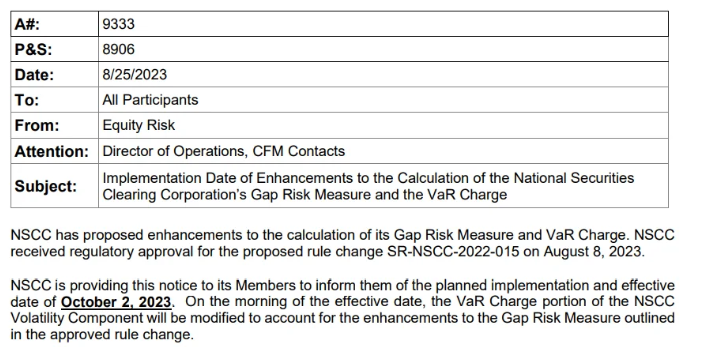

NSCC is providing this notice to its Members to inform them of the planned implementation and effective date of October 2, 2023. Why? IDIOSYNCRATIC RISK!

Remember, VaR tinkers with the mechanics that would have defaulted Robinhood, Instinet, & Others 1/28/21. I believe this is a precursor to MOASS.

Source: https://www.dtcc.com/-/media/Files/pdf/2023/8/25/a9333.pdf

Previous post: MOASS Prediction: October 24, 2023 (a Tuesday):

- The NSCC approved Enhancements to the Gap Risk Measure & the VaR Charge.

- VaR tinkers with the mechanics that would have defaulted Robinhood & Others 1/28/21.

- The NSCC, previously saved them by sacrificing retail, in allowing Robinhood and others to alter their margin charges and freezing the buy button.

Wut Mean?:

- The gap risk charge will now be added to a member's total VaR Charge whenever it applies. Previously, it only replaced the VaR Charge when it was the largest of three calculations. This addition improves the ability to handle unique risks.

- The gap risk charge will now consider the two largest positions in a portfolio instead of just the single largest one. This means the charge could apply when the combined value of these two largest positions exceeds a certain concentration threshold. This change offers better coverage for potential concurrent gap events in two major positions.

- The way the gap risk haircut (a percentage reduction) is determined will be revised. The minimum haircut for the largest position will be reduced from 10% to 5%, and a new minimum of 2.5% will be set for the second-largest position. This change in methodology is to ensure an appropriate margin level.

- NSCC will modify the criteria for ETF positions that are excluded from the gap risk charge. Instead of just excluding "non-index" positions, NSCC will exclude "non-diversified" positions, factoring in characteristics like the nature of the index the ETF tracks or whether the ETF is unleveraged. This change aims to be more precise about which ETFs are prone to gap risk and should improve transparency for members.

- Regarding the gap risk charge for securities financing transactions cleared by NSCC, the methodology of which already includes the gap risk charge as an additive component to margin and which would not change as a result of this proposal, (ii) to make clear that the gap risk charge applies to Net Unsettled Positions, (iii) to remove an unnecessary reference, (iv) to reflect that NSCC considers impact analysis when determining and calibrating the concentration threshold and gap risk haircuts, and (v) to make other technical changes for clarity).

Why is it changing? It's all about the idiosyncratic risk!:

- NSCC's proposed changes approved for the gap risk charge, ensuring the collection of adequate margin to address risks from members’ portfolios.

- Based on provided confidential data and impact study, the changes offer better margin coverage than the current methodology.

- Making the gap risk charge additive should help NSCC address more idiosyncratic risk scenarios in concentrated portfolios compared to the existing methodology.

- Adjusting the gap risk calculation for the two largest positions with two separate haircuts, based on backtesting and impact analysis, allows NSCC to cover risks from simultaneous gap moves in multiple concentrated positions.

- Changing criteria for ETFs in the gap risk charge (from non-index to non-diversified) enhances NSCC's precision in determining which ETFs are susceptible to gap risk events, improving risk exposure accuracy.

- The Proposed Rule Change equips NSCC to better manage its exposure to portfolios with identified concentration risk, hence limiting its risk exposure during member defaults.

- NSCC's rule ensures uninterrupted operation in its critical clearance and settlement services, even during a member default, by having adequate financial resources.

- The changes minimize the chance of NSCC tapping into the mutualized clearing fund, thereby reducing non-defaulting members' risk exposure to shared losses.

- The Commission believes these proposed changes will help NSCC safeguard securities and funds in its custody or control, aligning with Section 17A(b)(3)(F) of the Act.

The approved rule aims to address the potential increased idiosyncratic risks NSCC might face, especially regarding the liquidation of a risky portfolio during a member default.

- After reviewing NSCC’s analysis, the Commission agrees that the new rule would result in improved backtesting coverage, reducing credit exposure to members.

- The Commission asserts that this rule will empower NSCC to manage its credit risks more effectively, allowing it to adapt to backtesting performance issues, market events, structural changes, or model validation findings.

- This proactive management ensures NSCC can consistently collect enough margin to cover potential exposures to its members.

- The goal is to produce margin levels that align with the risk attributes of these concentrated holdings, especially securities more vulnerable to gap risk events.

- The rule would enhance NSCC's ability to recognize and produce margins that match the idiosyncratic risks and attributes of portfolios that meet the concentration threshold.

- Broadening the gap risk charge to an additive feature and focusing on the two largest non-diversified positions will help NSCC better manage the idiosyncratic risks tied to concentrated portfolios.

- Given the additive nature of the gap risk charge, the Commission agrees that the adjustments to its calculation, like establishing floors for gap risk haircuts for the two largest positions, are aptly designed to handle NSCC’s idiosyncratic risks exposure during member defaults.

- Introducing specific criteria to determine which securities fall under the gap risk charge will enable NSCC to pinpoint those more prone to idiosyncratic risks, ensuring ETFs identified as non-diversified are included.

Implementation:

Today's update tells us 10/2!

So what should these changes mean?:

- Increased Margin Requirements: With the changes in the methodology, members should face higher margin requirements. The addition of the gap risk charge to the VaR Charge (as opposed to it only replacing the VaR charge when it's the largest of three calculations) would mean that members should be required to deposit more funds to NSCC to cover this risk.

- Multiple Significant Positions Impact: Previously, the gap risk charge considered only the largest non-index position. By considering the two largest positions in a portfolio, the margin requirements should rise for members who have significant short positions in multiple securities, especially if those securities are prone to volatile price movements....

- Revised Haircut Percentages: The change in haircut percentages implies concerns about the risk. The lowered percentages (from 10% to 5% for the largest position and a new 2.5% for the second-largest position) mean the gap risk charge should be applied more frequently.

- New Criteria for ETFs: By moving from "non-index" to "non-diversified" as the criteria for exclusion from the gap risk charge, there's a more refined approach to evaluating which ETFs are prone to gap risk. This should impact members who previously used certain ETF positions as a strategy to manage their margins...

- Increased Transparency: Improved transparency in terms of which ETFs are prone to gap risk means that members can make more informed decisions. However, it also implies that any loopholes or strategies that were previously employed might no longer be valid, leading to strategy changes or potential increased costs for some members.

How does this lead to MOASS?:

- The changes should lead to higher margin requirements for those with short positions in volatile stocks like GameStop. The higher the costs, the more pressure on short sellers to close their positions, especially if they face liquidity challenges.

- If short sellers can't meet their margin requirements, they'll be forced to buy back the shares to close their positions, leading to a surge in demand and subsequently, a rise in share price.

- As the stock price rises due to forced buybacks, other short sellers face further margin calls, creating a snowball effect where more short sellers are forced to buy back shares, pushing the price up even further until lift off...

Oh yeah:

- They are REALLY concerned about idiosyncratic risk.

https://home.treasury.gov/system/files/261/FSOC2021AnnualReport.pdf

Additional Background:

Robinhood, Imstinet, & Other Brokers Would Have Defaulted January 28, 2021 - The NSCC, as an enabler, saved them, while sacrificing retail, in allowing them to alter their margin charges by freezing stock buying - top priority: protecting too-big-to-fail clearinghouse - Retail's fault the NSCC didn't prepare (and anything by ringingbells really, the amount of work they have done on this front is herculean and we are all better for it)

TLDRS:

NSCC is providing this notice to its Members to inform them of the planned implementation and effective date of October 2, 2023.

- Remember VaR tinkers with the mechanics that would have defaulted Robinhood, Instinet, & Others 1/28/21.

- The approved rule aims to address the potential increased idiosyncratic risks NSCC might face, especially regarding the liquidation of a risky portfolio during a member default.

- Enhances NSCC's ability to recognize and produce margins that match the idiosyncratic risks and attributes of portfolios that meet the concentration threshold.

- Broadening the gap risk charge to an additive feature and focusing on the two largest non-diversified positions will help NSCC better manage the idiosyncratic risks tied to concentrated portfolios.

- Given the additive nature of the gap risk charge, the Commission agrees that the adjustments to its calculation, like establishing floors for gap risk haircuts for the two largest positions, are aptly designed to handle NSCC’s idiosyncratic risks exposure during member defaults.

- Introducing specific criteria to determine which securities fall under the gap risk charge will enable NSCC to pinpoint those more prone to idiosyncratic risks, ensuring ETFs identified as non-diversified are included.

- Robinhood, Instinet, & Other Brokers Would Have Defaulted January 28, 2021 - The NSCC, as an enabler, saved them, while sacrificing retail, in allowing them to alter their margin charges by freezing stock buying - top priority: protecting too-big-to-fail clearinghouse - Retail's fault the NSCC didn't prepare

- The changes should lead to higher margin requirements for those with short positions in volatile stocks like GameStop. The higher the costs, the more pressure on short sellers to close their positions, especially if they face liquidity challenges.

- If short sellers can't meet their margin requirements, they'll be forced to buy back the shares to close their positions, leading to a surge in demand and subsequently, a rise in share price.

- As the stock price rises due to forced buybacks, other short sellers face further margin calls, creating a snowball effect where more short sellers are forced to buy back shares, pushing the price up even further until lift off...

- MOASS Prediction: anytime after 10/2.

- This prediction is not financial advice in anyway, only an attempt to read tea leaves based on implementation dates.