Prohibition Against Conflicts of Interest in Certain Securitizations prohibiting a sponsor of an asset-backed security (including a synthetic asset-backed security) that would result in conflicts of interest effective February 5, 2024.

Background:

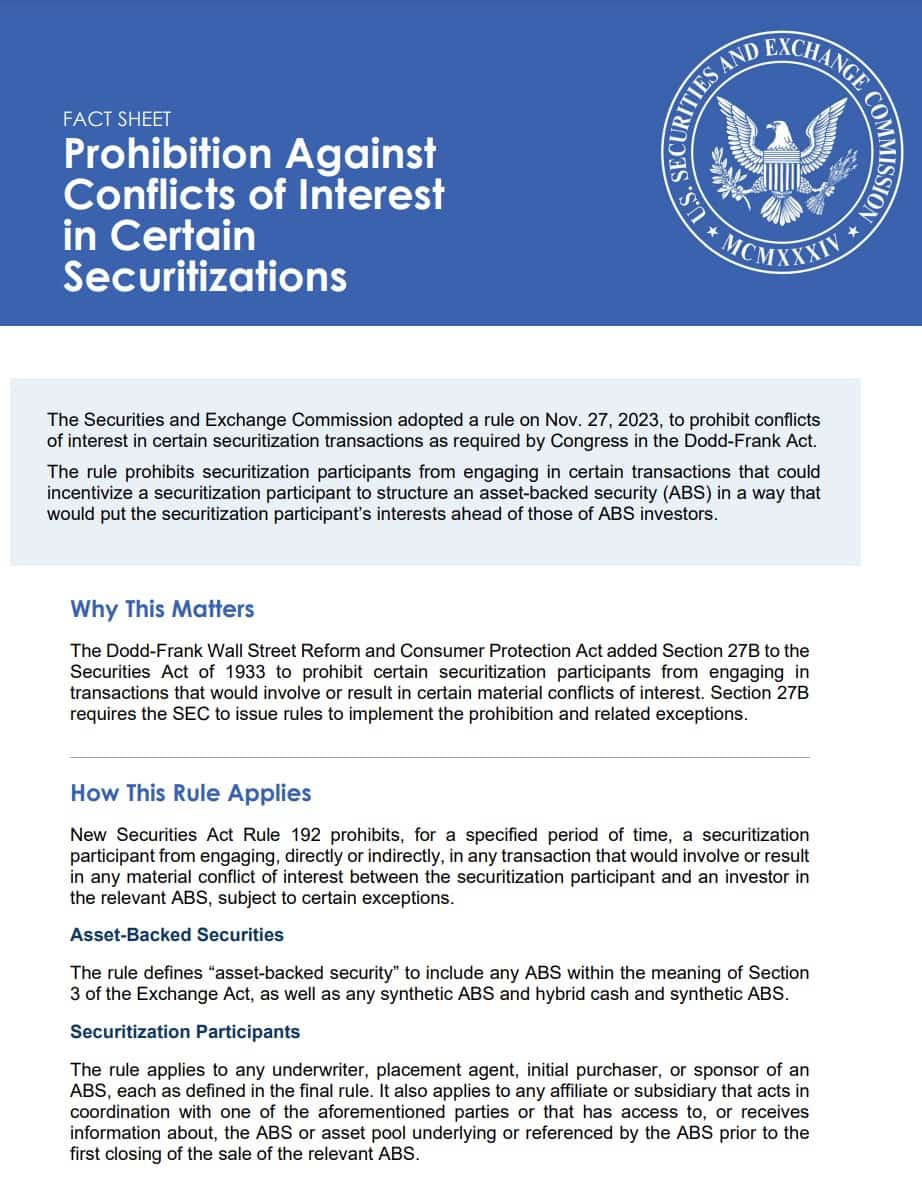

- The SEC proposed new Rule 192 to implement the prohibition in Securities Act Section 27B1 (“Section 27B”), which was added by Section 621 of the Dodd-Frank Act.

- Section 27B(a) provides that an underwriter, placement agent, initial purchaser, or sponsor, or affiliates or subsidiaries of any such entity, of an asset-backed security (“ABS”), including a synthetic asset-backed security, shall not, at any time for a period ending on the date that is one year after the date of the first closing of the sale of the asset-backed security, engage in any transaction that would involve or result in any material conflict of interest with respect to any investor in a transaction arising out of such activity.

- Section 27B(b) further requires that the SEC issue rules for the purpose of implementing the prohibition in Section 27B(a).

- Section 27B(c) provides exceptions from the prohibition in Section 27B(a) for certain risk-mitigating hedging activities, liquidity commitments, and bona fide market-making activities.

Summary of the Proposed Rule:

- Proposed Rule 192 would implement the prohibition in Securities Act Section 27B(a) and, consistent with Section 27B(c), provide exceptions from the prohibition for certain risk mitigating hedging activities, liquidity commitments, and bona fide market-making activities.

- The proposal is intended to target transactions that effectively represent a bet against a securitization and focus on the types of transactions that were the subject of regulatory and Congressional investigations following the financial crisis of 2007-2009.

- Fundamentally, the rule is intended to prevent the sale of ABS that are tainted by material conflicts of interest by prohibiting securitization participants from engaging in certain transactions that could incentivize a securitization participant to structure an ABS in a way that would put the securitization participant’s interests ahead of those of ABS investors.

- By focusing on transactions that effectively represent a “bet” against the performance of an ABS, Rule 192 will provide strong investor protection against material conflicts of interest in securitization transactions while not unduly hindering routine securitization activities that do not give rise to the risks that Section 27B is intended to address.

- The final rule will benefit investors by prohibiting securitization participants from engaging in a short sale of the relevant ABS, purchasing a credit default swap or other credit derivative pursuant to which the securitization participant would be entitled to receive payments upon the occurrence of specified credit events in respect of the relevant ABS.

To achieve these objectives, Rule 192:

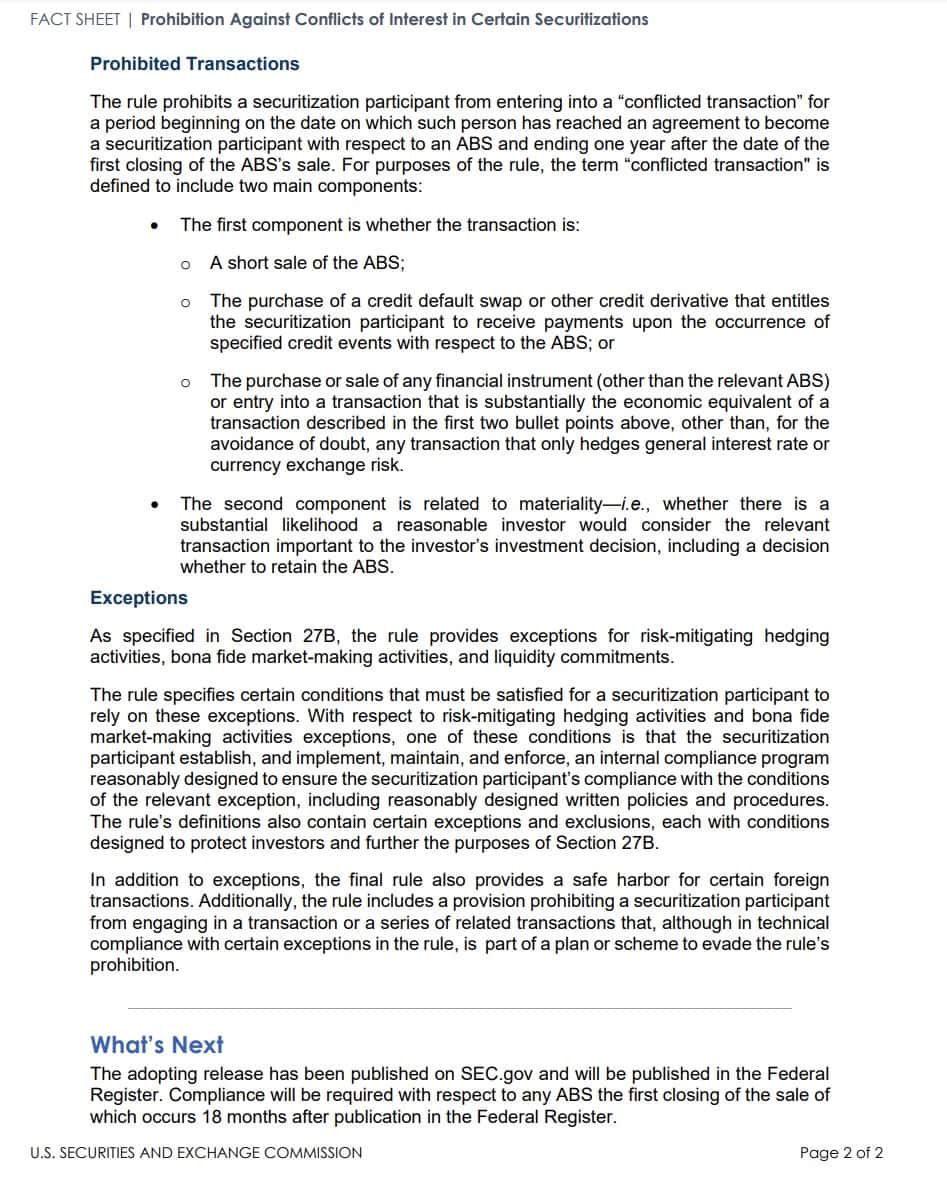

- Prohibits, for a specified period, a securitization participant from engaging in any transaction that would result in a material conflict of interest between the securitization participant and an investor in the relevant ABS.

- A securitization participant may not, for a period beginning on the date on which such person has reached an agreement to become a securitization participant with respect to an ABS and ending on the date that is one year after the date of the first closing of the sale of such ABS, directly or indirectly engage in any transaction that would involve or result in a material conflict of interest between the securitization participant and an investor in such ABS.

Under the final rule, such transactions are “conflicted transactions” and include:

- Engaging in a short sale of the relevant ABS.

- Purchasing a credit default swap or other credit derivative that entitles the securitization participant to receive payments upon the occurrence of specified credit events in respect of the ABS.

- Purchasing or selling any financial instrument (other than the relevant ABS) or entering into a transaction that is substantially the economic equivalent of the aforementioned transactions, other than, for the avoidance of doubt, any transaction that only hedges general interest rate or currency exchange risk.

- Transactions unrelated to the idiosyncratic credit performance of the ABS, such as reinsurance agreements, hedging of general market risk (such as interest rate and foreign exchange risks), or routine securitization activities (such as the provision of warehouse financing or the transfer of assets into a securitization vehicle) are not “conflicted transactions” as defined by the rule, and thus are not subject to the prohibition.

Defines the persons that are subject to the rule:

- A securitization participant includes any underwriter, placement agent, initial purchaser, or sponsor of an ABS and also includes any affiliate or subsidiary that acts in coordination with an underwriter, placement agent, initial purchaser, or sponsor or that has access to, or receives information about, the relevant ABS or the asset pool underlying or referenced by the relevant ABS prior to the first closing of the sale of the relevant ABS.

- The final rule includes functional definitions for the terms “underwriter,” “placement agent,” “initial purchaser,” and “sponsor,” which are based on the person’s activities in connection with a securitization.

The definition of “sponsor” in the final rule excludes:

- a person that acts solely pursuant to such person’s contractual rights as a holder of a long position in the ABS.

- Any person that performs only administrative, legal, due diligence, custodial, or ministerial acts related to the structure, design, assembly, or ongoing administration of an ABS or the composition of the underlying pool of assets.

- The United States or an agency of the United States with respect to any ABS that is fully insured or fully guaranteed as to the timely payment of principal and interest by the United States.

Defines asset-backed securities that are subject to the prohibition:

- Under the final rule, an “asset-backed security” subject to the prohibition is defined, to include asset-backed securities and also includes synthetic ABS and hybrid cash and synthetic ABS.

Provides exceptions to the prohibition for risk-mitigating hedging activities, liquidity commitments, and bona fide market-making activities:

- These exceptions permit certain market activities, subject to satisfaction of the specified conditions, that would otherwise be prohibited by the rule.

Addresses evasion of the exceptions:

- If a securitization participant engages in a transaction or series of related transactions that, although in technical compliance with the exception for risk-mitigating hedging activities, liquidity commitments, or bona fide market-making activities, is part of a plan or scheme to evade the prohibition in Rule 192(a)(1), that transaction or series of related transactions will be deemed to violate the prohibition.

Provides a safe harbor for certain foreign transactions:

- The prohibition will not apply to an asset-backed security if it is not issued by a U.S. person and the offer and sale of the asset-backed security is in compliance.

Fact Sheet:

What the SEC folks are saying:

TLDRS:

- SEC Rule to Prohibit Conflicts of Interest in Certain Securitizations effective February 5, 2024.

- This rule aims to prevent material conflicts of interest in the sale of asset-backed securities (ABS).

- It prohibits securitization participants from engaging in transactions that could result in a material conflict of interest with ABS investors for a specified period.

- The rule defines a "conflicted transaction" as one that involves a short sale of the ABS, the purchase of a credit derivative linked to the ABS, or a transaction economically equivalent to these, excluding those that only hedge general interest rate or currency risks.

- The transaction also must be considered materially important by a reasonable investor.

- The rule allows exceptions for risk-mitigating hedging activities, liquidity commitments, and bona fide market-making activities, subject to certain conditions.

- Under the compliance date adopted, any securitization participant must comply with the prohibition and the requirements of the exceptions to the final rule, as applicable, with respect to any ABS the first closing of the sale of which occurs Monday, June 9, 2025.

- This delayed compliance date is designed to provide affected securitization participants that intend to utilize the risk-mitigating hedging activities exception and the bona fide market-making activities exception with adequate time to develop the internal compliance programs that are required to satisfy the conditions of such exceptions as well as adequate time to develop any internal compliance mechanisms that the securitization participant decides to implement in order to address the scope of its affiliates and subsidiaries that are subject to the final rule.