SEC Commissioner Mark Uyeda on Proposed Rule 6b-1 (Volume-Based Exchange Transaction Pricing): "Ultimately, given the anticompetitive harms likely associated with the proposal—which will harm smaller entities and retail investors—I cannot support it."

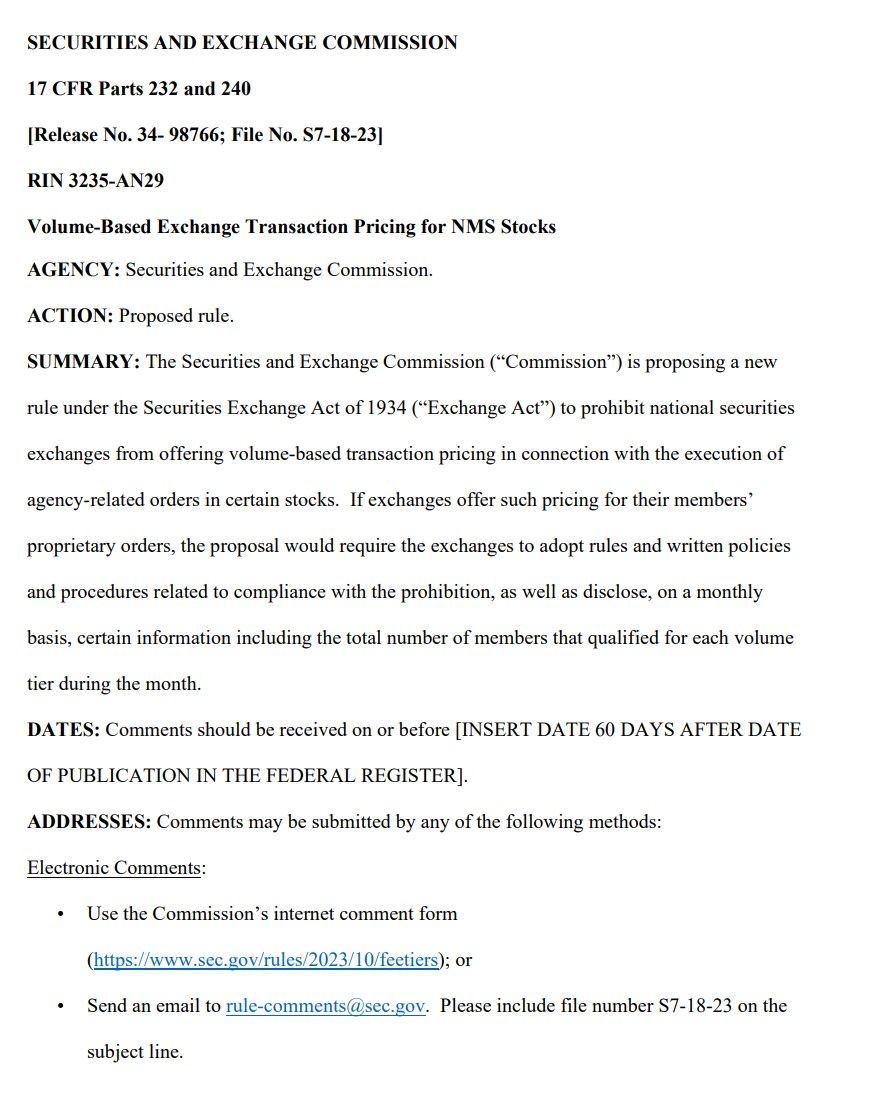

Statement on Volume-Based Exchange Transaction Pricing for NMS Stocks

Thank you, Chair Gensler. Today’s proposal would “prohibit national securities exchanges from offering volume-based transaction pricing for agency-related volume in certain stocks and … require national securities exchanges to disclose certain information if they offer volume-based transaction pricing for proprietary volume in these stocks.”[1]

Volume-based transaction pricing is alleged to harm investors by allowing intermediaries to receive insufficiently disclosed incentive payments for routing orders to exchanges. However, upon closer examination, this simplistic explanation does not paint the full picture. Rather than moving forward with this proposal, the Commission would have been better off making a serious attempt to study and identify the root causes of how pricing and trading volume on exchanges has led to current conditions.

A key component of a market-based economy is the freedom to develop pricing mechanisms. These mechanisms may range from the pricing of various bundles of goods and services to everyday volume discounts that retailers receive from wholesalers when they purchase their supplies. Prices and price mechanisms send signals that optimize the allocation of scarce resources and is a far superior alternative than central planning.

When wholesalers give volume discounts to retailers, they generally do not do this out of generosity or charity; they do it because moving items in bulk may be more efficient, and the volume discounts reflect that efficiency. In competitive markets, customers benefit from these volume discounts. Today’s rule proposal would prohibit exchanges from extending volume discounts to broker-dealers, if those broker-dealers are engaged in transactional services for their customers.

Economies of scale are inherent in our securities markets. There are fixed costs that, on a per unit basis, reward scale, such as information technology and data expenses, investments in connectivity to exchange platforms, and compliance costs. Even though one would expect some degree of market power to evolve out of such scale economies, our brokerage industry is marked by a considerable amount of competition.[2] One reason is that inputs that would otherwise constitute scale economies can be sold by large broker-dealers—through technological connectivity—to small broker-dealers, thereby sharing the benefits of the scale. This is precisely what currently happens when exchange services are offered by member broker-dealers to non-member broker-dealers. As the proposal’s economic analysis notes “[t]hrough direct market and sponsored access services, … lower-volume broker-dealers choose to route orders through high volume broker-dealers.”[3] This renders the process of sending trades to a platform less expensive than it would otherwise be for small broker-dealers. In turn, this efficient mechanism is rewarded by the exchanges through volume pricing. Like the rest of the economy, volume-discount pricing promotes efficiency and cost-reduction. Yet, today’s proposal would prohibit it.

The proposal would except proprietary traders, meaning that exchange members who are trading for their own account could continue to receive volume-discounts, while those that facilitate transactions of customers could not. Ironically, this exception highlights the competitive damage inherent in the proposal because it will disadvantage small proprietary traders. The Commission’s proposal would preclude the availability of the benefits of volume-based discounts that would have been enjoyed by small proprietary traders—as customers of broker-dealers—but leave those same benefits in place for large proprietary traders who do not require such broker-dealer intermediation. How would this action benefit competition? How would it benefit retail investors?

Given the shift in incentives entailed by prohibiting volume-based discounts, the added anticompetitive burden on small broker-dealers—who may no longer be able to purchase transactional access services from other broker-dealers at as low a cost as previously—is the same as it is for the small proprietary traders. Thus, a new broker-dealer or small proprietary trading firm will be disadvantaged. This raises questions as to whether the Commission has sufficiently considered its obligations under the Exchange Act, which “prohibits the Commission from adopting any rule that would impose a burden on competition not necessary or appropriate in furtherance of the Exchange Act.”[4]

Liquidity has a positive externality. If you want to buy or sell a security, you want a platform where there are as many other buyers and sellers as possible to obtain the best price. In securities markets, liquidity begets liquidity and, for this reason, there will be a certain degree of market concentration that prevails among exchange platforms. Unsurprisingly, exchanges compete for increased liquidity, including through their pricing models. The National Market System was implemented to promote national competition for securities transactions through required information flows and obligations. Thus far, that framework has been largely successful. The proposal’s economic analysis highlights 16 exchanges in the United States. Within that number, there are three exchange “groups” that account for the bulk of the transactions, with “the Nasdaq group … making up 30% of the market by trading volume, the Intercontinental Exchange group … making up 34% and Cboe Global Markets making up 24%.”[5] In a securities market, where liquidity begets liquidity—where size begets size—that is a competitive outcome.

Nevertheless, the Commission should continue to evaluate the state of competition within the markets and the quality of execution services. For example, one improvement might include clearer disclosure regarding volume discounts to better inform the market.

Ultimately, given the anticompetitive harms likely associated with the proposal—which will harm smaller entities and retail investors—I cannot support it. I thank the staff in the Divisions of Trading and Markets and Economic and Risk Analysis as well as the Office of General Counsel for their efforts.

[1] See Volume-Based Exchange Transaction Pricing for NMS Stocks (“Volume-Based Transaction Pricing”), Release No. 34-98766, (Oct. 18, 2023), at 1, available at https://www.sec.gov/files/rules/proposed/2023/34-98766.pdf.

[2] See https://www.finra.org/media-center/statistics, which indicates as of 2022, 3,378 securities firms regulated by FINRA, with over 150,000 branch offices.

[3] See Volume-Based Transaction Pricing at 103.

[4] Id. at 63; and see 15 U.S.C. 78w(a)(2).

[5] Id. at 71.

What Mark is Upset about:

Background:

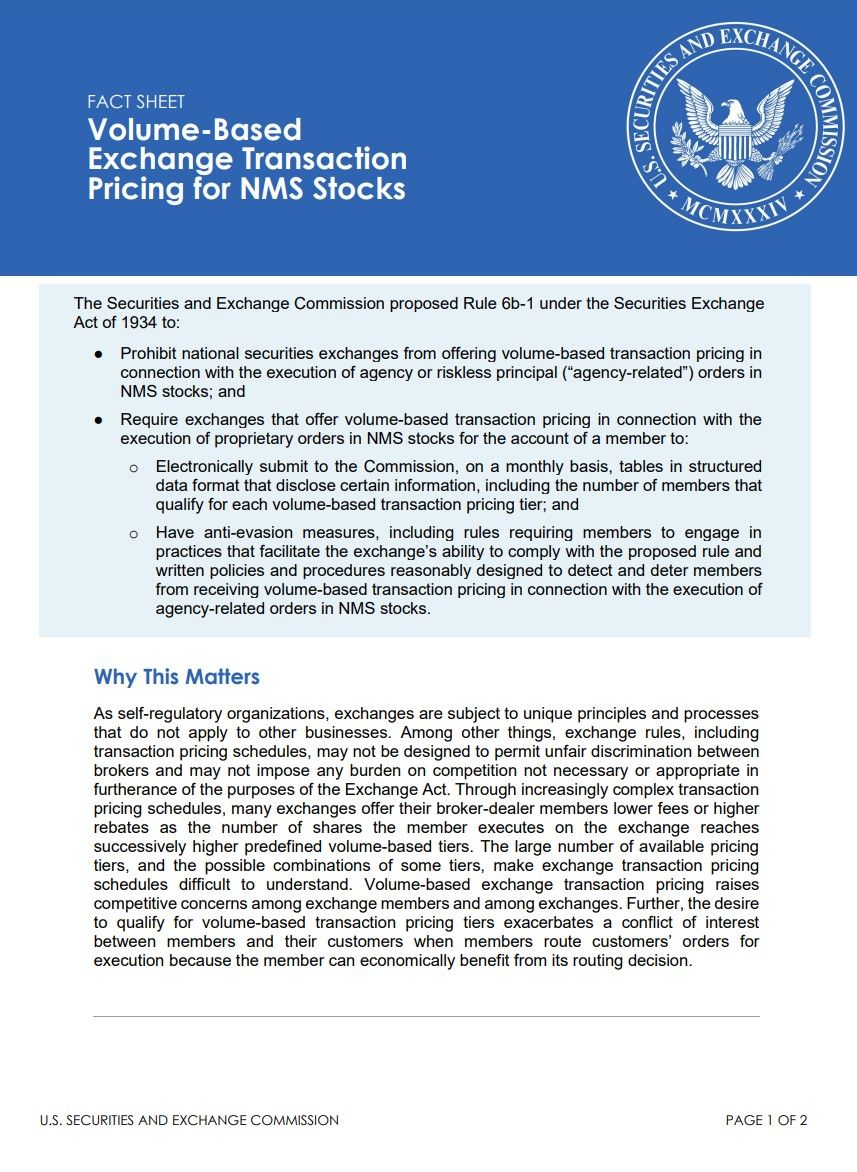

National securities exchanges (“exchanges”) that trade NMS stocks maintain pricing schedules that set forth the transaction pricing they apply to their broker-dealer members that execute orders on their trading platforms. As self-regulatory organizations under the Exchange Act, exchanges are subject to unique principles and processes that do not apply to other businesses. For example, all proposed rules of an exchange, including exchange transaction pricing proposals, must be filed with the Commission. In addition, pricing schedules must be publicly posted on the exchange’s website.

The Exchange Act further requires that exchange pricing proposals, among other things, provide for the “equitable allocation of reasonable dues, fees, and other charges among its members and issuers and other persons using its facilities” that “are not designed to permit unfair discrimination between customers, issuers, brokers, or dealers” and “do not impose any burden on competition not necessary or appropriate in furtherance of the purposes of” the Exchange Act. With respect to the requirement that the rules of an exchange not impose any burden on competition not necessary or appropriate in furtherance of the purposes of the Exchange Act, the Senate Banking, Housing and Urban Affairs Committee report that accompanied the 1975 amendments to the Exchange Act stated that “this paragraph is designed to make clear that a balance must be struck between regulatory objectives and competition, and that unless an interference with competition is justified in terms of the achievement of a statutory objective, it cannot stand.”

Section 11A of the Exchange Act directs the Commission to facilitate the establishment of a national market system in accordance with specified Congressional findings. Among the Congressional findings are assuring (i) fair competition among brokers and dealers and among exchange markets, and (ii) the practicability of brokers executing investors’ orders in the best market. Rather than setting forth minimum components of the national market system, the Exchange Act grants the Commission broad authority to oversee the implementation, operation, and regulation of the national market system consistent with Congressionally determined goals and objectives.

Fact Sheet:

Press Release:

The Securities and Exchange Commission today proposed a new rule that would prohibit national securities exchanges from offering volume-based transaction pricing in connection with the execution of agency or riskless principal (“agency-related”) orders in NMS stocks. The proposal also would require national securities exchanges to have certain anti-evasion rules and written policies and procedures and disclose certain information if they offer volume-based transaction pricing for member proprietary volume in NMS stocks.

“Currently, the playing field upon which broker-dealers compete is unlevel,” said SEC Chair Gary Gensler. “Through volume-based transaction pricing, mid-sized and smaller broker-dealers effectively pay higher fees than larger brokers to trade on most exchanges. We have heard from a number of market participants that volume-based transaction pricing along with related market practices raise concerns about competition in the markets. I am pleased to support this proposal because it will elicit important public feedback on how the Commission can best promote competition amongst equity market participants.”

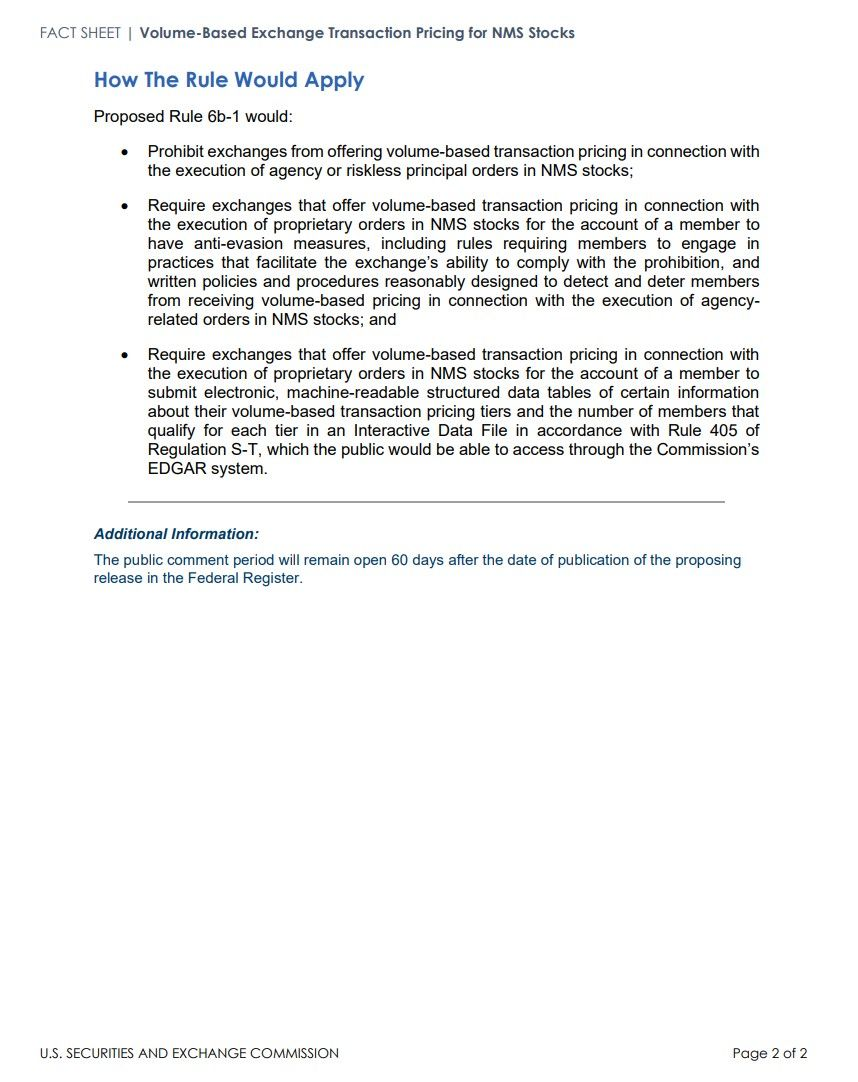

Proposed Rule 6b-1 under the Securities Exchange Act of 1934 would prohibit national securities exchanges from offering volume-based transaction pricing in connection with the execution of agency-related orders in NMS stocks. It also would require exchanges that offer volume-based transaction pricing in connection with the execution of members’ proprietary orders in NMS stocks to disclose certain information, including the number of members that qualify for each transaction pricing tier that the exchange offers. Exchanges would be required to submit this information to the Commission on a monthly basis, and the public would be able to access the information through the Commission’s EDGAR system.

In addition, proposed Rule 6b-1 would require exchanges that have volume-based transaction pricing for member proprietary orders in NMS stocks to have anti-evasion measures, including rules requiring members to engage in practices that facilitate the exchange’s ability to comply with the prohibition on volume-based exchange transaction pricing for agency-related orders in NMS stocks and to have written policies and procedures reasonably designed to detect and deter members from receiving volume-based pricing in connection with the execution of agency-related orders in NMS stocks.

The proposing release will be published in the Federal Register. The public comment period will remain open until 60 days after the date of publication of the proposing release in the Federal Register.

How to comment:

Electronic Comments:

- Use the Commission’s online form at: https://www.sec.gov/rules/2023/10/feetiers

- Alternatively, send an email to [email protected]. Ensure the subject line includes the file number S7-18-23.

Paper Comments:

- Mail your paper comments to: Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

Important Notes:

- Always refer to the file number S7-18-23 in your submission.

- If using email, include the file number in the subject line.

- For efficiency, only use one method of submission.

- All comments will be posted on the Commission’s website at: https://www.sec.gov/rules/proposed.shtml

- Refrain from including personal details in your comments. Only provide information you're comfortable being public.

- Obscene or copyrighted material may be redacted or not published.

TLDRS:

- SEC Proposes Rule to Address Volume-Based Exchange Transaction Pricing for NMS Stocks.

- SEC Commissioner Mark Uyeda: "Ultimately, given the anticompetitive harms likely associated with the proposal—which will harm smaller entities and retail investors—I cannot support it."

- "The Commission’s proposal would preclude the availability of the benefits of volume-based discounts that would have been enjoyed by small proprietary traders—as customers of broker-dealers—but leave those same benefits in place for large proprietary traders who do not require such broker-dealer intermediation. How would this action benefit competition? How would it benefit retail investors?"

- "Given the shift in incentives entailed by prohibiting volume-based discounts, the added anticompetitive burden on small broker-dealers—who may no longer be able to purchase transactional access services from other broker-dealers at as low a cost as previously—is the same as it is for the small proprietary traders."

- "In securities markets, liquidity begets liquidity and, for this reason, there will be a certain degree of market concentration that prevails among exchange platforms."

- "Ultimately, given the anticompetitive harms likely associated with the proposal—which will harm smaller entities and retail investors—I cannot support it."

Proposed Rule 6b-1 would:

- Prohibit exchanges from offering volume-based transaction pricing in connection with the execution of agency or riskless principal orders in NMS stocks.

- Require exchanges that offer volume-based transaction pricing in connection with the execution of proprietary orders in NMS stocks for the account of a member to have anti-evasion measures, including rules requiring members to engage in practices that facilitate the exchange’s ability to comply with the prohibition, and written policies and procedures reasonably designed to detect and deter members from receiving volume-based pricing in connection with the execution of agency related orders in NMS stocks.

- Require exchanges that offer volume-based transaction pricing in connection with the execution of proprietary orders in NMS stocks for the account of a member to submit electronic, machine-readable structured data tables of certain information about their volume-based transaction pricing tiers and the number of members that qualify for each tier in an Interactive Data File in accordance with Rule 405 of Regulation S-T, which the public would be able to access through the Commission’s EDGAR system.

- OPEN FOR COMMENT!