FICC Alert! SR-FICC-2023-010: FICC & CME amend Cross-Margining Agreement. The current agreement lacks a clear requirement for joint liquidation at each Clearing Organization. The amendment identifies joint liquidation as the preferred method for default.

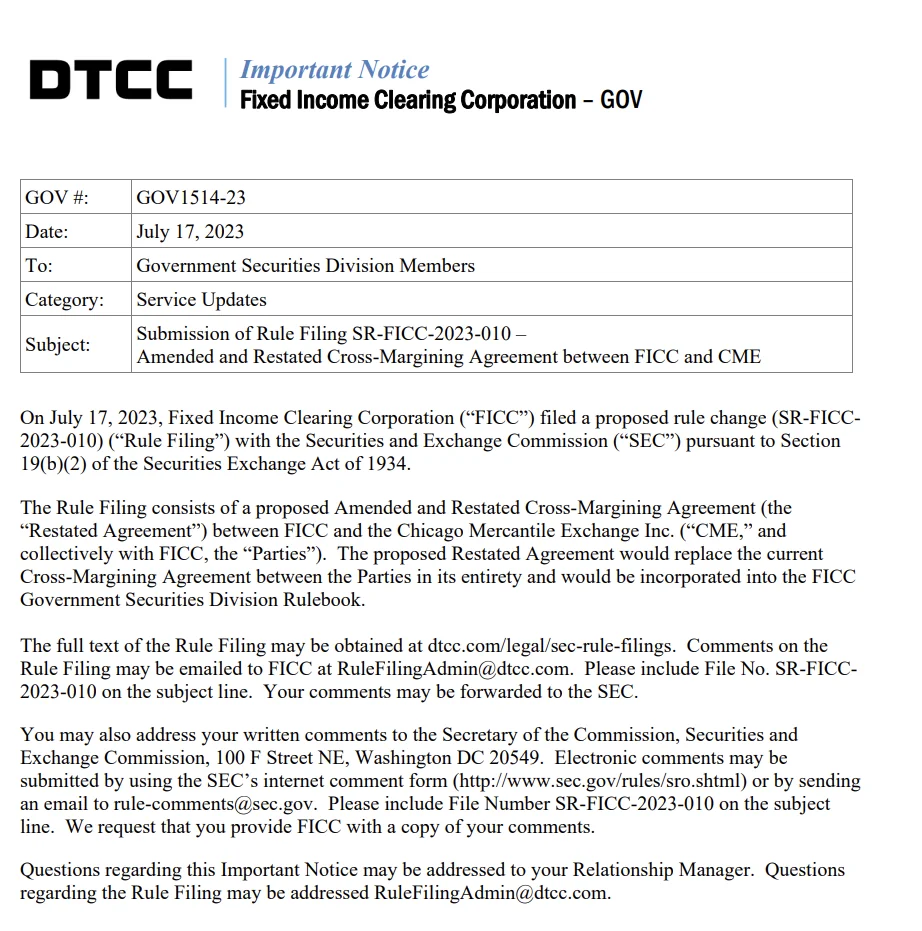

- On July 17, 2023, the Fixed Income Clearing Corporation (FICC) proposed a rule change (SR-FICC2023-010) to the Securities and Exchange Commission (SEC).

- This proposal involves an Amended and Restated Cross-Margining Agreement between FICC and the Chicago Mercantile Exchange Inc. (CME).

- If approved, this Restated Agreement would replace the current Cross-Margining Agreement entirely and be incorporated into the FICC Government Securities Division Rulebook.

SR-FICC-2023-010

Purpose:

Wut mean?

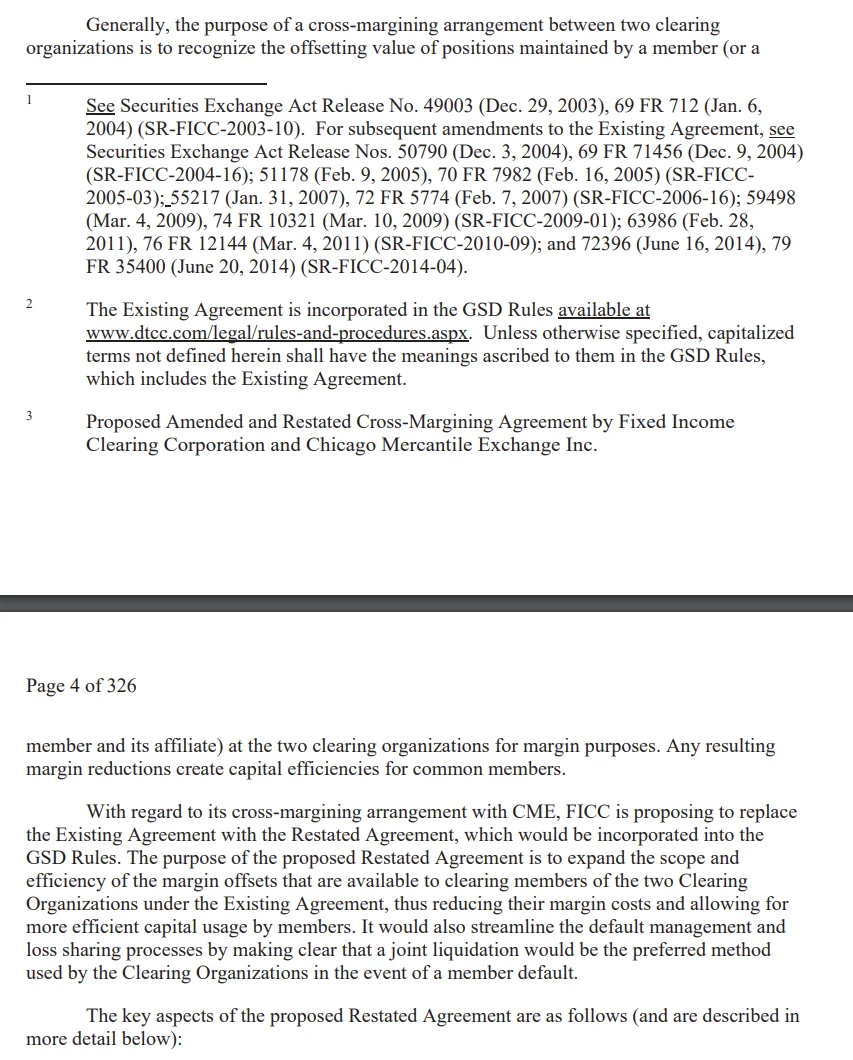

Cross-margining arrangements between two clearing organizations, such as the FICC and the CME, are designed to recognize the offsetting value of positions maintained by a member for margin purposes.

- This can lead to margin reductions and capital efficiencies for common members.

FICC has proposed to replace the existing cross-margining agreement with a Restated Agreement, which aims to expand the scope and efficiency of the margin offsets available to clearing members, thus reducing their margin costs and allowing for more efficient capital usage.

- The agreement also aims to streamline the default management and loss sharing processes, making it clear that a joint liquidation would be the preferred method used by the Clearing Organizations in the event of a member default.

Key aspects of the proposed Restated Agreement include:

- Member Participation: Participation would continue to be voluntary, and the criteria for participation would remain the same as under the current agreement.

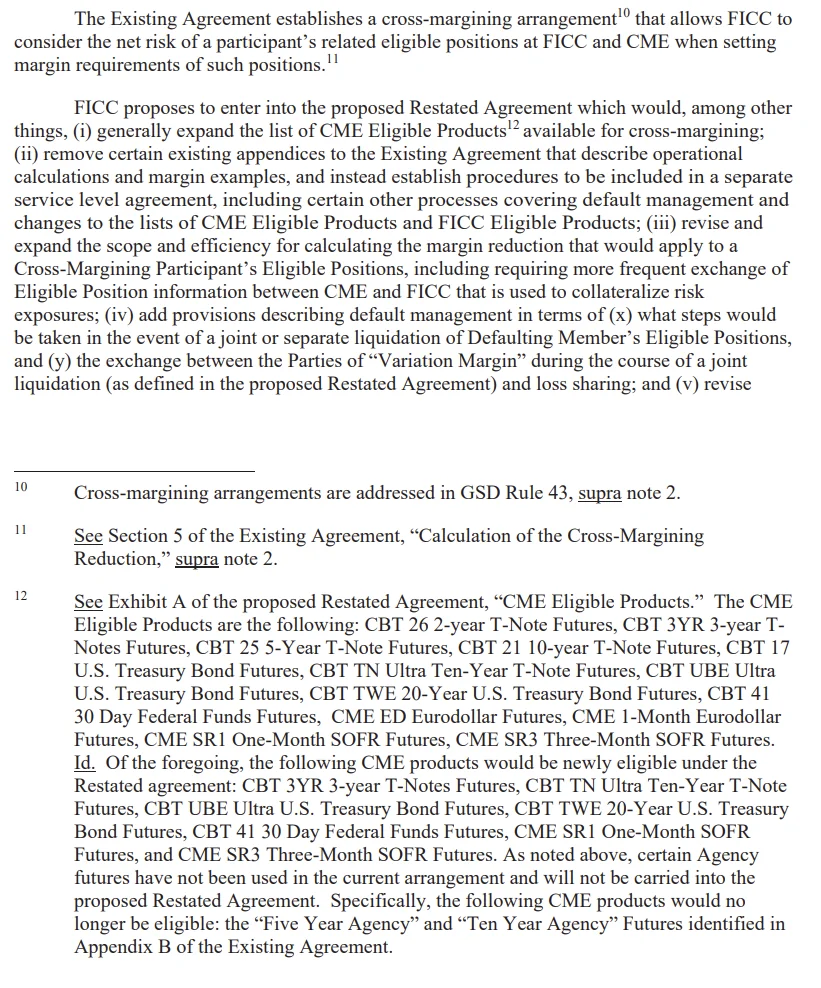

- Eligible Products: Additional CME products would become eligible under the proposed Restated Agreement, allowing for greater potential margin offsets.

- Calculation of Margin and Margin Reductions: The proposed Restated Agreement would simplify the overall margin calculation process by eliminating the need for application of offset classes of securities and conversion of CME Eligible Products into equivalent GSD Treasury security products. This should generate margin savings in excess of those under the existing agreement.

- Default Management: The proposed Restated Agreement would make clear that a joint liquidation is the preferred means of liquidation of cross-margining positions in the event of a member default. It would also provide for the possible exchange of variation margin during the course of a joint liquidation.

- FICC believes that the proposed expansion of the scope of CME Eligible Products available for cross-margining, the expansion of the scope and efficiency of the margin offsets that would be available to Cross-Margining Participants, and the improvement in the efficiency and effectiveness of the default management process would enhance the cross-margining arrangement between FICC and CME.

- "FICC believes that these enhancements would encourage greater utilization of centralized clearing, thereby facilitating systemic risk reduction."

Background:

Wut mean?

- FICC has proposed to replace the existing cross-margining agreement with a Restated Agreement, which aims to expand the scope and efficiency of the margin offsets available to clearing members, thus reducing their margin costs and allowing for more efficient capital usage.

- The Restated Agreement also aims to streamline the default management and loss sharing processes, making it clear that a joint liquidation would be the preferred method used by the Clearing Organizations in the event of a member default.

Key aspects include:

- Member Participation: Participation would continue to be voluntary, and the criteria for participation would remain the same as under the existing agreement.

- Eligible Products: Additional CME products would become eligible under the proposed Restated Agreement, allowing for greater potential margin offsets.

- Calculation of Margin and Margin Reductions: The proposed Restated Agreement would simplify the overall margin calculation process by eliminating the need for application of offset classes of securities and conversion of CME Eligible Products into equivalent GSD Treasury security products.

- Default Management: The proposed Restated Agreement would make clear that a joint liquidation is the preferred means of liquidation of cross-margining positions in the event of a member default. It would also provide for the possible exchange of variation margin during the course of a joint liquidation.

Key Terms of the Existing Agreement:

Wut mean?

The Existing Agreement between FICC and CME involves a daily margin calculation process for cross-margining. This process is not based on FICC's VaR model.

- Instead, both FICC and CME independently manage their own positions and collateral, and determine the margin available for cross-margining.

Every business day, they exchange files regarding their members' positions eligible for cross-margining.

- FICC then calculates how much a member's margin requirement can be reduced by comparing the member's eligible positions and related margin requirements at GSD against those at CME.

- Both FICC and CME can then reduce the amount of collateral they collect to reflect the offsets between the participant's positions at FICC and at CME.

- The calculation of these offsets relies on a methodology that converts CME Eligible Products into equivalent GSD Treasury security products and uses minimum margin factors to measure interest rate exposure.

To limit potential margin reductions from cross-margining, the Clearing Organizations apply a Disallowance Factor to each Offset Class (a group of securities by maturity).

- Based on these Disallowance Factors, margin offsets are determined for each Offset Class.

- The sum of these margin offsets provides the member's Cross-Margining Reduction at CME and at GSD.

The Clearing Organizations have the right to not reduce a participant's margin requirement by the Cross-Margining Reduction or to reduce it by less than the Cross-Margining Reduction.

- However, they cannot reduce a participant's margin requirement by more than the Cross-Margining Reduction.

Wut mean?

CME and FICC mutually guarantee certain performance obligations of a Cross-Margining Participant.

- These guarantees are necessary to facilitate the Cross-Margining Arrangement and represent contractual commitments between the two Clearing Organizations.

Specifically, CME and FICC guarantee the Cross-Margining Participant’s performance of its obligations to the other Clearing Corporation up to the amount of the member’s Cross-Margining Reduction.

- This is the maximum amount by which a Cross-Margining Participant’s margin requirement at one Clearing Organization may be reduced.

In addition, the Cross-Margining Participant has an obligation to reimburse a Clearing Organization for any amounts paid under these guarantees.

- This obligation is collateralized by the positions and margin of the Cross-Margining Participant held by the guarantor (either CME or FICC).

- The provisions covering the cross-margining guarantees and the Cross-Margining Participant’s Reimbursement Obligation will remain the same under the proposed Restated Agreement.

Member Default Event:

Wut mean?

Under the Existing Agreement, there is no explicit requirement for CME and FICC to conduct a joint liquidation at each Clearing Organization.

- However, they are required to coordinate the liquidation of positions covered by the Cross-Margining Arrangement to close out offsetting or hedged positions simultaneously, unless one party has elected not to liquidate.

The agreement also includes provisions for sharing losses between CME and FICC according to the terms of the cross-margining Guaranties.

- The allocation of losses depends on whether each party's liquidation results in a Cross Margin Gain or Cross Margin Loss.

If after payments are made according to the Guaranties and loss sharing arrangement, one of the Clearing Organizations computes an Aggregate Net Surplus, and the other an Aggregate Net Loss, the agreement includes an obligation for the Clearing Organization with the surplus to make a "Maximization Payment" to the other Clearing Organization.

- There is also a "Maximization Reimbursement Obligation" of the Defaulting Member to the Clearing Organization that is obligated to make a Maximization Payment.

- This provision allows excess collateral of a Defaulting Member to initially remain with the Clearing Organizations, if needed, to cover losses.

The Proposed Restated Agreement - Key Elements of the Proposed Restated Agreement:

Wut mean?

Would expand the list of CME products eligible for cross-margining to include a broader range of interest rate futures cleared by CME. This change is intended to provide Cross-Margining Participants with benefits that better align with the current structure of CME's Interest Rates futures market. The expanded list would include additional U.S. Treasury futures and SOFR futures. The list of FICC Eligible Products would consist of U.S. Treasury securities, specifically Treasury notes and bonds. Both FICC and CME would establish a "Cross-Margining Account" for each participating member, which would identify the transactions, positions, and margin subject to the proposed Restated Agreement.

Wut mean?

Includes provisions to improve default management procedures, information sharing, and documentation between FICC and CME. A separate service level agreement (SLA) would be established, outlining specific timeframes for the daily exchange of information needed to value positions in the Cross-Margining Accounts and calculate the Cross-Margin Requirement for each participant. The SLA would also detail operational processes for default management and criteria for modifying the list of eligible products for cross-margining. Changes to eligible products that require a change to FICC's or CME's margin model would need regulatory review and approval. The SLA would replace certain appendices in the Existing Agreement, incorporating operational processes and information related to the proposed changes to cross-margin requirements and loss sharing arrangements.

Adopts a new methodology for the daily calculation of a Cross-Margining Participant’s Cross-Margin Requirements. The aim is to expand the scope and efficiency of margin offsets, thus reducing margin costs and allowing for more efficient capital usage. The new methodology would treat a participant’s relevant products as a single portfolio, eliminating the need for separate margin calculations and conversions of Eligible Products. Each Clearing Organization would independently determine the percentage of margin savings derived from treating the portfolio as a single entity. If the lesser of these percentages exceeds the minimum margin offset threshold agreed by the Clearing Organizations, the amount of margin required to be deposited by a Cross-Margining Participant would be reduced by the lower of these percentages. If both percentages are less than the agreed threshold, no Margin Reduction would be applied. The Cross-Margin Requirement for a participant cannot be changed without the consent of both Clearing Organizations.

Allows either FICC or CME to terminate, suspend, or limit the activities of a Cross-Margining Participant (a "Defaulting Member") at any time. Upon such an event, the Clearing Organization that has taken these actions (the "Liquidating CO") must immediately notify the other Clearing Organization. Unlike the existing agreement, the proposed agreement provides a different approach to the liquidation process by outlining a sequence of coordinated steps the Clearing Organizations must take depending on whether or not the other Clearing Organization elects to treat the Cross-Margining Participant as a Defaulting Member under its rules. The aim of this new approach is to improve the efficiency and effectiveness of the default management process and enhance coordination between the Clearing Organizations.

Wut mean?

Includes provisions for a scenario where one Clearing Organization (the "Liquidating CO") treats the Cross-Margining Participant as a Defaulting Member, and the other Clearing Organization (the "Non-Liquidating CO") does not.

- In this case, the Non-Liquidating CO would provide the Liquidating CO with cash to cover the margin reduction under the proposed Restated Agreement, aligning the Defaulting Member’s margin resources with its exposures at the Liquidating CO.

Specifically, the Non-Liquidating CO would require the Defaulting Member to pay the sum of its Margin Reduction at both the Liquidating CO and the Non-Liquidating CO within one hour of demand.

- If the Non-Liquidating CO receives this payment in full within the timeframe, it would then pay the Liquidating CO the Defaulting Member’s Margin Reduction at the Liquidating CO within one hour of receipt.

- After making this payment, the Non-Liquidating CO would have no further obligations to the Liquidating CO regarding the Default Event.

However, if the Non-Liquidating CO does not receive this payment in full within one hour or another agreed upon timeframe, it would cease to act for the Defaulting Member.

- The provisions of the proposed Restated Agreement pertaining to the scenario where both Clearing Organizations treat the Member as a Defaulting Member would then apply.

Outlines three potential liquidation routes if both Clearing Organizations decide to treat the Cross-Margining Participant as a Defaulting Member. The choice of liquidation alternative depends on portfolio exposure, resources, hedging cost, and approval through DTCC’s default management governance process.

- Joint Liquidation: The Clearing Organizations would attempt to conduct a joint liquidation, where they jointly transfer, liquidate, or close out the Eligible Positions in the Cross-Margining Accounts carried for the Defaulting Member.

- Buy-Out: If a joint liquidation is deemed not feasible or advisable, either Clearing Organization may offer to buy-out the Relevant Positions and any remaining collateral relating to them at the last settlement price for such positions immediately prior to the time the offer is made.

- Individual Liquidation: If neither joint liquidation nor buy-out is feasible or advisable, each Clearing Organization would independently transfer, liquidate, or close out the Eligible Positions in the Cross-Margining Account carried for the Defaulting Member at that Clearing Organization.

VM Margin:

- One Clearing Organization has a Gain, the other has a Loss: If a Clearing Organization has both a Cross-Margin VM Gain and an Other VM Gain (Payor), and the other Clearing Organization has a Cross-Margin VM Loss (Receiver), the Payor would pay the Receiver an amount equal to the VM Receiver’s Cross-Margin VM Loss, but not exceeding the VM Payor’s Cross-Margin VM Gain. However, the VM Payor is not required to make such payment if it determines that the liquidation will result in a loss to it or if the VM Receiver is legally restricted from making the payment.

- One Clearing Organization has a Gain and a Loss, the other has a Loss: If a Clearing Organization has a Cross-Margin VM Gain and an Other VM Loss (the Payor) and the sum of these amounts is positive (Aggregate Gain), and the other Clearing Organization has a Cross-Margin VM Loss (the Receiver), the VM Payor will pay the VM Receiver an amount equal to the VM Receiver’s Cross-Margin VM Loss, but not exceeding the VM Payor’s Aggregate VM Gain, unless otherwise agreed. Again, the VM Payor is not required to make such payment if it determines that the liquidation will result in a loss to it or if the VM Receiver is legally restricted from making the payment.

- One Clearing Organization has a Gain and a Loss, the other has a Loss, and the sum is negative: If a Clearing Organization has a Cross-Margin VM Gain and an Other VM Loss and the sum of these two amounts is negative, and the other Clearing Organization has a Cross-Margin VM Loss, neither Clearing Organization is required to make a payment unless otherwise agreed.

After the liquidation of a Defaulting Member, the VM Receiver must repay any variation margin payments it received from the VM Payor. This repayment obligation is netted and offset against the VM Payor’s payment obligation under the loss sharing provisions in the Agreement.

Loss Sharing:

The process for calculating and allocating gains or losses after the liquidation of a Defaulting Member:

Net Gain or Net Loss Calculation: Each Clearing Organization calculates its individual "Net Gain" or "Net Loss" based on its "Collateral on Hand" and its "Liquidation Cost".

- "Net Gain" or "Net Loss" is the sum of the Collateral on Hand and the Liquidation Cost.

- If this sum is positive, it's a "Net Gain"; if negative, it's a "Net Loss".

- "Collateral on Hand" refers to the margin held with respect to the Cross-Margining Account of a Defaulting Member immediately prior to the Default Event.

- "Liquidation Cost" is the aggregate gain or loss realized in the liquidation, transfer, or management of Eligible Positions held by the Clearing Organization in the Cross-Margining Account of the Defaulting Member, including any unpaid Variation Margin and any reasonable costs, fees, and expenses incurred.

- The Clearing Organizations determine whether the sum of the individual Net Gains and Net Losses results in a combined Net Gain or Net Loss.

- The Clearing Organizations then allocate any combined Net Gain or Net Loss pro rata based on each Clearing Organization’s "Share of the Cross-Margining Requirement" (its "Allocated Net Gain" or "Allocated Net Loss," as applicable).

- If a Clearing Organization has an individual Net Gain that is less than its Allocated Net Gain, an individual Net Loss that is greater than its Allocated Net Loss, or an individual Net Loss when the joint liquidation resulted in a combined Net Gain (the "worse-off party"), then the other Clearing Organization shall be required to pay to the worse-off party an amount equal to the difference between the worse-off party’s individual Net Gain or Net Loss and its Allocated Net Gain and Allocated Net Loss.

The "Share of the Cross-Margining Requirement" for a Clearing Organization is the ratio of the margin required for the Cross-Margining Account at the Clearing Organization after taking into account the Margin Reduction to the total Cross-Margining Requirement across both Clearing Organizations.

Separate Liquidations:

The loss sharing provisions under this separate liquidation scenario are:

- If both Clearing Organizations have a Net Gain or a Net Loss with respect to the Cross-Margining Account of the Defaulting Member, no payment will be due to either Clearing Organization in respect of the Guaranties between FICC and CME.

- If one Clearing Organization has a Net Loss (the “worse-off party”) and the other has a Net Gain (the “better-off party”), then the better-off party will pay the worse-off party the lesser of the Net Gain or the absolute value of the Net Loss.

The proposed Restated Agreement will not retain language from the Existing Agreement that each Clearing Organization’s calculation of Available Margin for loss sharing purposes is subject to such Clearing Organization’s prior satisfaction of its obligations under other cross-margining agreements and loss sharing arrangements. This means all margin amounts calculated under the proposed Restated Agreement would be available to cover a Clearing Organization’s losses.

How to comment:

- All prospective commenters should follow the Commission’s instructions on how to submit comments, available at https://www.sec.gov/regulatory-actions/how-to-submitcomments.

TLDRS:

- On July 17, 2023, the Fixed Income Clearing Corporation (FICC) proposed a rule change to the Securities and Exchange Commission (SEC). This involves a new Cross-Margining Agreement between FICC and the Chicago Mercantile Exchange Inc. (CME), which would replace the current agreement and be incorporated into the FICC Government Securities Division Rulebook.

- Cross-margining arrangements allow for margin reductions and capital efficiencies for common members.

- The new agreement aims to expand the scope and efficiency of these margin offsets, reduce margin costs, and streamline default management and loss sharing processes.

Key points of the proposed agreement:

- Voluntary member participation with the same criteria as the existing agreement.

- Additional CME products would become eligible, allowing for potential margin offsets.

- Simplified margin calculation process, generating margin savings in excess of those under the existing agreement.

- Clear preference for joint liquidation in the event of a member default, with possible exchange of variation margin during the liquidation.

The proposal also expands the list of CME products eligible for cross-margining and adopts a new methodology for daily calculation of a Cross-Margining Participant’s Cross-Margin Requirements.

- This aims to expand the scope and efficiency of margin offsets, thus reducing margin costs and allowing for more efficient capital usage.

- In the event of a member default, the proposal outlines potential liquidation routes.

- The choice depends on portfolio exposure, resources, hedging cost, and approval through DTCC’s default management governance process.

Under the Existing Agreement, there is no express language requiring the Parties to attempt to conduct a joint liquidation.

- The proposed Agreement would make clear that a joint liquidation is the preferred means of liquidation of cross-margining positions in the event of a member default.

- All prospective commenters should follow the Commission’s instructions on how to submit comments, available at https://www.sec.gov/regulatory-actions/how-to-submitcomments.