SEC Commissioner Mark T. Uyeda from his statement on Form N-PORT and From N-CEN reporting: "I reject the premise that frequent public disclosure of consistent information made available for all funds is a “public good.”"

Just as SEC Commissioner Hester Peirce, SEC Commissioner Mark Uyeda dissents against the SEC's Form N-PORT and Form N-CEN reporting amendments.

Uyeda has criticized the SEC’s decision to increase the frequency of public disclosure of fund portfolio data, arguing that the move could harm fund investors and undermine active management strategies. Uyeda expressed concern that requiring monthly public disclosure of Form N-PORT data would expose fund managers’ investment strategies to predatory trading and copying, potentially leading to decreased performance and higher trading costs. He emphasized that these changes disproportionately affect smaller asset managers, many of whom follow active management strategies, and could further tilt the market in favor of passive investing.

Uyeda argued that the Commission failed to justify the need for more frequent public disclosure and did not adequately consider the potential negative impacts on investors, particularly those in actively managed funds. He also questioned the assumption that more public data benefits retail investors, pointing out that many investors are not interested in detailed portfolio holdings and that the increased disclosure could lead to unintended consequences, such as fund liquidations.

Moreover, Uyeda criticized the Commission for prioritizing regulatory transparency over protecting the intellectual property of fund managers, stating that the new rules could discourage the fundamental research that contributes to price discovery in the markets. He warned that the new regulations might stifle the diversity of investment strategies and reduce investor choice, ultimately harming the very markets they are intended to protect.

"just because some funds have decided that the benefits of public disclosure outweigh the harm does not mean that we should mandate more frequent disclosure for all funds."

Uyeda in his own words:

I reject the premise that frequent public disclosure of consistent information made available for all funds is a “public good.” The capital markets function efficiently because there are financial incentives to conduct value-adding fundamental research for securities and their prices, which is one reason for the very existence of fund investment managers.

Today’s amendments would require this information to be reported to the Commission within 30 days after the end of each calendar month, providing faster regulatory transparency into fund holdings and information based on timing that is not dependent on a fund’s fiscal quarter.

Why does the difference between regulatory transparency and public transparency matter? Why does the difference between twelve public data points versus four public data points matter? It is because fund portfolios represent the intellectual work product of investment advisers. Thus, the idea that fund advisers need to provide their investment ideas to the general public for free is highly concerning. If fund investment advisers are not compensated for their skill in conducting fundamental investment research and effective trading strategies, then such efforts will be less likely to occur at all – and the public good of price discovery will be significantly harmed.

Similarly, some funds may have a focused portfolio consisting of a handful of companies, in which each investment decision is highly impactful. As such, public disclosure of Form N-PORT data raises the risk of predatory trading, where the manager’s careful investment decisions can be easily and cheaply copied.

The Commission’s decision to minimize these concerns is puzzling. Form N-PORT, as the Commission has repeatedly observed, is primarily designed to assist the Commission and its staff.[8] It is not retail investor friendly. Instead, the Commission believes that individual investors will benefit from third-party service providers that aggregate and analyze the data for a fee, as well as the efforts of academics.

just because some funds have decided that the benefits of public disclosure outweigh the harm does not mean that we should mandate more frequent disclosure for all funds.

The results are the intellectual work product of the fund manager and its skill; that information is not a public good to which everyone may have access for free, while the active management itself is a public good given that it contributes to price discovery. Thus, with this rulemaking we run the danger of undermining the public good at issue here.

So, what is Uyeda so big mad about?:

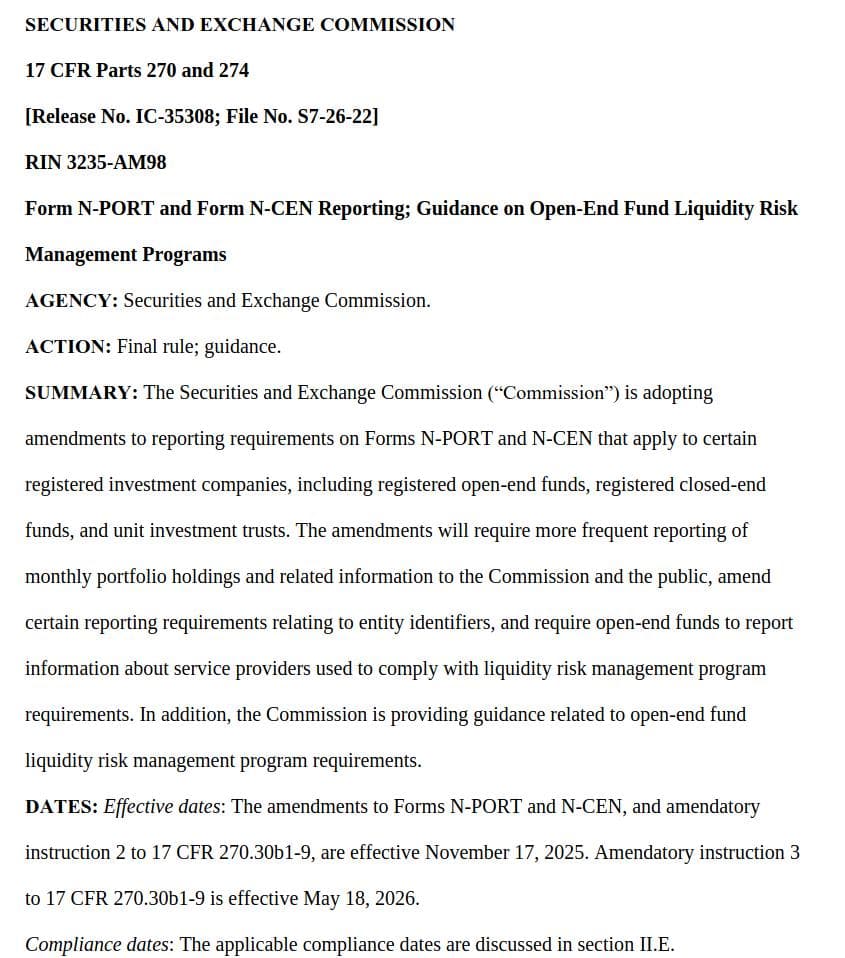

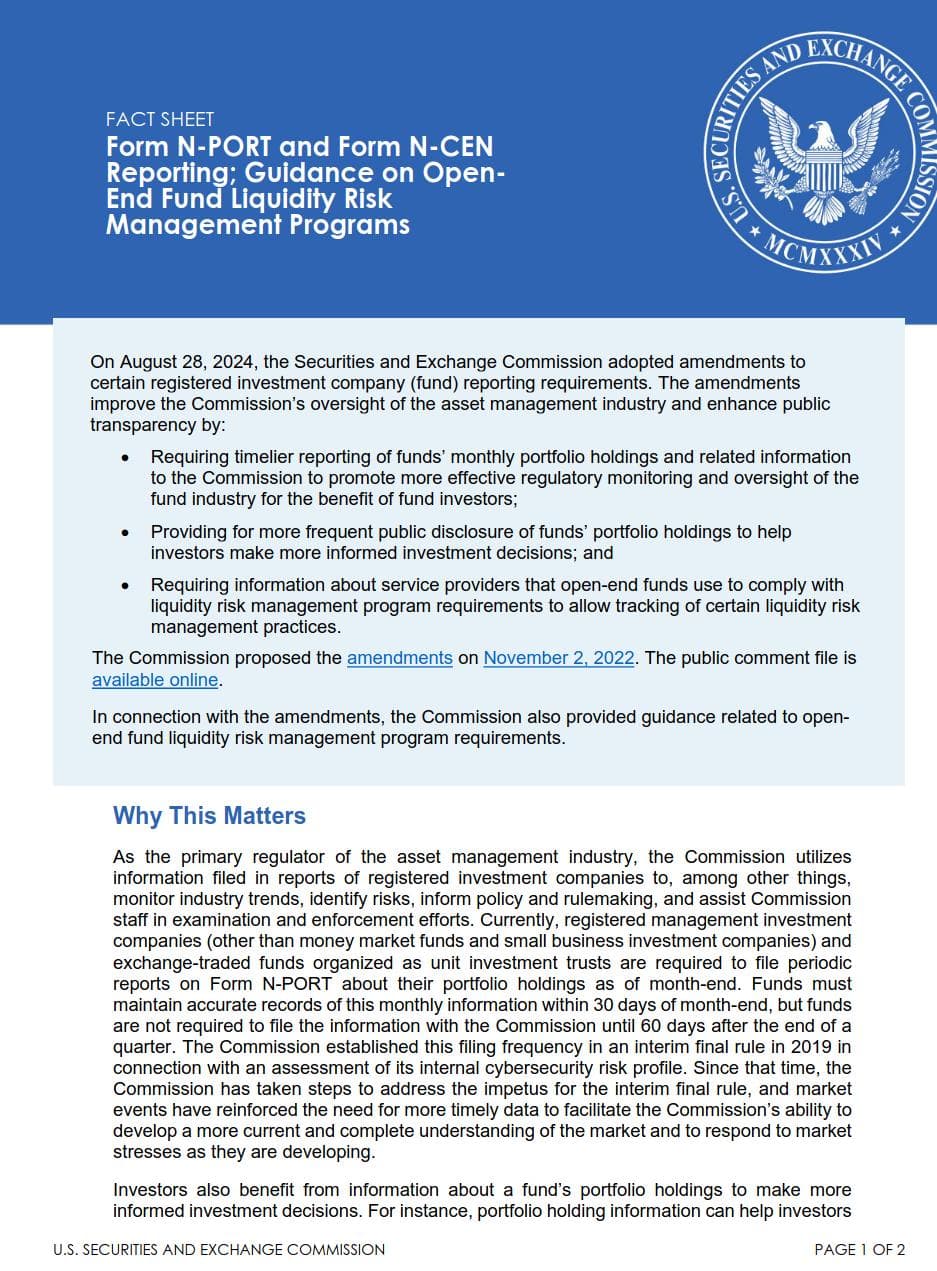

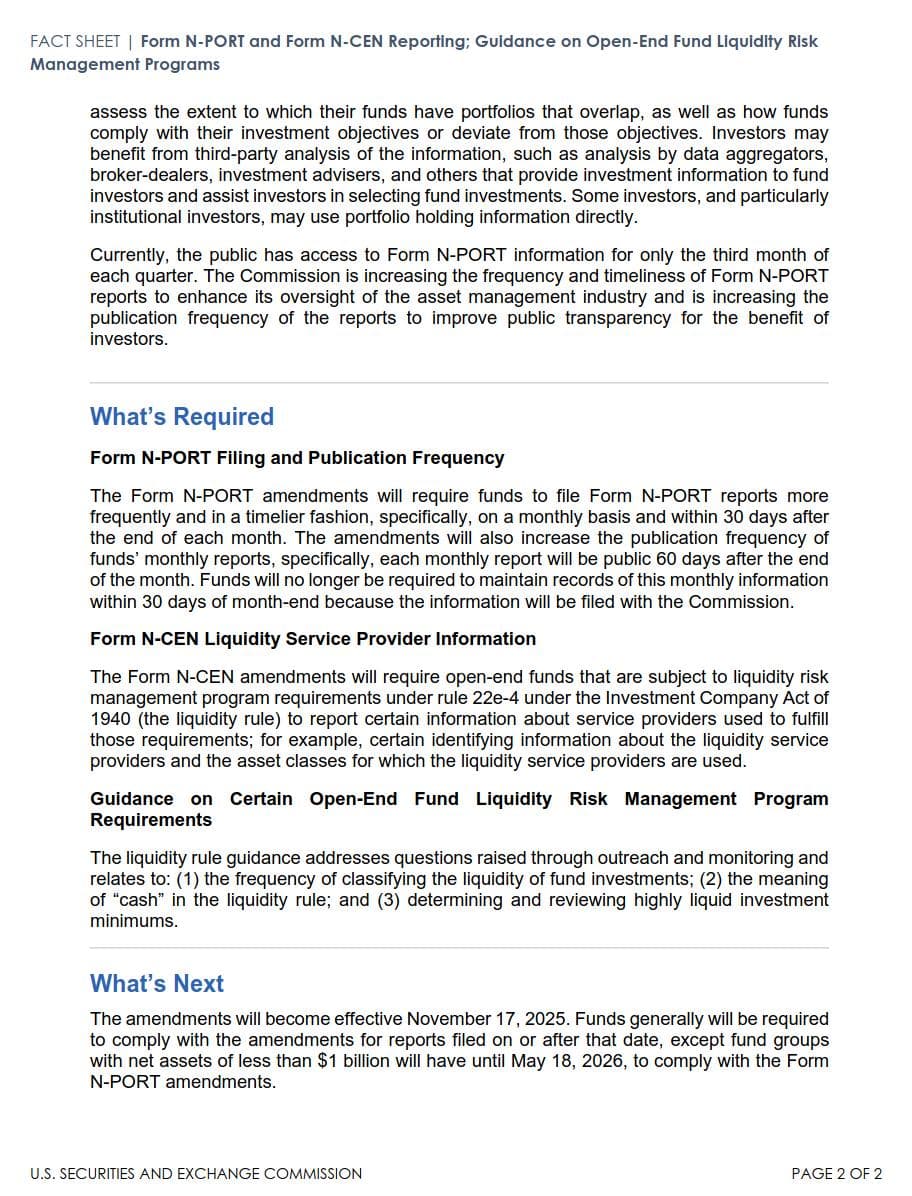

The SEC has approved amendments to the reporting requirements for investment funds, aiming to provide both the Commission and investors with more timely and detailed information. Under the new rules, funds will be required to file monthly reports on Form N-PORT, instead of the current quarterly filings, giving the SEC and investors quicker access to data on funds' portfolio holdings and associated risks.

These changes, effective from November 17, 2025, will triple the amount of portfolio data available to investors each year, enhancing their ability to monitor and assess the performance and risk profiles of their investments. The reports will be made public 60 days after the end of each month, increasing transparency across the fund industry.

The SEC also introduced amendments to Form N-CEN, which will require funds to report on service providers involved in liquidity risk management, and offered new guidance to address common questions in this area. Smaller fund groups with net assets under $1 billion will have an extended deadline until May 2026 to comply with the new Form N-PORT requirements.

TLDRS:

- SEC Commissioner Mark Uyeda dissents against the SEC's amendments to Form N-PORT and Form N-CEN reporting.

- Uyeda criticized the increase in public disclosure frequency, arguing it could harm fund investors and undermine active management strategies.

- "I reject the premise that frequent public disclosure of consistent information made available for all funds is a “public good.”"

- "just because some funds have decided that the benefits of public disclosure outweigh the harm does not mean that we should mandate more frequent disclosure for all funds."

- "Similarly, some funds may have a focused portfolio consisting of a handful of companies, in which each investment decision is highly impactful. As such, public disclosure of Form N-PORT data raises the risk of predatory trading, where the manager’s careful investment decisions can be easily and cheaply copied."

- He expressed concerns that monthly public disclosure of Form N-PORT data could lead to predatory trading, copying of fund strategies, decreased performance, and higher trading costs.

- Uyeda emphasized that these changes disproportionately affect smaller asset managers, potentially favoring passive investing over active strategies.

- He argued that the SEC failed to justify the need for more frequent public disclosure and did not consider the potential negative impacts, such as fund liquidations.

- Uyeda warned that the new rules might discourage fundamental research, stifle investment strategy diversity, and reduce investor choice, ultimately harming the markets.

What Uyeda is upset about:

- The SEC adopted amendments to increase the frequency of fund reporting from quarterly to monthly, effective November 17, 2025.

- The new rules will triple the amount of portfolio data available to investors, enhancing transparency and enabling better monitoring of fund performance and risks.

- Monthly reports will be made public 60 days after the end of each month.

- The SEC also amended Form N-CEN to require reporting on liquidity risk management service providers and issued new guidance on liquidity risk management.

- Smaller funds with net assets under $1 billion have an extended compliance deadline until May 2026.

SEC Commissioner Mark T. Uyeda from his statement against Form N-PORT and From N-CEN reporting:

— dismal-jellyfish (@DismalJellyfish) August 30, 2024

"I reject the premise that frequent public disclosure of consistent information made available for all funds is a “public good.”"https://t.co/hNxeWFOFLF