received the data.

The statutory mandate—which requires periodic, but not daily, aggregate reporting—appears to reflect Congress’ attempt to strike an appropriate balance. The information required by Table 1 satisfies the Congressional mandate. The statute does not require the Table 2 information. Indeed, even though an earlier version of the legislation required daily reports on short sales to the Commission,[2] the statute as enacted does not mention daily short sale information.

The Commission could have chosen a less burdensome approach. Commission and self-regulatory organization rules already require market participants to report information related to short sales and short positions. The Commission could have taken an approach that leveraged or consolidated those existing reporting requirements in a way that reduced or eliminated the costs of duplicative (and potentially confusing)[3] reporting of similar data.

FINRA collects aggregate short interest information in individual securities on a bimonthly basis from broker-dealers. The relevant listing exchange or FINRA publishes the data with a two-week lag. As suggested by commenters, the Commission could have built on this system by requiring weekly reporting to FINRA and shortening the dissemination lag to one-week.[4] This approach would have provided timelier information to the public than the rule we are adopting today. The information might have been more reliable.[5] And, it could have been enhanced to provide additional information to the market.[6]

The release is too cavalier in its treatment of the risks attendant from capturing detailed daily short sale related data at the Manager level. The information to be reported, particularly as related to daily net changes in a Manager’s short positions, is highly sensitive. As one commenter explained, “small daily fluctuations do not have significant regulatory value, but their disclosure exposes us to unlimited risk of commercial harm.”[7] Exposure of this data could lead to retaliation and the compromise of valuable proprietary trading strategies.[8] The Commission does not currently intend for these data to see the light of day, but that intention offers little comfort to Managers. Exposure could come through a breach of EDGAR. After all, increasing the value of information reported to EDGAR only makes it more attractive to hackers, who will be willing to invest more money and effort into gaining access to the data. Exposure also could come through a change of heart. The recommendation before us reflects a prudent determination not to publicly disseminate non-aggregated Manager-level data (either on an anonymous or an attributed basis). Once we start collecting these data, however, it will be extraordinarily easy for the Commission to flip the switch to disseminate this information to the public. The temptation and political pressure to do so will likely be great, especially after significant market events, particularly as proponents would argue that doing so would impose no additional direct costs on market participants. The Commission’s feeble rationale for including Table 2 in Form SHO—excluding it “would not further the goal of enhancing the transparency of short-sale related data”[9]—could as easily be used to justify the publication of the data.

Although I cannot support today’s rulemaking, I appreciate that it reflects the staff’s efforts to address a number of concerns raised during the comment period. Many thanks to the Division of Trading and Markets, the Division of Economic and Risk Analysis, and the Office of General Counsel, as well as other offices throughout the Commission. I enjoyed our discussions and look forward to working with you during implementation.

I have a number of questions:

Why is daily data publicly disseminated a month or more after short sale positions are opened or covered more useful to investors than weekly data disseminated with a one-week lag, which is what we could have gotten under an enhanced FINRA rule?

What do we anticipate the compliance costs will be in the first year and then in each subsequent year? What, if anything, can we do to help contain those costs?

How have we taken into account the cost of requiring Managers to daily monitor their positions? As one commenter explained, “Managers’ reporting systems generally are not equipped to monitor short positions and related transactions that affect those positions on a daily basis.”[10]

How important were data generated under temporary interim rule 10a-3T, which the Commission adopted in October 2008, to the fashioning of this final rule? Are you concerned that relying on data from that unusual time period fifteen years ago might be problematic?

Managers will file Form SHO on EDGAR. Given the sensitivity and value of the information contained in the Form, commenters raised concerns about the vulnerability of the data to attack. While the Commission has been working to strengthen and improve EDGAR, the Commission also is increasing the role that EDGAR plays.

Why is EDGAR the right system for this information?

What assurance can you give to future filers about the safety of their information?

Will managers have to report with respect to foreign equity securities and foreign issuers, even though such issuers have limited U.S. jurisdictional ties and in many cases are subject to short-sale reporting regulations in their home jurisdictions? If so, why?

Commenters suggested limiting the rule’s scope to equity securities of U.S. reporting company issuers. The release acknowledges that information on non-reporting issuers will be more difficult to obtain and report. The effects of reporting regarding short interest in these issuers could be particularly pronounced, and discouraging short-selling in the over-the-counter market could worsen market quality. What are the Commission’s plans for assessing whether the application of the rule to these securities has a net positive effect on the quality of the over-the-counter market?

The economic analysis acknowledges that fear of triggering reporting thresholds could deter market makers from providing liquidity during volatile times. How is the staff planning to monitor the effect the rule is having on liquidity?

What has Hester Upset?

Fact Sheet

Press Release:

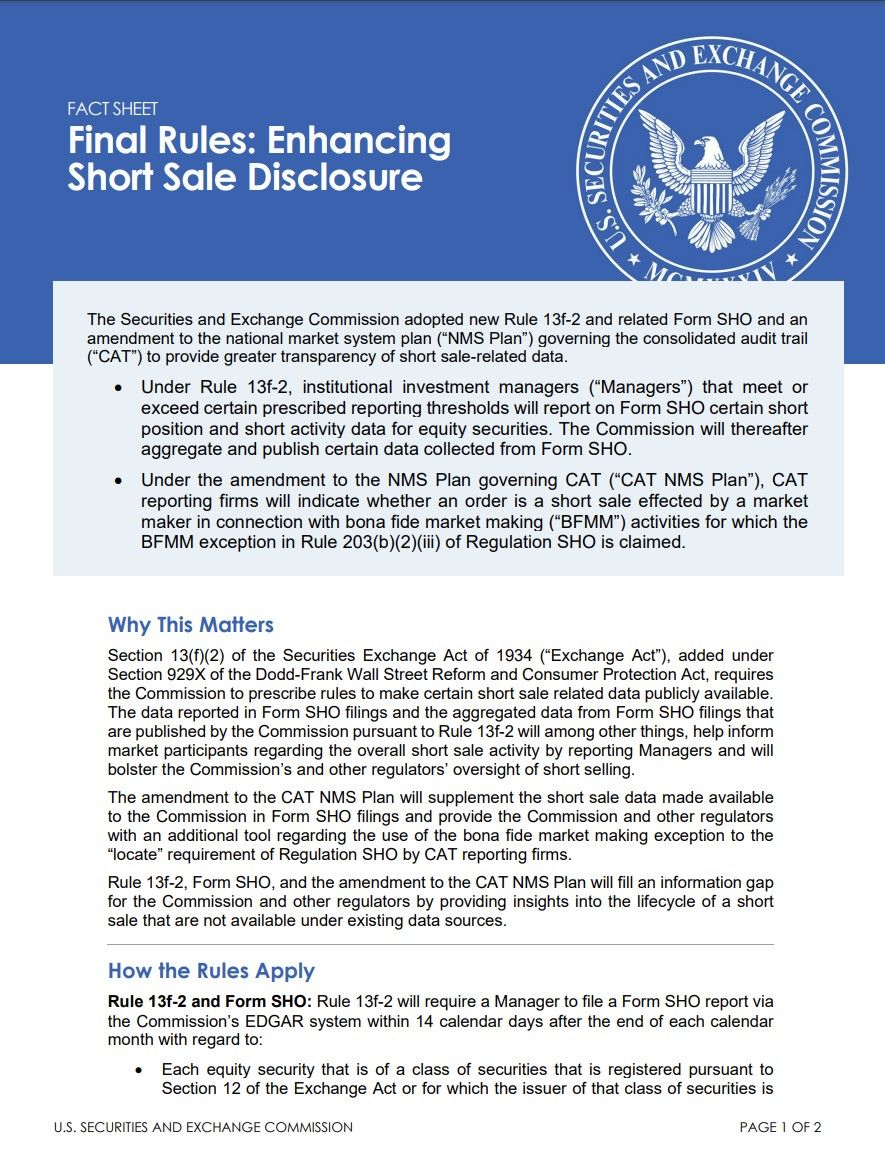

The Securities and Exchange Commission today adopted new Rule 13f-2 to provide greater transparency to investors and other market participants by increasing the public availability of short sale related data. Congress directed the SEC in Section 929X of the Dodd-Frank Act of 2010 to promulgate rules to make certain short sale data publicly available.

“In the wake of the 2008 financial crisis, Congress directed the SEC to enhance the transparency of short selling of equity securities,” said SEC Chair Gary Gensler. “Today’s adoption will promote greater transparency about short selling both to regulators and the public. This rule addresses Congress’s mandate and improves upon existing sources of short sale-related data in the equity markets. Given past market events, it’s important for the Commission and the public to know more about short sale activity in the equity markets, especially in times of stress or volatility.”

Specifically, Rule 13f-2 will require institutional investment managers that meet or exceed certain thresholds to report on Form SHO specified short position data and short activity data for equity securities. The Commission will aggregate the resulting data by security, thereby maintaining the confidentiality of the reporting managers, and publicly disseminate the aggregated data via EDGAR on a delayed basis. This new data will supplement the short sale data that is currently publicly available.

Relatedly, the Commission today also adopted an amendment to the National Market System Plan (NMS Plan) governing the consolidated audit trail (CAT). The amendment to the NMS Plan governing the CAT (CAT NMS Plan) will require each CAT reporting firm that is reporting short sales to indicate when it is asserting use of the bona fide market making exception in Rule 203(b)(2)(iii) of Regulation SHO.

The adopting release for Rule 13f-2 and related Form SHO, as well as the notice of the amendment to the CAT NMS Plan, will be published in the Federal Register. The final rule, Form SHO, and the amendment to the CAT NMS Plan will become effective 60 days after publication of the adopting release in the Federal Register. The compliance date for Rule 13f-2 and Form SHO will be 12 months after the effective date of the adopting release, with public aggregated reporting to follow three months later, and the compliance date for the amendment to the CAT NMS Plan will be 18 months after the effective date of the adopting release.

TLDRS:

- SEC Adopts Rule to Increase Transparency Into Short Selling and Amendment to CAT NMS Plan for Purposes of Short Sale Data Collection.

- Hester Peirce Statement on SEC's Short Sale Disclosure: "Because a narrower rule leveraging existing reporting requirements could have brought more meaningful transparency at lower costs, I cannot support this recommendation."

- Rule 13f-2 and Form SHO: Rule 13f-2 will require a Manager to file a Form SHO report via the Commission’s EDGAR system within 14 calendar days after the end of each calendar month with regard to:

- Each equity security that is of a class of securities that is registered pursuant to Section 12 of the Exchange Act or for which the issuer of that class of securities is required to file reports pursuant to Section 15(d) of the Exchange Act (“Reporting Company Issuer”) over which the Manager and all accounts over which the Manager (or any person under the Manager’s control) has investment discretion with respect to a monthly average gross short position that meets or exceeds a prescribed reporting threshold

- Each equity security that is of a class of securities of an issuer that is not a Reporting Company Issuer over which the Manager and all accounts over which the Manager (or any person under the Manager’s control) has investment discretion with respect to a gross short position that meets or exceeds a prescribed reporting threshold.

For each reported equity security, a Manager will be required to report on Form SHO certain information, including:

- The Manager’s end-of-month gross short position in the equity security at the close of regular trading hours on the last settlement date of the calendar month

- For each individual settlement date during the calendar month, the Manager’s “net” activity in the reported equity security, which includes activity in derivatives, such as options.

- The Commission will then publish, through EDGAR, and on a slightly delayed basis, certain aggregated short sale related information regarding each equity security reported by Managers on Form SHO.