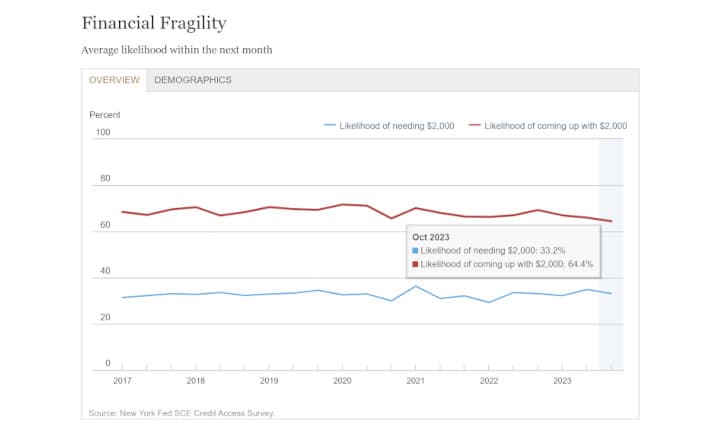

Survey of Consumer Expectations: U.S. households probability of being able to come up with $2,000 if an unexpected need arose within the next month falling to its lowest level since 2013.

Source: https://www.newyorkfed.org/microeconomics/sce/credit-access#/financial-fragility1

Wut Mean?:

Overall Decline in Consumer Credit Demand (2023):

- General weakening in most credit application rates.

- Credit card limit increase applications rose.

Rejection Rates Trends:

- Overall rise in rejection rates for credit applications.

- Decline in rejection rates for credit card limit extensions and new mortgage applications.

- Higher creditworthiness among those applying for new mortgages in 2023.

Future Credit Application Expectations:

- Anticipated decrease in likelihood of applying for new credit cards, auto loans, mortgages, or mortgage refinances in the next 12 months.

- Significantly higher average perceived likelihood of future credit application rejections.

Increased Financial Fragility:

- Probability of being able to raise $2,000 for unexpected needs lowest since 2013.

Specific Credit Application Trends:

- Overall credit application rate fell to 41.2% from 44.8% in 2022.

- Decreases in applications for credit cards, auto loans, mortgage loans, and mortgage refinancing.

- Increase in credit card limit increase applications.

- Mortgage loan applications at a new low of 4.3%.

Specific Rejection Rate Trends:

- Increased rejection rates for credit cards, auto loans, and mortgage refinancing.

- Decreased rejection rates for mortgage loans and credit card limit extensions.

- Auto loans rejection rate at 11.0%, the highest since 2013.

Reduced Likelihood of Future Credit Applications:

- Notable decrease to 25.1% in households planning to apply for any credit type in the next 12 months.

Key findings from the survey over the past year include:

Experiences:

- Reported application rates for any kind of credit over the past 12 months declined notably over the past year, following a smaller decline in 2022. Current rates are below pre-pandemic levels for those older than 40 but are slightly higher for those under 40. Overall, the average 2023 application rate of 41.2% was well below its 2022 level of 44.8%, and below its pre-pandemic 2019 level of 45.8%.

- Reported rejection rates among applicants increased by 2.1 percentage points to 20.1% in 2023 from 18.0% in 2022, well above its 2019 level of 17.6%.

- The average share of respondents who were too discouraged to apply for credit over the past 12 months, despite needing it, continued its gradual decline, falling to 5.2% in 2023 from 6.5% in 2022, 6.6% in 2021, and 7.0% in 2020, and falling below its 2019 level of 6.4%.

- Considering applications and rejections experienced by respondents in the 12 months preceding each survey for specific credit types (credit cards, credit card limit increases, auto loans, mortgages, and mortgage refinancing), the survey found:

- Application Rates:

- The application rate for credit cards remained robust during 2023, reaching 29.0% in October 2023, above its October 2022 level of 27.1% and its pre-pandemic reading of 27.2% in October 2019. The average application rate for credit cards for 2023 overall was 26.0%, 0.7 percentage points lower than the average rate for 2022.

- The application rate for credit card limit increases increased somewhat during 2023, at 17.8% in October 2023, compared to 11.2% in October 2022 and 12.0% in October 2019. For 2023 overall, the application rate increased to 14.4% in 2023, from 11.5% in 2022. The increase was largest for those with credit scores under 680.

- The application rate for auto loans in October 2023 was 13.5%, slightly higher than in October 2022 (12.9%), but the average application rate for the year overall declined to 12.7% in 2023 from 13.0% in 2022.

- Mortgage loan application rates declined to 4.3% in October 2023 from 6.7% in October 2022. The average rate for 2023 overall was 5.7%, 1.5 percentage points below the 2022 average, and 2.2 percentage points below the 2019 average. The October 2023 reading is a new series low.

- Application rates for mortgage refinancing declined further during 2023, falling to 3.3% in October 2023 from 8.9% in October 2022. The October 2023 level is well below the levels that prevailed before the pandemic and represents a series low.

- Rejection Rates:

- Reported average rejection rates for credit cards, auto loans, and mortgage loan refinance applications in 2023 exceeded those in 2022, while those for mortgage and credit card limit extension applications instead declined slightly.

- The average rejection rate for credit card applications during 2023 increased by 1.1 percentage points to 19.6%.

- The average rejection rate of mortgage applications decreased by 2.5 percentage points to 12.1% in 2023, remaining above the 2019 rate of 10.2%.

- The average rejection rate on auto loans increased by 5.8 percentage point to 11.0% in 2023, the highest rate since the start of our series in 2013.

- The reported rejection rate for credit card limit increases declined to 30.9% in 2023 from 35.3% in 2022.

- The average rejection rate on mortgage refinance applications increased to 15.5% in 2023 from 9.9% in 2022.

- Voluntary account closures for any type of credit increased slightly to 15.8% in 2023 from 15.4% during 2022. The proportion of respondents experiencing lender-initiated account closures for any type of credit increased to 7.2% in 2023 from 5.3% in 2022.

- Application Rates:

Expectations

- Responses regarding the ability to pay for an unexpected expense suggested a slight increase in the subjective financial fragility of U.S. households. The average probability of being able to come up with $2,000 if an unexpected need arose within the next month decreased to 65.8% in 2023 from 67.5% in 2022. The 65.8% annual reading is a new series’ low. The average probability of needing $2,000 for an unexpected expense in the next month increased to 33.4% in 2023 from an average of 32.0% in 2022.

- The proportion of respondents who reported that they are likely to apply for at least one type of credit over the next 12 months decreased notably, falling to 25.1% in October 2023 (25.9% for 2023 overall) from 28.0% in October 2022 (and 26.7% for 2022 overall) The decrease was driven mostly by those with credit scores between 680 and 760 and respondents aged 60 and older.

- The average likelihood of applying for a mortgage decreased further to 6.7%. from 7.3% in 2022. The average likelihood of applying for a mortgage refinance over the next 12 months reached a new series low of 3.5% in October 2023. For the year overall, the average likelihood of applying for a mortgage refinance dropped to 4.7% in 2023 from 6.1% in 2022.

- The average likelihood of applying for an auto loan declined marginally, to 10.2% in October 2023 (11.3% for 2023 overall) from 10.9% in October 2022 (11.4% for 2022 overall).

- The average likelihood of applying for a credit card over the next 12 months declined slightly, to 12.7% in October 2023 (12.3% for 2023) from 13.6% in October 2022 (12.6% for 2022 overall). The average likelihood of applying for a credit card limit increase over the next 12 months was mostly unchanged in 2023, relative to 2022.

- The average perceived likelihood of a future credit application being rejected, conditional on applying over the next 12 months, was higher in 2023 relative to 2022 for all loan types. The rate increased by 1.7 percentage points for credit cards, 6.4 percentage points for mortgage loans, 4.2 percentage points for auto loans, 3.3 percentage points for credit card limit increase requests, and 3.0 percentage points for mortgage refinance applications.

Folks are involuntarily losing access to credit accounts at a faster rate:

TLDRS:

Survey of Consumer Expectations:

- Credit Demand and Application Rates (2023):

- Overall decline in consumer credit demand.

- Decreased application rates for most credit types; increase for credit card limit increases.

- Notable drop in mortgage loan applications to 4.3%.

- Rejection Rates and Creditworthiness:

- Rise in rejection rates for credit cards, auto loans, and mortgage refinancing.

- Decrease in rejection rates for new mortgage applications and credit card limit extensions.

- Applicants for new mortgages in 2023 showed higher creditworthiness.

- Future Credit Application Expectations:

- Decreased likelihood of applying for new credit cards, auto loans, and mortgages in the next 12 months.

- Increased perceived likelihood of future credit application rejections for all loan types.

- Financial Fragility of U.S. Households:

- Decreased probability of raising $2,000 for unexpected needs, the lowest since 2013.

- Voluntary and Involuntary Account Closures:

- Rise in lender-initiated account closures for any type of credit in 2023.

- It's a good thing GameStop has Apes holding down the balance sheet in an economy facing headwinds!