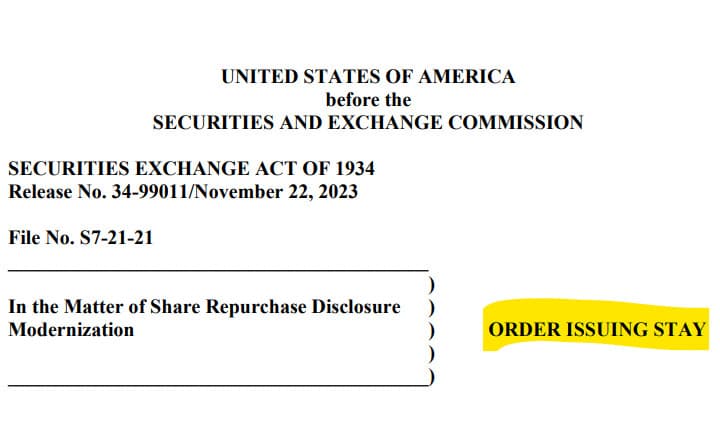

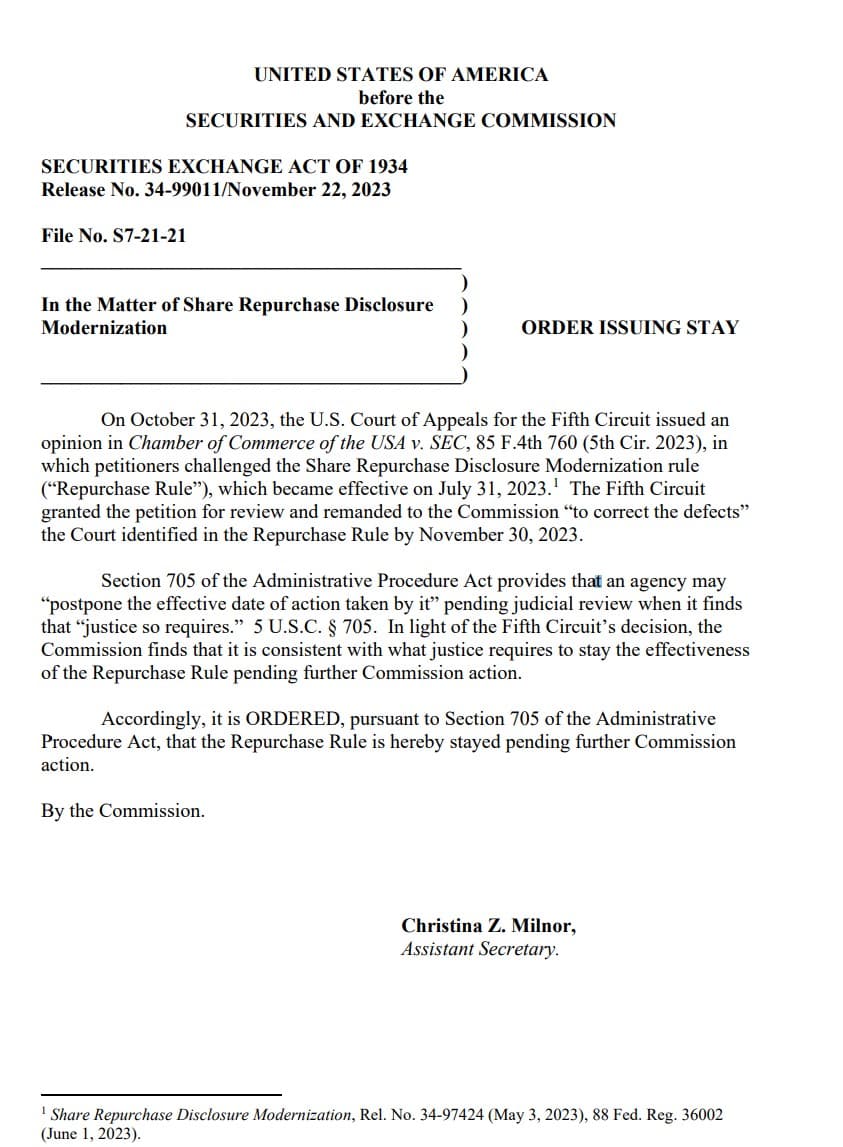

SEC Alert! An order issuing a stay has been granted for the Share Repurchase Disclosure Modernization Rule. Rule now on hold due to Chamber of Commerce of the USA suing the SEC about the rule.

What are they so upset about?

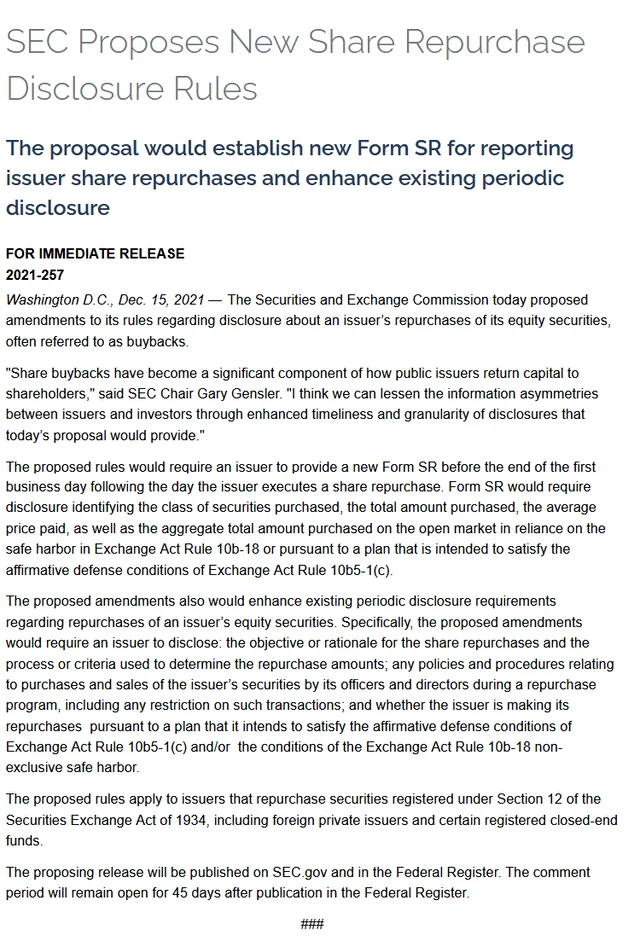

The proposed rules would require an issuer to provide a new Form SR before the end of the first business day following the day the issuer executes a share repurchase. Form SR would require disclosure identifying the class of securities purchased, the total amount purchased, the average price paid, as well as the aggregate total amount purchased on the open market in reliance on the safe harbor in Exchange Act Rule 10b-18 or pursuant to a plan that is intended to satisfy the affirmative defense conditions of Exchange Act Rule 10b5-1(c).

Commissioner Hester M. Peirce on proposed share repurchase disclosure modernization: "Despite this commendable and much needed change, I cannot support a rule that mandates immaterial disclosures without sensible exemptions. Accordingly, I dissent."

She CANNOT support requiring large hedge fund advisers to file a current report as soon as practicable, but no later than 72 hours from the occurrence of one or more trigger events:

Current Reporting for Large Hedge Fund Advisers and Quarterly Event Reporting for All Private Equity Fund Advisers

Currently, advisers to private funds file Form PF on a quarterly or annual basis, depending on the size and type of private funds they advise. The amendments to Form PF will also require large hedge fund advisers to file a current report as soon as practicable, but no later than 72 hours from the occurrence of one or more trigger events. Such trigger events will include certain extraordinary investment losses, significant margin and default events, terminations or material restrictions of prime broker relationships, operations events, and events associated with withdrawals and redemptions.

Statement:

Thank you, Chair Gensler. As you have heard, the final rule scraps the proposed requirement to disclose share repurchases within one business day. Despite this commendable and much needed change, I cannot support a rule that mandates immaterial disclosures without sensible exemptions. Accordingly, I dissent.

The release fails to demonstrate a problem in need of a solution. The release hints at discomfort with issuer share repurchases and suggests that granular disclosure might unearth nefarious practices related to buybacks. The release points out that share repurchases could be “conducted to increase management compensation or to affect various accounting metrics,” rather than to increase firm value.[1] Some people would argue that issuers should use excess cash to increase employee wages or fund research and development. In some cases, these buyback critics may be correct, but share repurchases are not inherently problematic. To the contrary, they enable companies to return excess cash to shareholders with greater tax-efficiency than dividends.[2] Shareholders who choose to sell their shares back to the company then can reinvest the proceeds into companies that need cash. The net result is that capital flows to where it can best be used. Issuers also sometimes repurchase shares for other legitimate purposes, including to “offset dilution from equity compensation plans, or [as] an appropriate investment when shares are viewed as undervalued.”[3]

The implicit skepticism of issuer repurchases is out of step with the SEC staff’s work on the issue. A 2020 SEC staff study found that repurchases help issuers “maintain optimal levels of cash holdings and minimize their cost of capital” and “on average” have “a positive effect on firm value.”[4] The study also found that increasing or meeting executive compensation levels or meeting “earnings-per-share (EPS)-based performance targets” is “unlikely” to motivate “most repurchase activity.”[5] Other studies have made similar findings.[6] Regardless of whether the findings of the staff study or the sentiment in this release are correct, in a free economy government should not micromanage corporate decisions—even implicitly through onerous disclosure requirements—about whether to use excess cash to buy back shares or for some other purpose.

The final rule, although it wisely backs off essentially real-time disclosure of issuer buybacks, is flawed in its granularity. The reasonable investor does not need to know about every repurchase by every public issuer. Disclosure of daily repurchase information will “bury [investors] in an avalanche of trivial information[,] a result that is hardly conducive to informed decisionmaking.”[7] The release justifies the daily mandate by explaining that “investors cannot currently be certain that any given repurchase in fact conveys information about the issuer’s fundamental value.”[8] Even though the release acknowledges that “many, perhaps even most, share repurchases are not undertaken solely or primarily to benefit managers or to achieve targets, such as those based on EPS,” it worries that this “fact . . . does not aid investors who are attempting to assess the efficiency of, and information conveyed by, any given repurchase by a particular issuer.”[9] True, and they also cannot be certain that every decision regarding a research and development project and or capital investment is efficient and undertaken with pure motives. Yet we do not require the level of disclosure we are requiring here. In many areas, a company’s officers and directors could have wrong motives for their decisions, but the antidote is not requiring companies to describe in painstaking detail every corporate action. As several commenters noted, we risk creating “white noise,” the contextless volume of which could confuse investors. [10]

The immateriality of the mandated disclosure calls into question the benefits of the rule, but the rule’s costs are also a concern. Even with the delayed disclosure, the daily repurchase information could publicly release confidential information, including, in narrow cases, pending merger or acquisition activity[11] or other confidential corporate actions.[12] The provision of the required information, even on the timeline required by the final rule, will impose costs on companies, particularly as they will have to produce the data in structured format.[13] Other elements of the rule may also prove to be costly, including requiring issuers to disclose their rationale behind share repurchase activity, and provide their policies and procedures about executive sales during repurchase programs.

In light of the rule’s questionable benefits, the Commission’s refusal to make reasonable accommodations for small and foreign issuers is puzzling. For example, the Commission could have accommodated smaller reporting companies by providing an extended compliance period or at least temporary relief from the structured data requirements. The Commission also could have adhered to the historical treatment of foreign private issuers (“FPIs”).[14] Instead of deferring to FPIs’ home country regulators, the rule requires them to file on the same quarterly schedule as domestic issuers. If this immaterial information warrants quarterly reporting, will we stop making sensible accommodations to FPIs in other areas as well? The Commission also failed to respond adequately to the unique considerations raised about the new requirement’s application to closed-end funds and banks.[15] Finally, the release imposes unnecessarily aggressive compliance deadlines.

The final rule is not as bad as it could have been,[16] but better-than-it-might-have-been is not my standard for supporting a final rule. That said, I am thankful to staff across the Commission for their hard work on this release and for their engagement with me on it. As always, their work is excellent. Among others, I want to thank staff in the Divisions of Corporation Finance, Investment Management, Economic and Risk Analysis, the Office of General Counsel, and others throughout the Commission.

TLDRS:

- An order issuing a stay has been granted for the Share Repurchase Disclosure Modernization Rule. Rule now on hold due to Chamber of Commerce of the USA suing the SEC about the rule.

- The proposed rules would require an issuer to provide a new Form SR before the end of the first business day following the day the issuer executes a share repurchase.

- Form SR would require disclosure identifying the class of securities purchased, the total amount purchased, the average price paid, as well as the aggregate total amount purchased on the open market in reliance on the safe harbor in Exchange Act Rule 10b-18 or pursuant to a plan that is intended to satisfy the affirmative defense conditions of Exchange Act Rule 10b5-1(c).