Caroline Crenshaw: "While routing to that exchange would result in an economic benefit for the member in the form of reduced fees or increased rebates, it may be costly to the customer if it comes at the expense of execution quality."

Statement:

A long line of economic literature asserts that competition among firms benefits consumers.[1] Competitive markets promote economic efficiency and growth, and their benefits can include lower prices and better products for consumers, as well as a more level playing field for small businesses that seek to enter new markets or expand their market share.[2]

In the realm of securities laws, in addition to investor protection, the Exchange Act requires the Commission to consider the effect that a proposed rule would have on competition.[3] Today we are considering a proposal that is designed to address a variety of concerns related to volume-based exchange transaction pricing (“tiered pricing”), including the competitive inequities associated with this type of pricing.

First, we are concerned about the impact of tiered pricing on competition between exchange members, such as when broker-dealers are competing for customers.[4] With tiered pricing, rebates go up and fees go down as a broker-dealer’s transaction volume increases on a given exchange, so that the more volume a broker-dealer transacts on that exchange, the better prices they get. This puts high-volume broker-dealers in a better position to offer lower commissions or fees, which may help them attract more order flow from customers—which in turn allows them to continue consolidating order flow to reach even more favorable pricing tiers as part of a self-reinforcing cycle.

While this cycle amplifies the competitive advantage for high-volume broker-dealers, it can disadvantage lower-volume broker-dealers, which tend to be smaller firms, since they cannot compete with larger firms for the order flow needed to get the best pricing. In fact, this cycle may be further magnified to the extent that smaller firms become customers of their high-volume competitors in an effort to qualify for better exchange pricing by routing some or all of their orders through their competitor. As others have suggested, existing rebate tier structure may play a role in picking winners and losers in today’s equity markets, limiting the competitive opportunities for firms that are unable to achieve the trading volumes needed to qualify for higher rebate payouts.[5]

Second, the Commission is concerned about certain exchanges using tiered pricing to preserve or extend their market power at the expense of inter-exchange competition.[6] For example, some primary listing exchanges base closing auction pricing on the volume a member executes during regular trading hours, in a practice known as “auction-linked pricing.”[7] This practice may incentivize members to route more orders to the listing exchange during regular hours to qualify for tiered pricing in the closing auction. This dynamic may harm the ability of non-listing exchanges to compete for order flow during the regular trading session outside of the auction.

Third, in addition to our concerns regarding competition, tiered pricing may present a conflict of interest between exchange members and their customers when routing orders.[8] Specifically, when a member executes an agency order, it faces an economic incentive to route the order to one particular exchange over others to achieve volume tier requirements on that exchange. While routing to that exchange would result in an economic benefit for the member in the form of reduced fees or increased rebates, it may be costly to the customer if it comes at the expense of execution quality.

Today’s proposal provides one possible avenue to address these concerns—a partial ban on tiered pricing, which would prohibit equity exchanges from offering tiered pricing in connection with the execution of agency-related volume in certain stocks, while also requiring transparency for tiered pricing related to member proprietary volume, among other things.[9] However, there are other ways to address these concerns as well, such as by adopting a full ban that would prohibit exchanges from offering tiered pricing for all volume in certain stocks, including both proprietary and agency-related order flow, as discussed in the Economic Analysis of this proposal.[10] Given these considerations and the proliferation of tiered transaction pricing schedules across many exchanges, I look forward to hearing feedback from commenters regarding the issues presented by this complex system of transaction-based fees.

For example, even though there are no third-party customers involved in tiered pricing for principal orders, volume-based pricing tiers still provide exchange members that engage in a high amount of principal trading with a competitive advantage in attracting customer order flow. Given this consideration, would a prohibition on tiered pricing that is limited to the execution of agency-related volume adequately address the concerns we have identified about member competition? Or, would a full prohibition on tiered pricing for all volume in certain stocks be more appropriate? Are there any practical concerns we should consider related to distinguishing between principal and agency order flow? Are there other ways tiered pricing may be hindering competition that we should be thinking about? I look forward to reviewing comments on these issues and others on which the proposing release solicits feedback.

Finally, I would like to thank staff in the Divisions of Trading and Markets, Economic and Risk Analysis, and the Office of General Counsel. I am deeply appreciative of your hard work on this proposal, and I am pleased to support it.

[1] See Obama White House Archives, Council of Economic Advisers Issue Brief (April 2016) at 1 available at https://obamawhitehouse.archives.gov/sites/default/files/page/files/20160414_cea_competition_issue_brief.pdf.

[2] See id. at 14.

[3] See 15 U.S.C. 78c(f) and 78w(a)(2).

[4] See Volume-Based Exchange Transaction Pricing for NMS Stocks, Rel. No.34-98766 (Oct. 18, 2023) (“Proposing Release”) at 13.

[5] See Letter from John Ramsay, Chief Market Policy Officer, Investors Exchange LLC to Vanessa Countryman, Secretary, Commission (Sept. 20, 2023) (“IEX Letter”) (comment letter on File No. S7-30-22) available at https://www.sec.gov/comments/s7-30-22/s73022-262059-619382.pdf.

[6] See Proposing Release at 22.

[7] See id. at 22, 151.

[8] See id. at 20.

[9] See id. at 5.

[10] See id. at 153. Under a full ban on tiered pricing, a requirement for disclosures regarding the number of exchange members qualifying for volume-based tiers would not be necessary, as there would be no volume-based tiers left. See id. at 156.

What Caroline is happy to support:

Background:

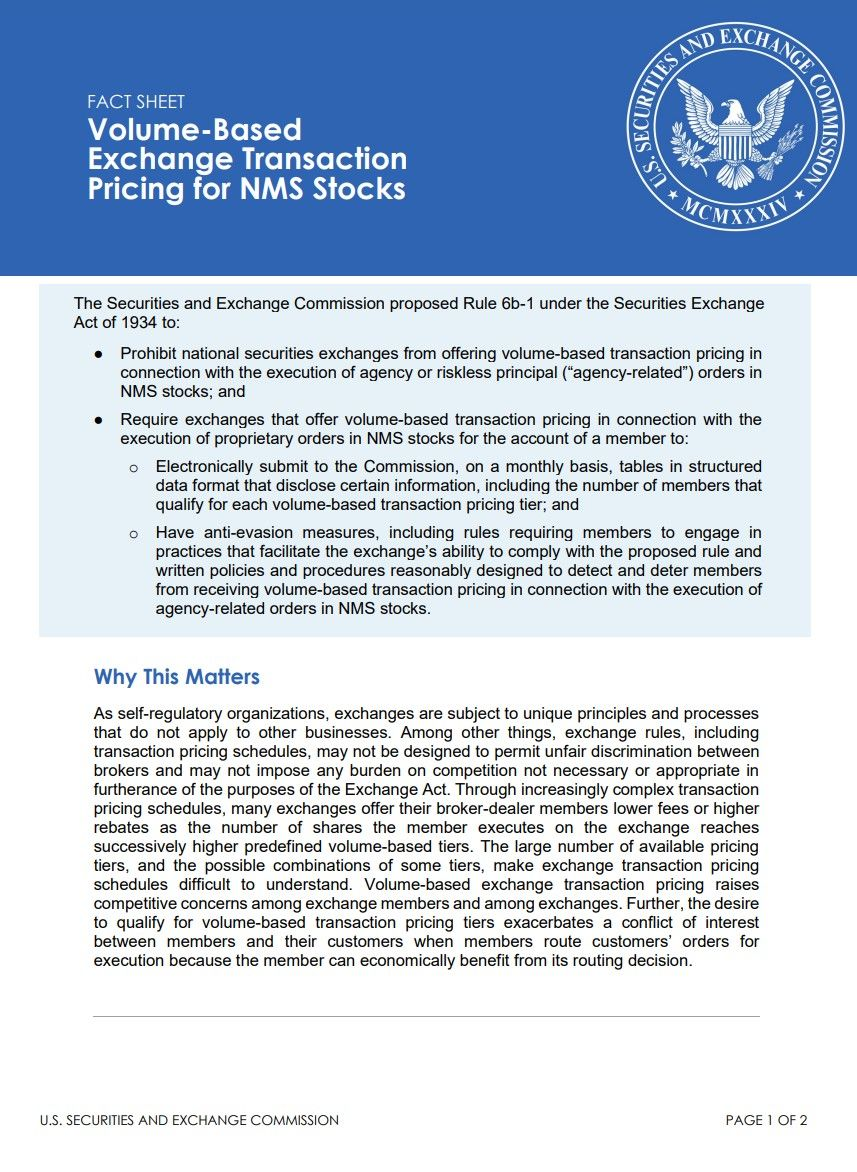

National securities exchanges (“exchanges”) that trade NMS stocks maintain pricing schedules that set forth the transaction pricing they apply to their broker-dealer members that execute orders on their trading platforms. As self-regulatory organizations under the Exchange Act, exchanges are subject to unique principles and processes that do not apply to other businesses. For example, all proposed rules of an exchange, including exchange transaction pricing proposals, must be filed with the Commission. In addition, pricing schedules must be publicly posted on the exchange’s website.

The Exchange Act further requires that exchange pricing proposals, among other things, provide for the “equitable allocation of reasonable dues, fees, and other charges among its members and issuers and other persons using its facilities” that “are not designed to permit unfair discrimination between customers, issuers, brokers, or dealers” and “do not impose any burden on competition not necessary or appropriate in furtherance of the purposes of” the Exchange Act. With respect to the requirement that the rules of an exchange not impose any burden on competition not necessary or appropriate in furtherance of the purposes of the Exchange Act, the Senate Banking, Housing and Urban Affairs Committee report that accompanied the 1975 amendments to the Exchange Act stated that “this paragraph is designed to make clear that a balance must be struck between regulatory objectives and competition, and that unless an interference with competition is justified in terms of the achievement of a statutory objective, it cannot stand.”

Section 11A of the Exchange Act directs the Commission to facilitate the establishment of a national market system in accordance with specified Congressional findings. Among the Congressional findings are assuring (i) fair competition among brokers and dealers and among exchange markets, and (ii) the practicability of brokers executing investors’ orders in the best market. Rather than setting forth minimum components of the national market system, the Exchange Act grants the Commission broad authority to oversee the implementation, operation, and regulation of the national market system consistent with Congressionally determined goals and objectives.

Fact Sheet:

Press Release:

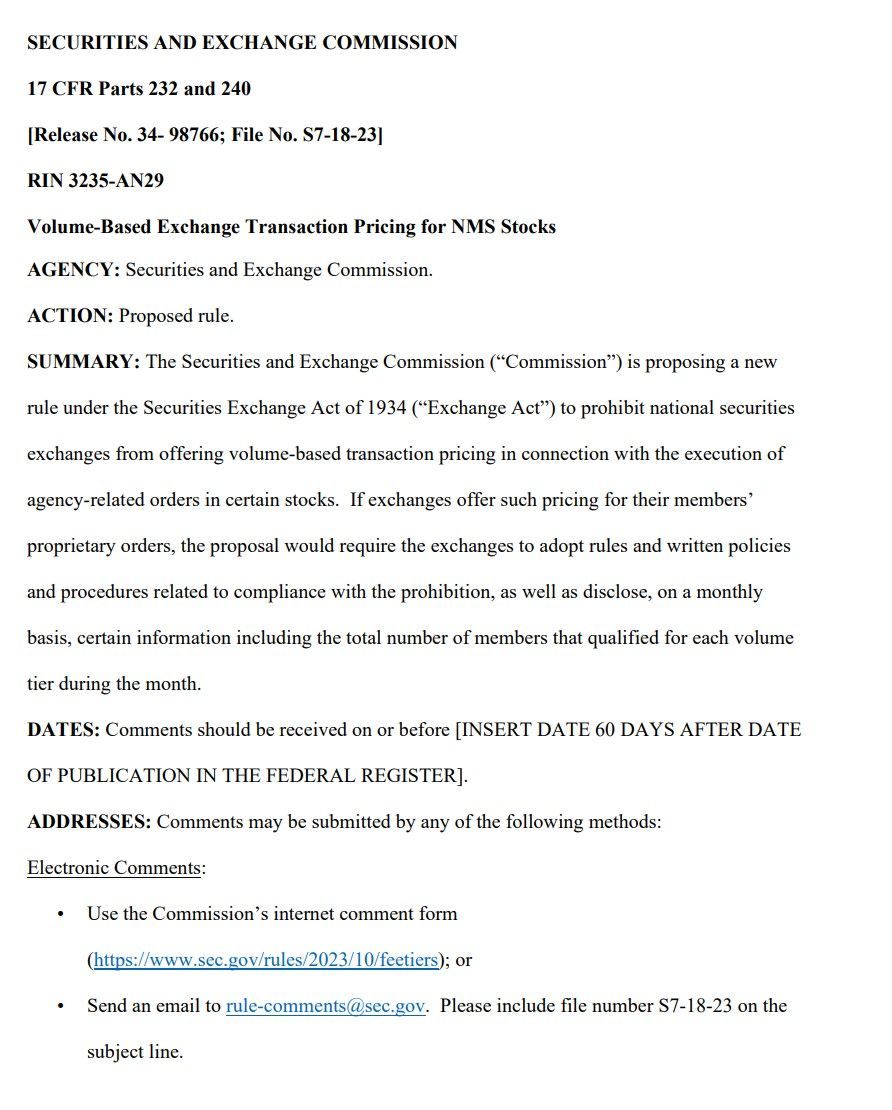

The Securities and Exchange Commission today proposed a new rule that would prohibit national securities exchanges from offering volume-based transaction pricing in connection with the execution of agency or riskless principal (“agency-related”) orders in NMS stocks. The proposal also would require national securities exchanges to have certain anti-evasion rules and written policies and procedures and disclose certain information if they offer volume-based transaction pricing for member proprietary volume in NMS stocks.

“Currently, the playing field upon which broker-dealers compete is unlevel,” said SEC Chair Gary Gensler. “Through volume-based transaction pricing, mid-sized and smaller broker-dealers effectively pay higher fees than larger brokers to trade on most exchanges. We have heard from a number of market participants that volume-based transaction pricing along with related market practices raise concerns about competition in the markets. I am pleased to support this proposal because it will elicit important public feedback on how the Commission can best promote competition amongst equity market participants.”

Proposed Rule 6b-1 under the Securities Exchange Act of 1934 would prohibit national securities exchanges from offering volume-based transaction pricing in connection with the execution of agency-related orders in NMS stocks. It also would require exchanges that offer volume-based transaction pricing in connection with the execution of members’ proprietary orders in NMS stocks to disclose certain information, including the number of members that qualify for each transaction pricing tier that the exchange offers. Exchanges would be required to submit this information to the Commission on a monthly basis, and the public would be able to access the information through the Commission’s EDGAR system.

In addition, proposed Rule 6b-1 would require exchanges that have volume-based transaction pricing for member proprietary orders in NMS stocks to have anti-evasion measures, including rules requiring members to engage in practices that facilitate the exchange’s ability to comply with the prohibition on volume-based exchange transaction pricing for agency-related orders in NMS stocks and to have written policies and procedures reasonably designed to detect and deter members from receiving volume-based pricing in connection with the execution of agency-related orders in NMS stocks.

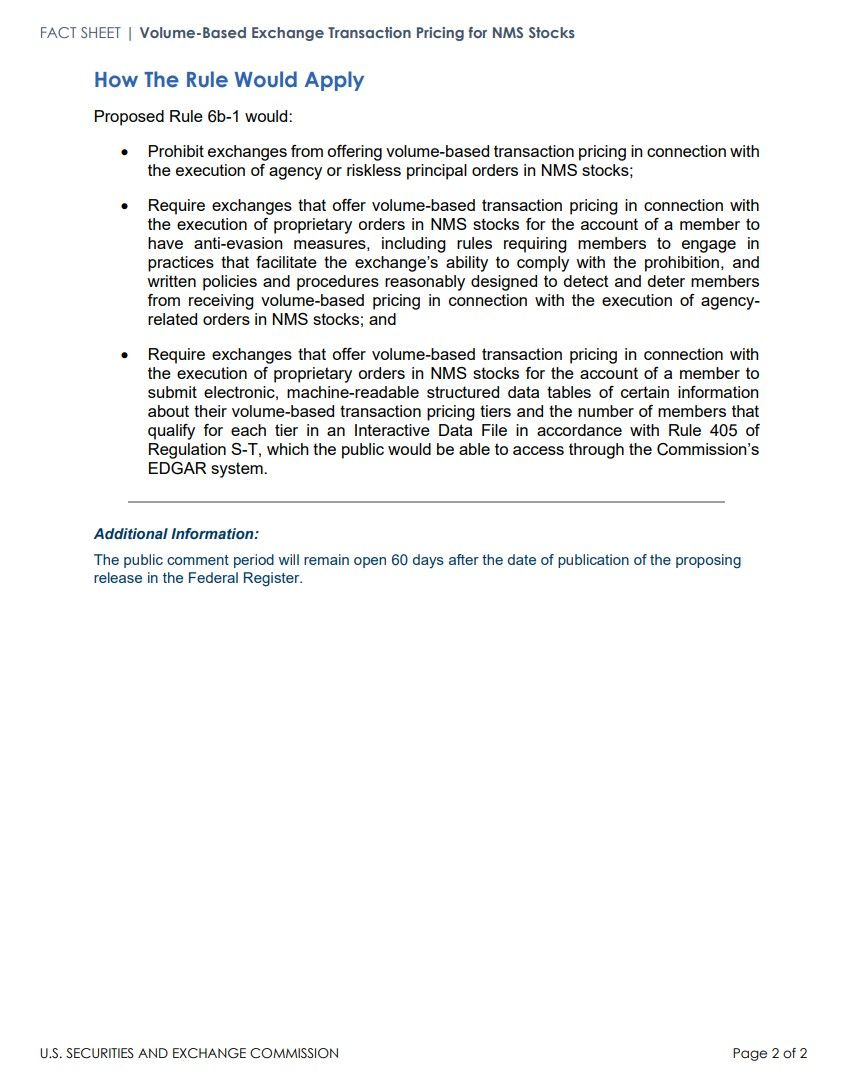

The proposing release will be published in the Federal Register. The public comment period will remain open until 60 days after the date of publication of the proposing release in the Federal Register.

How to comment:

Electronic Comments:

- Use the Commission’s online form at: https://www.sec.gov/rules/2023/10/feetiers

- Alternatively, send an email to [email protected]. Ensure the subject line includes the file number S7-18-23.

Paper Comments:

- Mail your paper comments to: Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

Important Notes:

- Always refer to the file number S7-18-23 in your submission.

- If using email, include the file number in the subject line.

- For efficiency, only use one method of submission.

- All comments will be posted on the Commission’s website at: https://www.sec.gov/rules/proposed.shtml

- Refrain from including personal details in your comments. Only provide information you're comfortable being public.

- Obscene or copyrighted material may be redacted or not published.

TLDRS:

- SEC Proposes Rule to Address Volume-Based Exchange Transaction Pricing for NMS Stocks.

SEC Commissioner Caroline Crenshaw:

- "I am pleased to support it."

- "While routing to that exchange would result in an economic benefit for the member in the form of reduced fees or increased rebates, it may be costly to the customer if it comes at the expense of execution quality."

- "While this cycle amplifies the competitive advantage for high-volume broker-dealers, it can disadvantage lower-volume broker-dealers, which tend to be smaller firms, since they cannot compete with larger firms for the order flow needed to get the best pricing. In fact, this cycle may be further magnified to the extent that smaller firms become customers of their high-volume competitors in an effort to qualify for better exchange pricing by routing some or all of their orders through their competitor."

- "tiered pricing may present a conflict of interest between exchange members and their customers when routing orders. Specifically, when a member executes an agency order, it faces an economic incentive to route the order to one particular exchange over others to achieve volume tier requirements on that exchange. While routing to that exchange would result in an economic benefit for the member in the form of reduced fees or increased rebates, it may be costly to the customer if it comes at the expense of execution quality."

- "I look forward to hearing feedback from commenters regarding the issues presented by this complex system of transaction-based fees."

- "Given this consideration, would a prohibition on tiered pricing that is limited to the execution of agency-related volume adequately address the concerns we have identified about member competition? Or, would a full prohibition on tiered pricing for all volume in certain stocks be more appropriate? Are there any practical concerns we should consider related to distinguishing between principal and agency order flow? Are there other ways tiered pricing may be hindering competition that we should be thinking about? I look forward to reviewing comments on these issues and others on which the proposing release solicits feedback."

Proposed Rule 6b-1 would:

- Prohibit exchanges from offering volume-based transaction pricing in connection with the execution of agency or riskless principal orders in NMS stocks.

- Require exchanges that offer volume-based transaction pricing in connection with the execution of proprietary orders in NMS stocks for the account of a member to have anti-evasion measures, including rules requiring members to engage in practices that facilitate the exchange’s ability to comply with the prohibition, and written policies and procedures reasonably designed to detect and deter members from receiving volume-based pricing in connection with the execution of agency related orders in NMS stocks.

- Require exchanges that offer volume-based transaction pricing in connection with the execution of proprietary orders in NMS stocks for the account of a member to submit electronic, machine-readable structured data tables of certain information about their volume-based transaction pricing tiers and the number of members that qualify for each tier in an Interactive Data File in accordance with Rule 405 of Regulation S-T, which the public would be able to access through the Commission’s EDGAR system.

- OPEN FOR COMMENT!