Senator Sherrod Brown to Secretary of the Treasury Janet Yellen: FSOC Must Be There to Protect Our Economy When Wall Street Tries to Duck Regulators.

Financial Stability Oversight Council Annual Report to Congress

For a long time, it’s been pretty clear what gets rewarded on Wall Street.

Bigger risks mean bigger profits. Bigger profits mean more stock options. Bigger profits mean fatter bonuses. And then, we end up with a Wall Street culture that glorifies seeing just how much you can get away with.

Executives know that when big bets pay off, they get to cash out. And when those bets fail, they won’t have to clean up the mess – workers and taxpayers will, always.

That’s what financial fiascoes boil down to: the Wall Street system encourages bad decisions – and leads to an economy of excess for executives and a shrinking middle class. It’s how we get East Palestine. It’s how we get the CEO of Stellantis making 365 times what their average worker makes.

We saw that story play out just 11 months ago.

Executives at SVB and the other poorly run banks put profits ahead of basic risk management.

Then, as the banks imploded, small businesses all over the country worried how they’d make payroll if they couldn’t access their deposits. Families asked themselves if their money would be safe. So regulators had to step in to protect our economy, while the executives got off scot-free.

2008 was the same story, too—just on a far bigger scale.

Wall Street took big risks with Americans’ money, just like SVB did. Wall Street figured out it could make even bigger bets by exploiting gaps in our regulatory system—always enticed by huge bonuses. Risk-taking built up in the shadows until it was too late to contain.

We all know how that turned out. Chaos on Wall Street put 9 million Americans out of work. Millions lost their homes and their wealth to foreclosure—I saw it in my neighborhood in Cleveland. Our zip code – 44105 – had more foreclosures than any other zip code in the country in the first half of 2007.

A mess that started in New York board rooms with big, barely supervised Wall Street companies then spread to neighborhoods around the country, swallowing up Americans’ jobs and homes and livelihoods.

Some would like to dismiss this as it’s all in the past, it’s all ancient history, it’s a once-in-a-century catastrophe that we don’t need to worry about anymore.

But 2008 showed us how Wall Street is always trying to hide the same old risky behavior in new terms that their PR team cooked up. They’re not going to give up finding new ways to get around the rules so they can make bigger bets to make bigger profits.

But when we let them get away with it, with no oversight or safeguards, Americans pay the price. We’ve seen it too many times.

That’s why, fourteen years ago, we created the Financial Stability Oversight Council—a council of all our financial regulators, which Secretary Yellen chairs.

FSOC’s job is to monitor and respond to financial risk wherever it develops. While other regulators only police some kinds of businesses, FSOC takes a 30,000-foot view of our financial system. When Wall Street and its high-priced lawyers try to avoid the rules, FSOC can react.

FSOC’s job is to close gaps in our regulatory system, covering blind spots that any one agency might have. It can also make sure safeguards are in place at the biggest, riskiest financial companies.

It plays a critical role in stopping the next AIG from blowing a hole in our economy. And FSOC is a key piece of how we end the cycle of bailouts and golden parachutes for executives, with workers stuck with the consequences.

Today, FSOC is as important as ever.

Right now, nonbank financial companies–hedge funds, private equity firms, insurance companies, clearinghouses–hold nearly 20 trillion dollars in assets.

And over the last decade, they’ve grown larger and larger. These days, these companies are responsible for a lot of the activity on Wall Street.

Some of these firms sit in the middle of our biggest markets. Others lend our biggest employers the cash to make payroll. Many finance buyouts, service mortgages, or make huge bets with billions of dollars—often using money from workers’ pensions.

Because these companies have become so central to our markets, it would be all too easy for just one of them to drag down our financial system.

And they have the same deep-rooted temptation to take on more risk for a big payday as anyone else on Wall Street – sometimes they’re even riskier.

And we all know that if one of these firms collapsed, the executives would be just fine. But most of the country wouldn’t.

That’s why FSOC is so important. When Wall Street tries to shapeshift to evade the watchdogs we depend on, FSOC must be there to take action to protect our economy.

Of course, it’s not a surprise that Wall Street and its well-funded allies have always wanted to kill anything that tries to hold it accountable. Their lobbyists viciously fought to try to stop us from implementing the Dodd-Frank reforms.

After we passed it, the chief lobbyist for the Financial Services Roundtable said “now it’s halftime.”

And now they’ve tasked their lobbyists with trying to block the Council from doing its job, forcing it to sit on its hands as risk builds up. They want to take away some of our most important tools for keeping our economy safe from reckless Wall Street behavior.

FSOC makes Wall Street nervous—nervous that FSOC could bring oversight and accountability to parts of Wall Street that wouldn’t otherwise get it.

The last administration worked hard to handcuff FSOC by undermining its ability to impose safeguards at the riskiest financial firms. The message to Wall Street was clear: FSOC isn’t really watching and won’t really act.

That is changing now. Today FSOC is far better positioned to make sure that bad bets anywhere on Wall Street don’t crush Main Street.

The Council is also focused on responding to new, emerging risks to our financial system. These are risks we’ve talked about on this Committee before—risks like digital assets, cybercrime, the changing climate, and artificial intelligence—–as well as the old risks that are as present as ever, like shadow banks. FSOC is also monitoring how the commercial property market is affecting our banking system—an important concern given what we’ve seen this week.

Secretary Yellen is responsible, too, for Treasury’s critical work to safeguard our national security by cracking down on illicit finance. I look forward to working with her to combat all the ways that bad actors like Hamas and Iran are funding their activities—including with new tools, like digital assets.

Ultimately, we cannot allow another financial crash, wherever the risks may come from, to set workers and consumers back.

Instead, we need an economy where hard work – not financial speculation – pays off. A system that works for everyone, not just big corporations and hedge funds and their lobbyists.

We know we’re still far from that economy – you only have to look at corporate profiteering the in the last few years. Every time Americans go to the grocery store, they’re paying for stock buybacks and executive bonuses.

And it’s what we see now with the big banks—throwing millions of dollars at a PR campaign to stop capital rules that will make sure that taxpayers don’t have to bail out another bank failure. All to keep profits high.

While I’ve been Chair of this Committee, I’ve worked every day to end a system that rewards risky behavior with piles of company stock and huge cash bonuses, instead of real accountability.

That’s why this Committee passed the bipartisan RECOUP Act last year—to crack down on a broken system.

And ultimately, that’s why we created FSOC, whose mission is so important today.

Secretary Yellen, thank you for being here this morning. I look forward to hearing about FSOC’s work to safeguard our financial system.

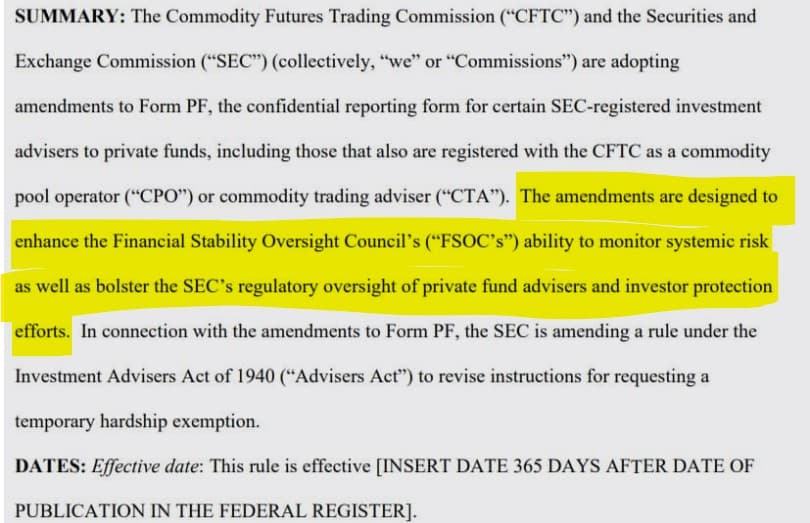

As we saw yesterday, FSOC got a boost with Form PF; Reporting Requirements for All Filers and Large Hedge Fund Advisers

Wut Mean?

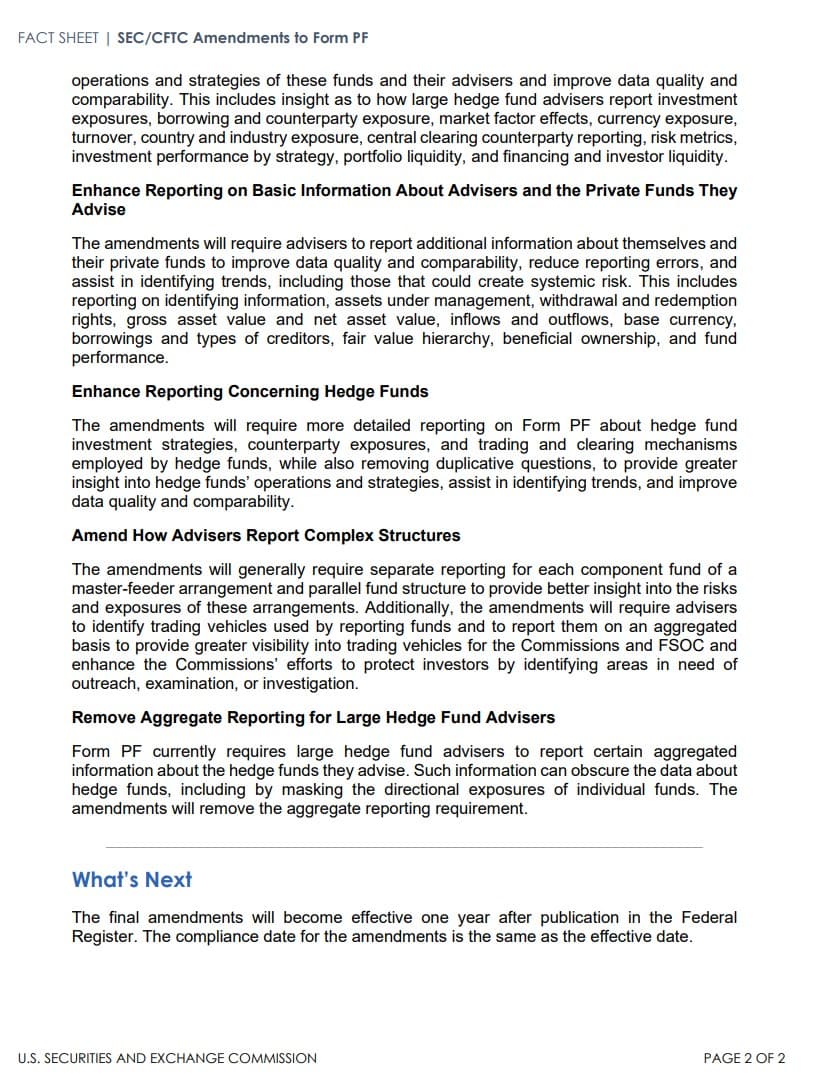

Among other things, the amendments to Form PF will enhance how large hedge fund advisers report investment exposures, borrowing and counterparty exposure, market factor effects, currency exposure, turnover, country and industry exposure, central clearing counterparty reporting, risk metrics, investment performance by strategy, portfolio liquidity, and financing and investor liquidity to provide better insight into the operations and strategies of these funds and their advisers and improve data quality and comparability.

Further, the amendments will require additional basic information about advisers and the private funds they advise, including identifying information, assets under management, withdrawal and redemption rights, gross asset value and net asset value, inflows and outflows, base currency, borrowings and types of creditors, fair value hierarchy, beneficial ownership, and fund performance to provide greater insight into private funds’ operations and strategies, to assist in identifying trends, including those that could create systemic risk, to improve data quality and comparability, and to reduce reporting errors.

The amendments will also require more detailed information about the investment strategies, counterparty exposures, and trading and clearing mechanisms employed by hedge funds, while also removing duplicative questions, to provide greater insight into hedge funds’ operations and strategies, to assist in identifying trends, and to improve data quality and comparability.

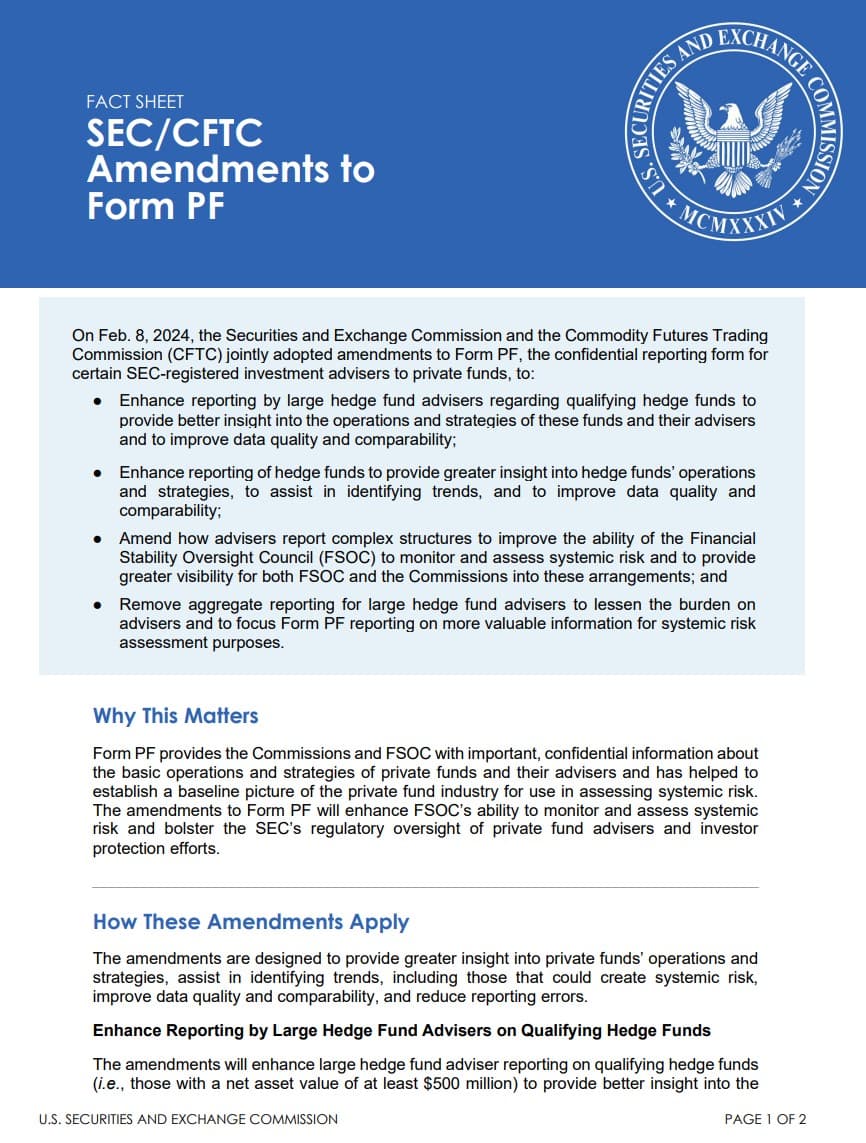

Fact Sheet

What Others are saying about this:

SEC Chair Gary Gensler: "I am pleased to support the adoption because it will improve the quality of the information we receive, particularly from large hedge fund advisers. This will help the SEC & FSOC to better assess systemic risk and protect investors."

Statement on Final Joint Amendments to Form PF

Today, the Commission voted to adopt amendments to Form PF, an important reporting tool whereby the Commission and the Financial Stability Oversight Council (FSOC) receive reporting from private fund advisers. I am pleased to support the adoption because it will improve the quality of the information we receive, particularly from large hedge fund advisers. This will help the SEC and FSOC to better assess systemic risk and protect investors.

Lest we forget, as a result of the 2008 financial crisis, eight million Americans lost their jobs, millions of Americans lost their homes, and small businesses across the country folded. Systemic risk from the banking and non-bank sectors alike spilled out into the broader economy.

In response to the 2008 crisis, Congress mandated that the SEC and the Commodity Futures Trading Commission (CFTC) adopt rules to establish reporting requirements for private funds. This reporting is to be “as necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk.” Thus, the two commissions jointly adopted Form PF in 2011.

I had the privilege to serve as Chair of the CFTC at the time. As I said when Form PF first was adopted, “With this final rule, regulators will gain transparency into an important sector of the financial marketplace to better assess risk to the overall system.”[1]

Private funds have evolved significantly in the 13 years since Form PF first was adopted. Further, private funds today are ever more interconnected with the broader capital markets.

Private funds nearly have tripled in size in the last decade to approximately $26 trillionin gross assets.[2] This compares with the U.S. commercial banking industry of approximately $23 trillion.[3] This makes visibility into these funds critical.

Since Form PF first was adopted, the Commissions and FSOC have identified gaps in the information we receive. Today’s adoption enhances the Commissions’ and FSOC’s understanding of the private fund industry as well the potential systemic risk posed by the industry and its individual participants. In addition, the adoption also furthers investor protection efforts.

Today’s final rules concern the Commissions’ joint sections on Form PF. These amendments will, among other things, expand the reporting requirements for large hedge fund advisers on their large hedge funds in three important ways.[4]

First, the final rules will expand reporting requirements about a large hedge fund’s investment exposures. Reporting on fund exposures to different types of assets has been critical to help monitor the risks that large hedge funds may present to the markets. Expanding such reporting from large hedge fund advisers will enhance investor protection efforts and the assessment of systemic risk.

Second, the final rules will expand reporting requirements about a large hedge fund’s open positions and certain large positions. These requirements will provide insight into the extent of a fund’s portfolio concentration and large exposures to any specific assets. Such concentration or exposure may increase the risk of amplified losses for investors. Gathering additional data on concentration and exposure will help to protect investors and assess systemic risk.

Third, the final rules will expand reporting requirements on large hedge funds’ borrowing and financing arrangements with counterparties, including central clearing counterparties. Gathering such information will help the Commissions and FSOC better to observe how hedge funds interconnect with the broader financial services industry.

In finalizing this adoption, we benefitted from public feedback on our proposed rules and made a number of appropriate changes.

Today’s adoption is the third step the Commission has taken in the last two years to update disclosure of this important sector of the capital markets.

First, in May 2023, we adopted requirements for certain advisers to hedge funds and private equity funds to provide current reporting of key events. Those rules also enhance reporting requirements for large private equity fund advisers. The first phase of the implementation went into place in December 2023.

Second, in July 2023, we finalized amendments to Form PF for large liquidity fund advisers to align their reporting requirements with those of money market funds.

Third is today’s adoption. I believe that these final rules will bring greater visibility for regulators into an important part of our capital markets. That will help protect investors and maintain fair, orderly, and efficient markets.

In addition to the adoption of these final rules, the Commission today also entered into a memorandum of understanding with the CFTC to facilitate data sharing between our agencies regarding information submitted to us on Form PF. I believe such data sharing will help our Commissions coordinate in overseeing this important area of the capital markets.

I’d like to thank members of the SEC staff for their work on these final rules, including:

William Birdthistle, Sarah ten Siethoff, Melissa Harke, Adele Murray, Tom Strumpf, Jill Pritzker, Neema Nassiri, Timothy Husson, David Stevens, Jon Hertzke, Michelle Beck, Holly Miller, Timothy Dulaney, Kevin Treharne, Trevor Tatum, Steve Flantsbaum, and Kolby Quass in the Division of Investment Management;

Jessica Wachter, Charles Woodworth, Ross Askanazi, Caroline Schulte, Dan Hiltgen, Michael Davis, and Rachel Li in the Division of Economic and Risk Analysis;

Meridith Mitchell, Natalie Shioji, Monica Lilly, and Alice Wang in the Office of the General Counsel;

Christopher Mulligan and Daniel Faigus in the Division of Examinations; and

Nikolay Vydashenko in the Division of Enforcement.

[1] SeeCommodity Futures Trading Commission, “CFTC and SEC Approve Confidential Private Fund Risk Reporting” (Oct. 31, 2011),available athttps://www.cftc.gov/PressRoom/PressReleases/6132-11.

[2] See Form ADV data (inclusive of assets attributable to securitized asset funds).

[3] SeeBoard of Governors of the Federal Reserve System, “Assets and Liabilities of Commercial Banks in the United States” (Feb. 2, 2024),available athttps://www.federalreserve.gov/releases/h8/current/default.htm. Total assets of approximately $23.3 trillion as of Jan. 24, 2024 (Table 2, Line 33).

[4] As detailed in the Adopting Release, the amendments will apply to hedge funds with at least $500 million in net asset value, also known as qualifying hedge funds.

Commissioner Hester M. Peirce: "I write to dissent from the latest unwarranted expansion of Form PF. These revisions stem from the Commission’s unbridled curiosity rather than from a legitimate regulatory objective."

I write to dissent from the latest unwarranted expansion of Form PF. These revisions stem from the Commission’s unbridled curiosity rather than from a legitimate regulatory objective. In 2010, Congress established the Financial Stability Oversight Council (“FSOC”) and charged it with, among other things, “identify[ing] risks to the financial stability of the United States.”[2] Congress directed the Securities and Exchange Commission (“SEC” or “Commission”) and the Commodity Futures Trading Commission (“CFTC”) (collectively, “Commissions”) to provide some of the information FSOC would need to fulfill its duties, and so in 2011 Form PF was born.[3]

At its inception, the Commissions acknowledged that, while Form PF data could be used for their own regulatory purposes, Form PF’s primary function was “to collect information . . . to assist FSOC in its monitoring obligations.”[4] Since that time, however, respect for Form PF’s primary purpose has given way to curiosity. We pair as co-equal FSOC’s use of Form PF data to “monitor[] and assess[] systemic risk” with our own desire “to collect additional data and make data more useful for the Commissions’ use in their respective regulatory programs.”[5] Relying on both these purposes, we are expanding dramatically the information Form PF collects.

In the Form’s early days, we were comfortable with its limitations. We stated clearly, for instance, that “[w]e have not sought to design a form that would provide FSOC in all cases with all the information it may need to make a determination that a particular entity should be designated for supervision by the [Federal Reserve Board].”[6] We recognized that the cost of demanding more information from all fund advisers would outweigh the benefits. Our sensibilities have changed in the intervening thirteen years, and Form PF is being amended to accommodate them.[7]

Despite this attitudinal shift, we continue to provide occasional lip service to the idea that these amendments have been made largely in pursuit of improving the identification and monitoring of systemic risk. As one commenter correctly highlighted, however, neither we nor the CFTC “describe[s] the types of activities that may give rise to systemic risk, nor do [we] describe how the proposed reporting requirements are specifically tailored to identify and effectively monitor these activities.”[8] Form PF has not-so-subtly morphed into an all-purpose means to gather information from the private market under the seemingly limitless rubric of systemic risk. Through strained logic, we manage to transform one-off reports describing the idiosyncrasies of individual private funds into harbingers of market-wide contagion.

Our apparent inability to articulate a rationale for compelling more data has in no way blunted our craving for it—in fact, it appears to have stoked it. Absent any discernible limiting features, we have seemingly decided that all gaps are created equal and filling them provides its own justification. Even a partial list of the additional data we will now collect with these revisions is dizzying.[9] As one commenter put it, “the Commissions appear to believe that monitoring for systemic risk and protecting investors may only be conducted by having access to every piece of fund-related data.”[10] A systemic risk regulator does not need to know everything about every entity.

Boundless curiosity is wonderful in a small child; it is a less attractive trait in regulatory agencies. As diligent regulators we should want to know why market disturbances occur, or even prevent them if we can do so without exceeding our statutory mandates. But we chase a white whale if we believe we are but one discrete piece of information away from being able to prevent the next Flash Crash or Global Financial Crisis.

We insist, for instance, that each component fund in a master-feeder arrangement be reported separately. We ignored commenters who pointed out that disaggregation makes little sense in light of how private funds manage risk[11] and that the information submitted will be of little use to the Commission.[12] We dismiss these concerns by stating that this fund-level data “allows for a clearer understanding of the reporting fund’s structure, including its portfolio liquidity.”[13] And besides, we say, “the disaggregated data can still be aggregated by FSOC and the Commissions if necessary to understand and assess the risk of the fund.”[14] The Commissions similarly reject a commonsense request for an exception to allow disregarded feeder funds to invest a de minimis amount in something other than a single master fund, U.S. treasury bills, or cash and cash equivalents.[15] Even a ten percent exception could cloud “our understanding of these funds and the risks they may pose.”[16] We likewise said no to calls to carve out certain private funds from the definition of hedge fund—such as private funds that can short or use leverage, but do not engage in those activities for a specified period of time.[17] Allowing carveouts from the definition, we determined, among other problems, would mean that we “would not receive important reporting on these activities which may contribute to systemic risk, particularly in the event of a fund that has the ability to engage in borrowing or short selling activities.”[18]

We do not have the better argument here. We have failed to explain why we must collect a small, unrepresentative component of the whole in order to fulfill Form PF’s purpose. Systemic risk involves the forest—trying to monitor the state of every individual tree at every given moment in time is a distraction and trades off the mistaken belief that we have the capacity to draw meaning from limitless amounts of discrete and often disparate information. Unbridled curiosity seems to be driving this decision rather than demonstrated need.

In our never-satisfied hunger for more particularized information, we too casually ignore concerns about cost, utility, and data protection. Form PF contains highly proprietary information. Unless we need it, we should not collect it. The leakage of such confidential business information could have serious competitive repercussions. What we put forward as streamlining of Form PF’s data gathering effort—say the drop-down menus to assist a filer in identifying its investment strategy,[19] or the introduction of sub-asset classes—commenters rightly see as costly fact-gathering endeavors of little value that create an increasingly tempting target for cyberthieves.[20] Our curiosity could have serious consequences—“an intrusive path into the proprietary workings of fund managers under the guise of regulatory ‘need to know’.”[21] Ensuring that the data we collect are used only for their intended regulatory purposes is a very weighty responsibility—so weighty that it ought to have us thinking twice about collecting data that is not needed for systemic risk assessment.

Moreover, as one commenter suggests, perhaps we should ensure that we have fully used the information we already receive before adding to private funds’ reporting burden.[22] Given that the last amendments are less than a year old, private funds might justifiably be feeling Form PF fatigue.[23]

The final rule does incorporate some commenter suggestions to reduce the costs and burdens and duplication associated with some of the proposal’s features,[24] which could indicate that the notice and comment process has worked as designed. Far from it. The Commissions dismissed far too many comments calling for revisions or relief, but more troubling, countless numbers of similar pleas likely were never submitted. By my count, we acknowledge that the Commissions received no comment on an element of the proposal more than 40 times in this release. Overburdened commenters are forced to pick and choose among hundreds of questions posed in this and other releases. They concentrate their limited time and strained resources on those matters they believe will be particularly disruptive.[25] With so many questions going unaddressed, we cannot be confident that we have a clear understanding of what the true costs of these amendments will be, let alone whether they are justified. For these reasons and others, I cannot support this rule.

Commenters are not alone in being overburdened. I am grateful to the hardworking staff of the Securities and Exchange Commission and the CFTC. Form amendments can be particularly challenging, especially with respect to a joint form such as this one and without the benefit of comment on many sections of the proposal. I commend the staffs of both agencies for their diligence and professionalism.

[1] Lewis Carroll, Alice’s Adventures in Wonderland, at 2.

[2] Dodd-Frank § 112(a)(1).

[3] Dodd-Frank §§ 404 (adding 15 U.S.C. 80b-4(b)(1)) (in a section titled “Collection of Systemic Risk Data; Reports; Examinations; Disclosures”) and 406 (adding 15 U.S.C. 80b-11) (requiring the SEC and CFTC, after consulting with FSOC, to “jointly promulgate rules to establish the form and content of the reports required to be filed with the Commission under subsection 204(b)”).

[4] See Reporting by Investment Advisers to Private Funds and Certain Commodity Pool Operators and Commodity Trading Advisors on Form PF, Investment Advisers Act Release No. 3145 (January 26, 2011) ("Original Proposal”), at 17 https://www.sec.gov/files/rules/proposed/2011/ia-3145.pdf (“While we are proposing to collect information on Form PF to assist FSOC in its monitoring obligations under the Dodd-Frank Act, the information collected on Form PF would be available to assist the Commissions in their regulatory programs, including examinations and investigations and investor protection efforts relating to private fund advisers. We have designed Form PF, in consultation with staff representing FSOC’s members, to provide FSOC with such information so that it may carry out its monitoring obligations.”).

[5] Adopting Release at 5-6 (“Based on this experience and in light of these changes, the Commissions and FSOC have identified significant information gaps and situations where revised information would improve the Commissions’ and FSOC’s understanding of the private fund industry and the potential systemic risk posed by it, as well as further investor protection efforts. Accordingly, to enhance FSOC’s monitoring and assessment of systemic risk and to collect additional data and make data more useful for the Commissions’ use in their respective regulatory programs, in August 2022, the Commissions proposed amendments to enhance the information advisers file on Form PF and improve data quality.”) (emphasis added).

[6] Original Proposal at 18 (“We have not sought to design a form that would provide FSOC in all cases with all the information it may need to make a determination that a particular entity should be designated for supervision by the FRB. Such a form, if feasible, likely would require substantial additional and more detailed data addressing a wider range of possible fund profiles, since it could not be tailored to a particular adviser, and would impose correspondingly greater burdens on private fund advisers. This type of information gathering may be better accomplished by OFR through targeted information requests to specific private fund advisers identified through

Form PF, rather than through a general reporting form.”) (internal citations removed).

[7] See, e.g., Adopting Release at 205-6 (“However, we continue to believe that a private fund of any size that provides for withdrawal or redemption rights may be affected by increased investor withdrawals during certain market events and/or vulnerable to failure as a result of investor redemptions, and so the additional data will be relevant for assessing broader systemic risk, for example by allowing the Commissions and FSOC to assess the prevalence of the exercise of withdrawal and redemption rights to identify potential patterns among affected funds that may signal stress at a particular fund or across many funds.”) (emphasis added).

[8] See, e.g., Comment Letter from SIFMA-AMG at 4 (Oct. 11, 2022) (“The Commissions, however, do not describe the types of activities that may give rise to systemic risk, nor do they describe how the proposed reporting requirements are specifically tailored to identify and effectively monitor these activities.”), https://www.sec.gov/comments/s7-22-22/s72222-20145436-310658.pdf. (“SIFMA-AMG Letter”)

[9] See, e.g., Adopting Release note 552 (“Other revisions that will provide this benefit include revising reporting of regulatory versus net assets under management; reporting of assumptions the adviser makes in responding to questions on Form PF; reporting of types of fund; reporting of master-feeder arrangements, internal/external private funds, and parallel fund structures; reporting of monthly gross and net asset values; reporting of the value of unfunded commitments; reporting on the value of borrowing activity; reporting of fair value hierarchy; reporting of beneficial ownership; reporting of fund performance; more granular reporting of hedge fund strategies; more granular reporting of hedge fund counterparty exposures including identification of counterparties representing a fund’s greatest exposure; and more granular reporting of hedge fund trading and clearing mechanisms.”).

[10] SIFMA-AMG Letter at 4 (“Rather, the Commissions appear to believe that monitoring for systemic risk and protecting investors may only be conducted by having access to every piece of fund-related data. Gathering granular data from all investment advisers does not inherently equate to systemic risk monitoring.”).

[11] See, e.g., Comment Letter from the Managed Fund Association at 3 (Dec. 7, 2022) (“Although advisers may form master-feeder structures and utilize trading vehicles to increase efficiency for investors, the broader private fund structures that those entities are part of are nonetheless managed on a consolidated or aggregated basis. Private fund advisers typically do not manage each feeder fund, master fund or trading vehicle within a private fund structure on a stand-alone basis with respect to risk management, financing, or liquidity. Rather, advisers frequently consider these matters from the perspective of the aggregated, consolidated activities of the private fund structure.”), https://www.sec.gov/comments/s7-22-22/s72222-20152435-320304.pdf. (“MFA Letter”)

[12] See, e.g., Comment Letter from the Alternative Investment Management Association Limited and the Alternative Credit Council at 7 (Oct. 11, 2022) (“We see no reason why advisers should be required to report feeder-level information in a fund of fund structure any differently than they report a one-to-one master-feeder structure, nor do we recognize any purported value this information will provide the Commissions.”), https://www.sec.gov/comments/s7-22-22/s72222-20145440-310665.pdf. ("AIMA Letter”)

[13] Adopting Release at 158 (“[D]isaggregated reporting, rather than being misleading, allows for a clearer understanding of the reporting fund’s structure, including its portfolio liquidity, because we can observe liquidity on a fund by fund basis while continuing to allow aggregation of data across the fund structure for the broader context.”).

[14] Adopting Release at 15.

[15] See AIMA Letter at 9 (“We believe the definition of ‘disregarded feeder’ as set out in proposed Instruction 6 should be revised to read: ‘feeder fund that invests all at least 80% of its assets in (i) a single master fund, and/or (ii) cash and cash equivalents, and/or (iii) government securities.’ This would allow a feeder fund to have a de minimis amount for direct investment which would be particularly helpful where derivatives or other instruments are held for currency class hedging or other reasons.”) (cross-outs and emphasis in the original) (emphasis in original); MFA Letter at 13 ("The Commissions should revise the definition to permit a ‘disregarded feeder fund’ to invest up to 10 percent of its capital in other investments that are not a single master fund or cash equivalents.”).

[16] Adopting Release at 17 (“In contrast, a feeder fund that does not invest all of its assets in a single master fund or cash and cash equivalents operates and invests in a different manner, and it is critical to our understanding of these funds and the risks that they may pose to receive disaggregated reporting of these fund arrangements because such feeder funds will generally have distinct risk exposures than their associated master funds.”).

[17] See, e.g., Comment Letter from the American Investment Council AIC at 8 (Oct. 11, 2022) (“The AIC recommends an amendment to the definition of ‘hedge fund’ to avoid potential data mismatches and to improve data quality as a result of the over-inclusive nature of the definition. Specifically, the AIC recommends that the definition only include funds that have engaged in shorting or borrowing activity over a 12-month period and provide a de minimis exception for shorting activity relative to the size of the private fund.”), https://www.sec.gov/comments/s7-22-22/s72222-20145432-310653.pdf.

[18] Adopting Release at 162.

[19] Adopting Release at 77. The list of strategies from which to choose will undoubtedly cause many filers analysis paralysis, but the Commissions assure us that it will facilitate “more targeted analysis and improve comparability”: equity (and associated sub-strategies such as long/short market neutral, long only, long/short short bias, and long/short long bias), macro (and associated sub-strategies such as active trading, commodity, currency, and global macro), convertible arbitrage, relative value (and associated strategies such as fixed income asset backed, fixed income convertible arbitrage, fixed income corporate, fixed income sovereign, fixed income arbitrage, and volatility arbitrage), event driven (and associated sub-sub-strategies such as distressed, distressed/restructuring, risk arbitrage/merger arbitrage, equity special situations, and special situations), credit (and associated sub-strategies such as asset based lending, litigation finance, emerging markets, and asset backed/structured products), managed futures/CTA (and associated sub-strategies such as fundamental, quantitative), investment in other funds, private credit (and associated sub-strategies such as direct lending/mid-market lending, distressed debt, junior/subordinate debt, mezzanine financing, senior debt, senior subordinated debt, special situations, venture debt, and other), private equity (and associated sub-strategies such as early stage, expansion/late stage, buyout, distressed, growth, private investment in private equity, secondaries, and turnaround), real estate, real estate investment trusts, real assets excluding real estate, annuity and life insurance policies, litigation finance, digital assets, general partner stakes investing, cash and cash equivalents, and other.

[20] See, e.g., SIFMA-AMG Letter at 7 (“Moreover, the Commissions should not seek information in an effort to monitor systemic risk unless that information is narrowly tailored, particularly when that information could give rise to confusion and security concerns. *** Second, the provision of granular sub-asset class information may allow those with access to the information (whether sanctioned or unsanctioned) to recreate a fund’s investment strategy which, if duplicated or made public, in whole or in part, could lead to investor harm instead of the investor protection that the Proposal purports to seek to achieve. We are concerned that the provision of such detailed information could disclose a fund’s investment strategy and, thus, this information should only be provided when there is a true need to have this level of detail about a fund’s investments.”); MFA Letter at 18 (“Further, the requirement to categorize net asset values in many small strategy buckets is unlikely to be useful for regulators and will require extensive calculations and subjective decisions, especially for the large percentage of funds that combine more than one investment strategy.”); AIMA Letter at 6, https://www.sec.gov/comments/s7-22-22/s72222-20145440-310665.pdf (“The systems built to assist with the reporting burden of the current Form PF will need to be broken down and rebuilt from the start in order to properly integrate the new requirements. From a cost and effort perspective, this should be estimated as being tantamount to the original build cost which itself far exceeded the amounts originally estimated by the Commissions.”).

[21] AIMA Letter at 2 (“The resulting massive collection of data from this Proposal, particularly when combined with the requirements of other existing and proposed rules, would represent far more than a necessary window into adviser activity. The granularity of the aggregate data collected would provide an intrusive path into the proprietary workings of fund managers under the guise of regulatory ‘need to know.’”).

[22] See SIFMA-AMG Letter at 4 (“While fund data is informative and interesting, a rulemaking with the goal of monitoring for systemic risk and protect sophisticated investors should meet a higher standard before burdensome reporting is compelled. SIFMA AMG believes that the Commissions should monitor for systemic risk in a more nuanced fashion and should leverage existing data sources when doing so. In addition, the Commissions should provide a robust cost-benefit analysis to support the costs associated with the Proposal’s new reporting requirements in light of the burdens they would introduce.”)

[23] “SEC Adopts Amendments to Enhance Private Fund Reporting.” May 3, 2023, https://www.sec.gov/news/press-release/2023-86. Press release.

[24] See, e.g., Adopting Release at 105 (“One commenter recommended allowing an adviser to select the sub-asset class that ‘best represents’ the position. We believe that adopting a ‘best represents’ standard, regardless of the position size, balances the importance of obtaining more accurate and granular data with a reporting standard that is less burdensome for advisers than the proposed standard.”); and at 188 (“The revisions include changes to instructions for purposes of clarification, revising framing or explanation of questions where commenters made suggestions to improve data quality, revising instructions to avoid duplicative reporting or to otherwise ease burden, or forgoing adopting certain amendments entirely.”).

[25] See, e.g., Comment Letter from Schulte Roth at 2 (Oct. 11, 2022) (“In light of the complexity of the proposals, and the timing of the comment period, it is not feasible to analyze all of the proposed changes, their implications and to identify alternatives. We would welcome the opportunity to have more time to study the proposals and provide additional comments. In the meantime, below are some responses to specific questions about which the Commissions seek comment.”), https://www.sec.gov/comments/s7-22-22/s72222-20145429-310650.pdf.

Commissioner Mark T. Uyeda: "Apparently, every burden the Commission can possibly conjure is necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk by FSOC."

Statement on Form PF; Reporting Requirements for All Filers and Large Hedge Fund Advisers

The latest Form PF amendments – the second set of substantive additions within a year – further expand the scope and granularity of information that private funds must report. The comment file is replete with substantive criticism of the expanded reporting requirements. Administrative agencies like the Commission have an obligation to consider and respond to significant comments received during the period for public comment.[1] Regrettably, the Commission dismisses those concerns with assumptions and unsupported conclusory statements.

For example, commenters expressed concern about disaggregating each component fund of a master-feeder arrangement and parallel fund structure.[2] One commenter explained that disaggregated information would be “misleading and difficult to analyze,” and that it is “not the type of information that the Commissions likely would be able to readily and accurately re-aggregate.”[3] The Commission simply “disagree[s],” that the information would be misleading, and notes that it “could, if necessary, aggregate the data to understand the overall fund.”[4] There is no analysis or evidence to support this response. The response’s “could, if necessary” language does not even imply that the Commission needs this information in the first place.

These form amendments also appear to exceed the authority granted to the Commission by Congress. The Investment Advisers Act of 1940 – as amended by Title IV of the Dodd-Frank Act – authorizes the Commission to require private fund advisers to file reports only if “necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk by [FSOC].”[5] In this manner, Congress limited the Commission’s authority to require private fund advisers to report information on Form PF. However, the Commission only pays lip service to this limitation.

The Commission justifies the various reporting burdens on private fund advisers with a version of the following statement: the new reporting requirement will “[improve] systemic risk assessment and regulator programs to protect investors.”[6] In many cases, the SEC does not even bother to claim that the additional reporting will satisfy the statutory standard, but instead settles for claiming that the reporting may do so.[7]

Apparently, every burden the Commission can possibly conjure is necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk by FSOC. A limitation is meaningless if no regulatory action would ever run afoul of it. As the Supreme Court has approvingly cited, “[a] statute should be construed so that effect is given to all its provisions, so that no part will be inoperative or superfluous, void or insignificant. . .”[8]

The SEC’s interpretation of Title IV of the Dodd-Frank Act has the practical effect of ignoring the limitation imposed by the statute. Adding conclusory references to “systemic risk” and “investor protection” does not satisfy the authority constraints imposed by statute.

The increasing granularity of the Form PF obligations raises important questions about what measures are being taken to protect the investors in the private funds reporting information on Form PF. These investors seem to have been all but forgotten in the Commission’s quest for ever more detailed and faster reporting of private fund information.

As then-Chair Mary Schapiro stated in 2011 when Form PF was first adopted;

I also know that the confidentiality of the information reported on Form PF is very important to those filing the information. The data is sensitive and proprietary and — by Congressional design — non-public. The Dodd-Frank Act contains strong protection for the information filed on Form PF. In addition, we are committed to building the controls necessary to provide appropriate confidentiality and limit the availability of proprietary hedge fund and other private fund information to those who have a regulatory need to know.[9]

Unauthorized disclosure of Form PF information could cause significant damage. Despite the assurances of then-Chairman Schapiro, raw Form PF data is now being widely distributed throughout the Federal government. Federal agencies are under constant threat of cybersecurity incidents. But even with strong cybersecurity and confidentiality protections, it is not possible for the employees, contractors, and third parties who have access to Form PF data to unlearn what they have observed should they leave federal employment and pursue positions in the private sector, such as competitors in the private funds industry.[10]

The Form PF amendments also represent a shocking deficiency in economic analysis. Two days ago, the Commission adopted rules that scope certain private funds into the definition of “dealer” or “government securities dealer” under the Securities Exchange Act of 1934.[11] In declining to exempt private funds from the definition, the Commission stated that “[a]lthough. . .the [SEC] collects some information about certain private funds through Form PF, this reporting alone is not a sufficient substitute for the comprehensive dealer requirements because, it is not as comprehensive.”[12]

Yet the Adopting Release for these Form PF amendments contains no analysis as to whether the new Form PF reporting obligations are appropriate in light of the newly-imposed overlapping dealer registration regime, with its own reporting requirements.[13] Failure to consider these overlapping obligations makes it impossible for the agency to act on a rational basis as required by the Administrative Procedure Act in considering these amendments.

Finally, I am troubled by the Commission’s approach towards smaller asset managers. The Adopting Release acknowledges the possibility that increased compliance costs will cause “smaller advisers to either exit or forgo entry.”[14] The Commission’s assertion that “the final amendments reduce many of the costs of compliance relative to the proposal. . ., [so] these effects may be mitigated, but may nonetheless occur”[15] is not compelling given that the final amendments make only minor changes from the proposal.[16]

The Commission’s war on private funds continues.[17] While I am unable to support today’s amendments, I thank the staff in the Divisions of Investment Management and Economic and Risk Analysis, as well as the Office of the General Counsel, for their efforts.

[1] See Perez v. Mortgage Bankers Association, 575 U.S. 92, 96 (2015), available at https://supreme.justia.com/cases/federal/us/575/92/.

[2] See, e.g., Comment Letter of Managed Funds Association (Dec. 7, 2022), available at https://www.sec.gov/comments/s7-22-22/s72222-20152435-320304.pdf.

[3] Id. at 4.

[4] See Form PF; Reporting Requirements for All Filers and Large Hedge Fund Advisers, Advisers Act Release No. 6546 (Feb. 8, 2024) (“Adopting Release”), at 191, available at https://www.sec.gov/files/rules/final/2024/ia-6546.pdf.

[5] See 15 U.S.C. 80b–4(b).

[6] See, e.g., Adopting Release, at 194.

[7] Id. (“[T]hese industry insights may improve systemic risk assessment and regulator investor protection efforts.”) (Emphasis added.)

[8] See Hibbs v. Winn, 542 U.S. 88, 101 (2004) (citing 2A N. Singer, Statutes and Statutory Construction §46.06, 181-86 (rev. 6th ed. 2000), available at https://supreme.justia.com/cases/federal/us/542/88/.

[9] Chairman Mary Schapiro, Opening Statement at SEC Open Meeting: Private Fund Systemic Risk Reporting (Oct. 26, 2011), available at https://www.sec.gov/news/speech/2011/spch102611mls.htm.

[10] Despite the vast resources of the Federal government, the neuralyzer remains a work of fiction. See Men in Black, Columbia Pictures (1997).

[11] See Further Definition of ‘As a Part of a Regular Business’ in the Definition of Dealer and Government Securities Dealer in Connection with Certain Liquidity Providers, Release No. 34-99477 (Feb. 6, 2024), available at https://www.sec.gov/files/rules/final/2024/34-99477.pdf.

[12] Id. at 71.

[13] The Adopting Release only mentions the amendments to the definition of “dealer” when analyzing the economic impacts of overlapping compliance dates. See, e.g., Adopting Release, supra note 4, at 221-222. The Adopting Release does not include any analysis as to whether the substantive reporting requirements imposed by the Form PF amendments continue to be appropriate in light of the amendments to the definition of “dealer.”

[14] See, Adopting Release, supra note 4, at 220 – 221.

[15] Id. at 220. (Emphasis added.)

[16] Id. at 7. (Proclaiming that the Commission is “adopting the amendments [to Form PF] largely as proposed. . .” (Emphasis added.))

[17] Commissioner Mark T. Uyeda, Statement on Further Definition of “As a Part of a Regular Business” in the Definition of Dealer (Feb. 6, 2024), available at https://www.sec.gov/news/statement/uyeda-statement-dealer-trader-020624 (“Indeed, following Form PF, the adoption of private fund adviser rules, securities lending disclosure, and short position and short activity reporting, this action feels like another salvo in the Commission’s war on private funds.”).

TLDRS

- Senator Sherrod Brown to Secretary of the Treasury Janet Yellen: FSOC Must Be There to Protect Our Economy When Wall Street Tries to Duck Regulators.

- "FSOC makes Wall Street nervous—nervous that FSOC could bring oversight and accountability to parts of Wall Street that wouldn’t otherwise get it."

- "When Wall Street tries to shapeshift to evade the watchdogs we depend on, FSOC must be there to take action to protect our economy."

- Yesterday, the SEC adopted amendments to enhance private fund reporting including those also registered with the CFTC.

- The amendments to Form PF will enhance reporting by large hedge fund advisers on various aspects such as investment exposures, borrowing, counterparty exposure, risk metrics, and investment performance to improve insight into fund operations and strategies, and enhance data quality and comparability.

- Additional information will be required about advisers and the private funds they manage, including details on assets under management, withdrawal rights, gross and net asset values, inflows and outflows, and fund performance, aimed at providing a deeper understanding of private funds’ operations, assisting in trend identification, and reducing reporting errors.

- The changes will also demand more detailed reporting on investment strategies, counterparty exposures, and trading and clearing mechanisms, while eliminating redundant questions to offer a clearer view of hedge funds’ operations and strategies, help in trend analysis, and enhance data quality and comparability.

- Goes into affect 1 year after being published in the Federal Register.

- What others are saying:

- SEC Chair Gary Gensler: "I am pleased to support the adoption because it will improve the quality of the information we receive, particularly from large hedge fund advisers. This will help the SEC & FSOC to better assess systemic risk and protect investors."

- Commissioner Hester M. Peirce: "I write to dissent from the latest unwarranted expansion of Form PF. These revisions stem from the Commission’s unbridled curiosity rather than from a legitimate regulatory objective."

- Commissioner Mark T. Uyeda: "Apparently, every burden the Commission can possibly conjure is necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk by FSOC."