Gary Gensler : "I am pleased to support this rule as it fulfills Congress’s mandate to address conflicts of interests in the securitization market, a market which was at the center of the 2008 financial crisis."

Source: https://www.sec.gov/news/statement/gensler-statement-securitizations-112723

Today, the Commission adopted a rule to prohibit certain market participants in the asset-backed securities (ABS) market from taking positions against the products they help bring to market. I am pleased to support this rule as it fulfills Congress’s mandate to address conflicts of interests in the securitization market, a market which was at the center of the 2008 financial crisis.

In the aftermath of the financial crisis, Congress addressed conflicts in the securitizations market through Section 621 in the Dodd-Frank Act, an amendment proposed by Senators Carl Levin and Jeff Merkley. An investigation led by Senator Levin found that conflict of interests arose when investment banks and other market participants sold securitized assets to investors while simultaneously taking large positions against those assets.[1]

In essence, Congress wanted to make sure that so-called securitization participants cannot bet against the ABS that they underwrite, place, or sponsor.[2]

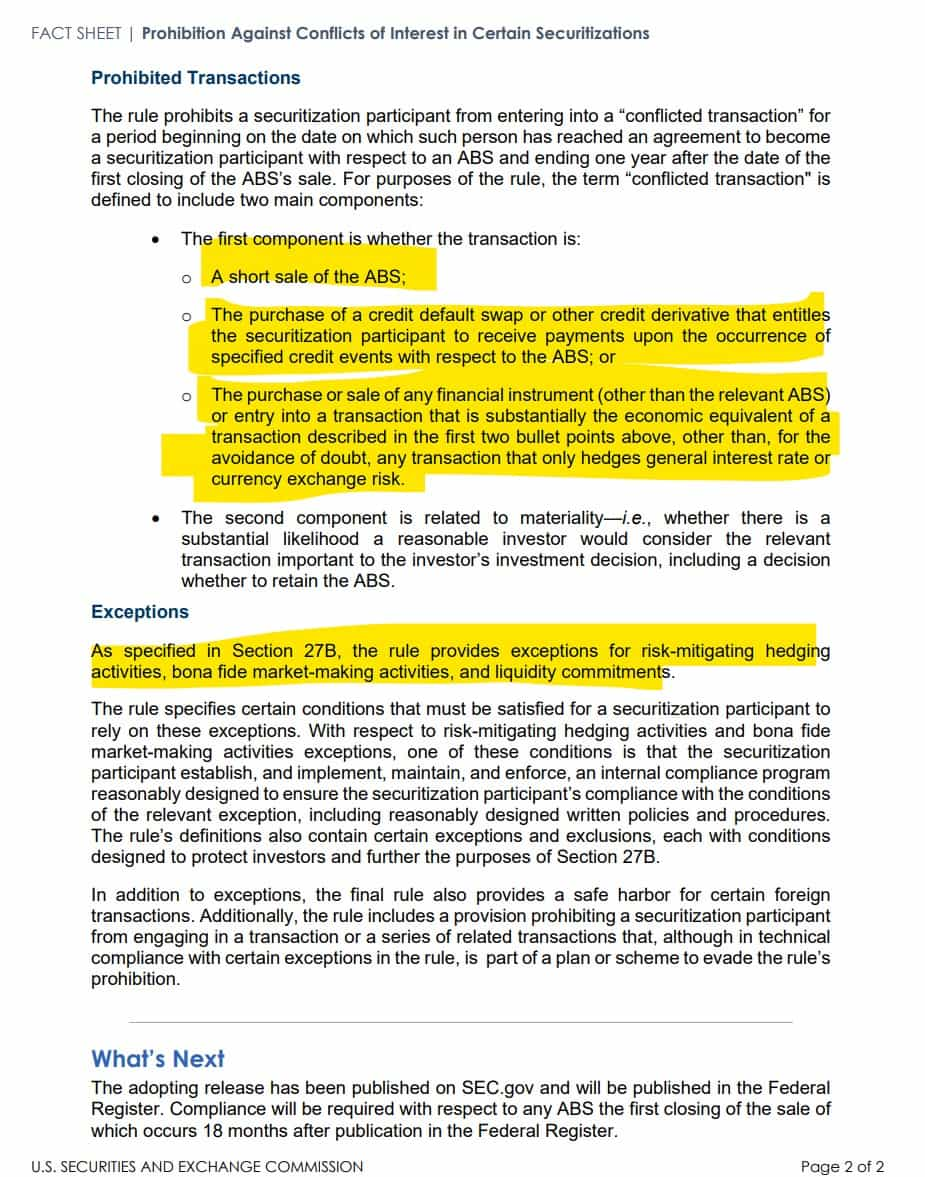

As directed by Congress, today’s rule prohibits securitization participants—including those who sell or facilitate the sale of an asset-backed security—from engaging in transactions that involve or result in any material conflict of interest with investors in that ABS.[3] The prohibition will remain in place for one year after the ABS’s first sale.

Further, as required by Section 621, the final rule provides exceptions for risk-mitigating hedging activities, bona fide market making, and certain liquidity commitments. Through these congressionally mandated exceptions, the rule allows these market activities while targeting the conflicts that Congress identified.

We benefitted from public input on these matters, and today’s adoption includes a number of modifications from the proposing release. I will mention three examples.

First, the final rule includes a more specific definition of a conflicted transaction than that which was proposed. Under the final rule, a conflicted transaction entails directly shorting the ABS, entering into a credit default swap that references the underlying assets, or something economically equivalent to either of those activities. These conflicted transactions represent ways of taking a position against the ABS that a securitization participant helps bring to market.

Second, the final rule makes clear that generalized hedging, such as an interest rate or currency hedge, is not a conflicted transaction.

Third, the final rule revises the proposed exception for risk-mitigating hedging to permit, subject to certain conditions, the use of risk management tools.

In addition, in response to comments from private mortgage insurers regarding whether the final rule would apply to their issuance of mortgage insurance linked notes (MILNs), the adopting release makes clear that MILNs do not meet the definition of an ABS or synthetic ABS for the purposes of the final rule.

Taken together, the final rule will help address conflicts of interest arising when securitization participants take positions against ABS investors’ interests. Such a rule benefits investors and issuers alike.

I’d like to thank the members of the SEC staff who worked on this final rule, including:

Erik Gerding, Mellissa Duru, Ted Yu, Rolaine Bancroft, Brandon Figg, Kayla Roberts, Ben Meeks, Komul Chaudhry, Deanna Virginio, Luna Bloom, Steve Hearne, Betsy Murphy, and Michael Coco in the Division of Corporation Finance;

Jessica Wachter, Lucretia Zinnen, Juan Echeverri, Missaka Warusawitharana, Aysa Dordzhieva, Igor Kozhanov, Joe Otchin, Oliver Richard, and Charles Woodworth in the Division of Economic and Risk Analysis;

Meredith Mitchell, Bryant Morris, Robert Teply, Dorothy McCuaig, Janice Mitnick, Joe Valerio, and Johanna Losert in the Office of the General Counsel;

Sarah ten Siethoff, Melissa Harke, and Adele Kittredge Murray in the Division of Investment Management;

Carol McGee, Josephine Tao, Mick (Tim) Riley, Patrice Pitts, James Curley, and Jesse Kloss in the Division of Trading and Markets;

Jason Casey in the Division of Enforcement;

Liz Pflaum, Ryne Duffy, and John Brodersen in the Division of Examinations; and

Dave Sanchez, Adam Wendell, Victoria Nilsson, and Mary Simpkins in the Office of Municipal Securities.

What Gary is happy about:

Fact Sheet:

Press Release:

The Securities and Exchange Commission today adopted Securities Act Rule 192 to implement Section 27B of the Securities Act of 1933, a provision added by Section 621 of the Dodd-Frank Act. The rule is intended to prevent the sale of asset-backed securities (ABS) that are tainted by material conflicts of interest. It prohibits a securitization participant, for a specified period of time, from engaging, directly or indirectly, in any transaction that would involve or result in any material conflict of interest between the securitization participant and an investor in the relevant ABS. Under new Rule 192, such transactions would be “conflicted transactions.”

Consistent with the statute, Rule 192 provides exceptions for risk-mitigating hedging activities, liquidity commitments, and bona fide market-making activities of a securitization participant. These exceptions permit certain market activities, subject to satisfaction of the specified conditions, which will allow securitization participants to continue important risk management, liquidity commitment, and market-making activities.

“I am pleased to support this rule as it fulfills Congress’s mandate to address conflicts of interests in the securitization market, a market which was at the center of the 2008 financial crisis,” said SEC Chair Gary Gensler. “As directed by Congress, today’s rule prohibits securitization participants — including those who sell or facilitate the sale of an asset-backed security — from engaging in transactions that involve or result in any material conflict of interest with investors in that ABS. Further, as required by Section 621 of the Dodd-Frank Act, the final rule provides exceptions for risk-mitigating hedging activities, bona fide market making, and certain liquidity commitments. Such a rule benefits investors and issuers alike."

Under new Rule 192, conflicted transactions include a short sale of the relevant ABS, the purchase of a credit default swap or other credit derivative that entitles the securitization participant to receive payments upon the occurrence of specified credit events in respect of the ABS, or a transaction that is substantially the economic equivalent of the aforementioned transactions, other than any transaction that only hedges general interest rate or currency exchange risk.

The adopting release is published on SEC.gov and will be published in the Federal Register. Rule 192 will become effective 60 days after publication in the Federal Register. Compliance with Rule 192 will be required with respect to any ABS the first closing of the sale of which occurs 18 months after the date of publication in the Federal Register.

TLDRS:

- SEC Adopts Rule to Prohibit Conflicts of Interest in Certain Securitizations.

- Gary Gensler : "I am pleased to support this rule as it fulfills Congress’s mandate to address conflicts of interests in the securitization market, a market which was at the center of the 2008 financial crisis."

What Gary is happy about:

- This rule aims to prevent material conflicts of interest in the sale of asset-backed securities (ABS).

- It prohibits securitization participants from engaging in transactions that could result in a material conflict of interest with ABS investors for a specified period.

- The rule defines a "conflicted transaction" as one that involves a short sale of the ABS, the purchase of a credit derivative linked to the ABS, or a transaction economically equivalent to these, excluding those that only hedge general interest rate or currency risks.

- The transaction also must be considered materially important by a reasonable investor.

- The rule allows exceptions for risk-mitigating hedging activities, liquidity commitments, and bona fide market-making activities, subject to certain conditions.

- The rule will be effective 60 days after publication in the Federal Register, with compliance required for any ABS whose first sale closing occurs 18 months after this publication.