Commissioner Hester M. Peirce on SEC's new beneficial ownership rule: "Although better than the proposed rule, the final beneficial ownership reporting rule continues to rest on flawed economics. Accordingly, I cannot support it."

Although better than the proposed rule,[1] the final beneficial ownership reporting rule continues to rest on flawed economics. Accordingly, I cannot support it.

The heart of the final rule is a shortening of the filing windows for Schedules 13D and G, which report an investor’s holding of large positions in a company’s shares. Although the original filing timelines are not necessarily the Platonic ideal, a decision to shorten the timeframes should be well justified. Here, a justification is lacking.

According to the Commission, shortening the 13D window will mitigate information asymmetries between everyday investors, on the one hand, and 13D filers and “informed bystanders,” on the other hand. By the Commission’s logic, narrowing the filing window should enable uninformed traders to share in profits created by the diligent efforts of more informed investors. But, absent a compelling reason, people who lawfully possess information should not have to hand that information over to their uninformed counterparties.

The Commission’s position ignores that disparities in information and perspective are central to the functioning of our markets.[2] Different people come to the market with different views of what a particular asset is worth and different levels of interest in buying or selling it. One person may desperately want to buy something that someone else is equally eager to sell. Hence, a market is made. The buyers and sellers generally do not have to explain their motivations. The prices speak for themselves.[3]

Of particular concern are rules that prevent someone who has worked hard to identify a mismanaged company and develop a strategy for improving it from getting adequately compensated for that work and the associated risk.[4] Indeed, the Commission acknowledges that “the initial information asymmetry between a prospective filer and the market is not a market failure because in its absence, the filer may not be sufficiently rewarded for the expenses of its efforts expended in information acquisition and in pursuing changes at the issuer, which often have market-level benefits.”[5] As one commenter explained, “permitting buyers to make a profit from their asymmetric information is often needed to induce them to invest effort to discover firms that are mismanaged.”[6]

Recognizing “that benefits may stem from the information asymmetry between a Schedule 13D filer and the market” and “that the information advantage of Schedule 13D filers results, in general, from their own expenditures . . . or efforts,” the adopting release emphasizes the informational advantages of so-called “informed bystanders.”[7] These informed bystanders are opportunistic traders who, observing the market, suspect that something is afoot or have become aware of the filer’s plans. The Commission worries that their consequent “informational advantage . . . over the selling shareholders in these transactions and the associated wealth transfers may be perceived by some market participants to be unfair.”[8] But it is unclear that we should give any weight to this concern. The release provides little evidence that informed bystanders are a large population.[9] Even if they were, they arguably contribute to price formation and market functioning.[10]

Economic principles have not changed since 1968, when the Williams Act, which forms the basis for the Section 13D mandate, became law.[11] The Commission points out that technology has changed and that those technological changes may enable investors to file their Schedules 13D faster[12] and accumulate “a large equity stake more quickly.”[13] However, as the Commission acknowledges, other technological[14] and legal[15] developments could increase costs for activists. Today, as a half-century ago when the Williams Act passed, the basic principle remains that people will not go to the trouble of identifying ways in which companies can improve unless they are rewarded for that work. And if investors pare back their monitoring of companies, other investors and the broader economy could suffer. The Commission’s economic analysis takes great pains to show that the changes will not impair activist investors that much, but in the process demonstrates that the rule will have substantial effects on how these investors proceed.[16] The result could be fewer potentially corporate value-enhancing campaigns.[17] This “modernization” effort might better be characterized as an insulation effort—insulating corporate managers from scrutiny.[18] Each campaign must be judged on its own merits, of course, and other reforms could be useful in ensuring that public company managers can respond to activists and present their side of the story to shareholders.

My concerns extend also to the 13G changes, which would shorten filing timelines for large investors with no control intent.[19] Shortening filing deadlines for investors who generally have no plans to effect a change in control lacks any economic rationale. Under the amendments, 13G filers will have to give up their intellectual property earlier than they do now and thus subject themselves to copycatting and frontrunning.[20] This cost to one group of investors is not outweighed by a corresponding benefit to other investors. As commenters noted, 13G information is not of immediate interest to market participants who are not trying to front run.[21]Amendments to reflect changes in the amount of holdings by 13G filers are particularly uninteresting.[22] Moreover, the costs of speedier filings for these investors, some of whom are small and not financial firms, are likely to be high.[23] Meeting the final rule’s timelines for filing amended 13Gs, although more reasonable than what was proposed, will nevertheless be costly and difficult.[24] The Commission pointed to a rationale for shortening the 13G initial filing window for passive investors: some investors improperly hide their control intent by filing a 13G instead of a 13D.[25] If this problem is real, why not address the errant filers’ violations directly by enforcing existing regulations governing 13G eligibility? Rather than dragging 13G filers along for the ride in a release that is focused on 13D filers, the Commission should have, as one commenter recommended, set aside this issue for study.[26]

Much of commenters’ attention was focused on aspects of the rule other than filing timetables; the proposal also included guidance about cash-settled derivatives and the definition of group. The adopting release also addresses these topics, albeit more practically than did the proposing release.The adopting release, however, continues to raise questions. For example, how clear is the analytical framework with respect to cash-settled derivative securities that the Release imports from the 2011 security-based swaps release? Does the group guidance inappropriately downplay the importance of an “agreement” in group formation?[27] Is the group guidance unnecessarily accommodating to activists whose objectives are not to increase the value of the company at issue, but to further a cause that is either neutral or detrimental to the value of the company?[28] It would have been easier to answer these questions had the Commission put this guidance out for proposal.

While I cannot support this rule, I am thankful to the Commission staff for their excellent and diligent work on this rulemaking. I particularly appreciated a number of lively, thought-provoking conversations about the rule. Among others, I want to thank Corey Klemmer in the Chair’s office, Valian Ashfar, Ted Yu, and Nick Panos in the Division of Corporation Finance, the Division of Economic and Risk Analysis, the Office of General Counsel, and others throughout the Commission.

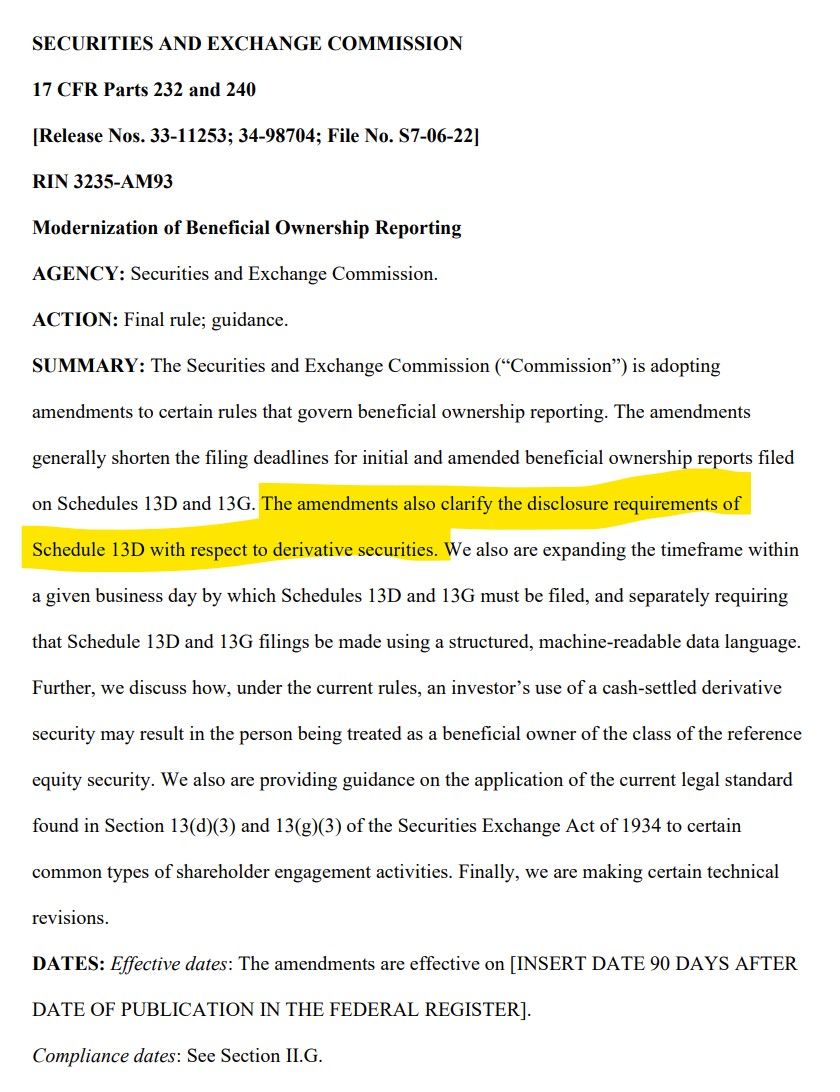

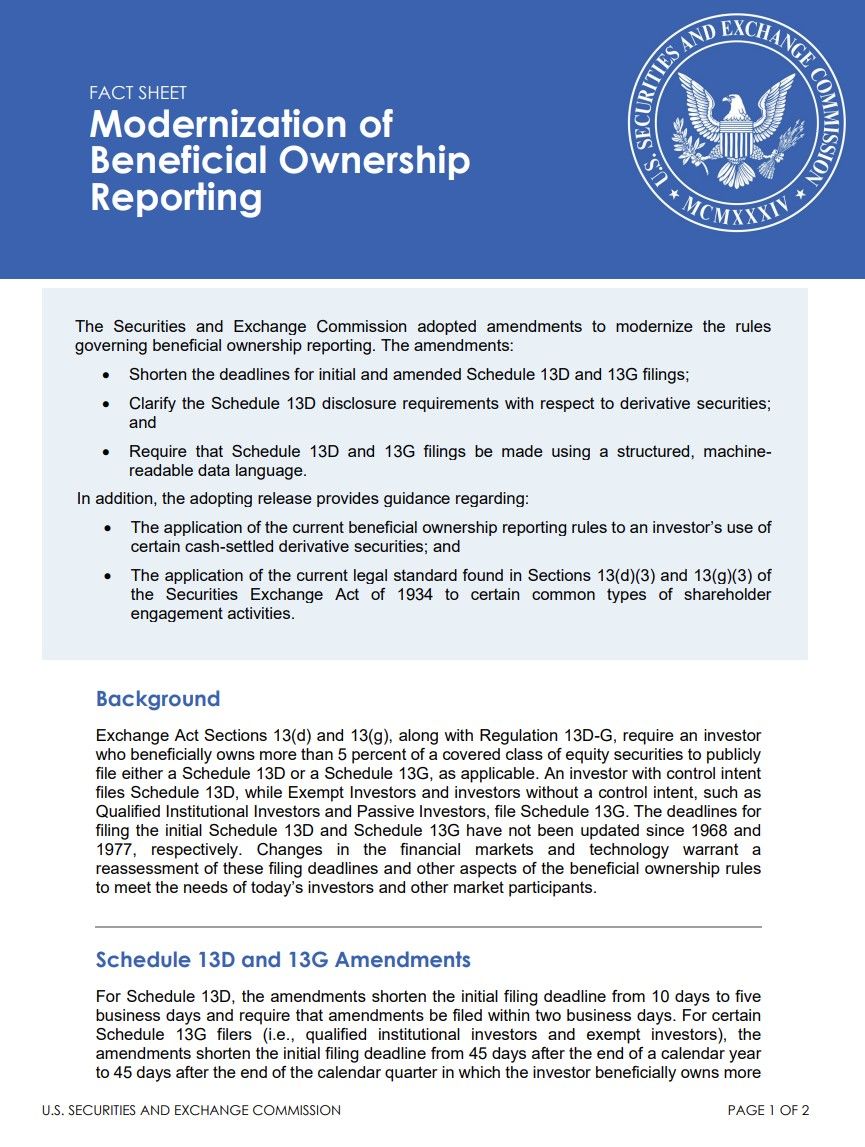

The Securities and Exchange Commission today adopted rule amendments governing beneficial ownership reporting under Sections 13(d) and 13(g) of the Securities Exchange Act of 1934. The amendments update Regulation 13D-G to require market participants to provide more timely information on their positions to meet the needs of investors in today’s financial markets.

“Today’s adoption updates rules that first went into effect more than 50 years ago. Frankly, these deadlines from half a century ago feel antiquated,” said SEC Chair Gary Gensler. “In our fast-paced markets, it shouldn’t take 10 days for the public to learn about an attempt to change or influence control of a public company. I am pleased to support this adoption because it updates Schedules 13D and 13G reporting requirements for modern markets, ensures investors receive material information in a timely way, and reduces information asymmetries.”

Exchange Act Sections 13(d) and 13(g), along with Regulation 13D-G, require an investor who beneficially owns more than 5 percent of a covered class of equity securities to publicly file either a Schedule 13D or a Schedule 13G, as applicable. An investor with control intent files Schedule 13D, while Exempt Investors and investors without a control intent, such as Qualified Institutional Investors and Passive Investors, file Schedule 13G.

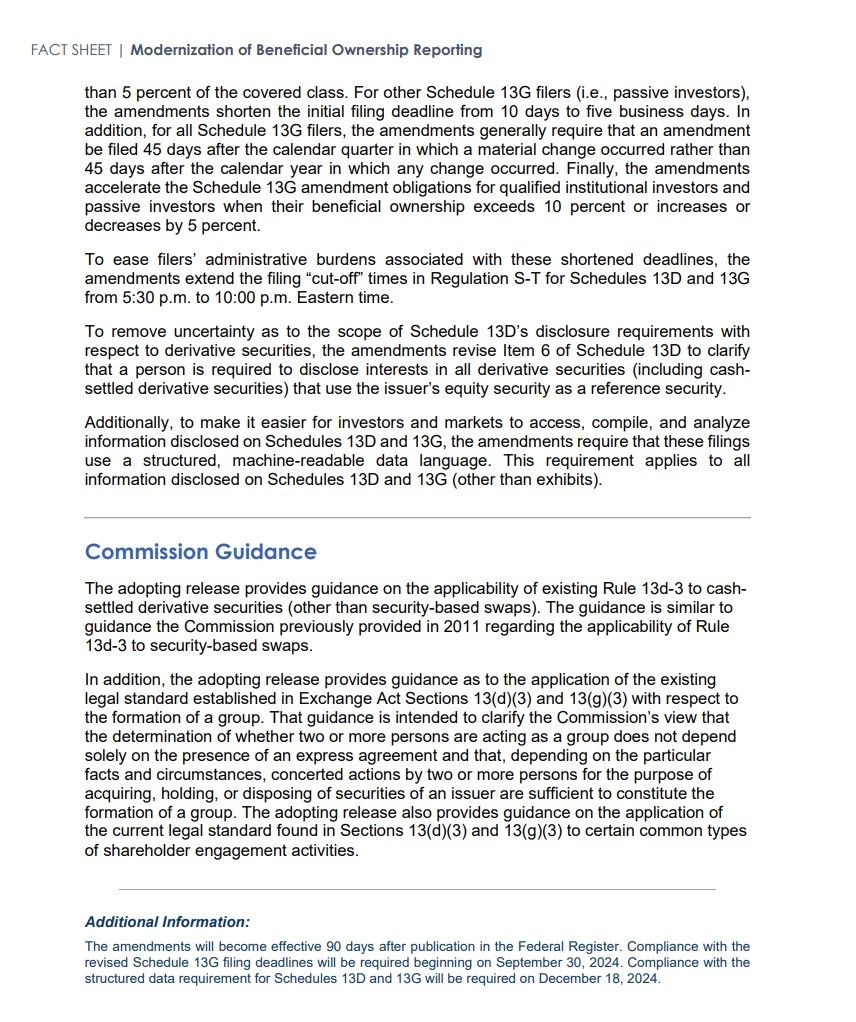

Among other things, today’s amendments: shorten the deadline for initial Schedule 13D filings from 10 days to five business days and require that Schedule 13D amendments be filed within two business days; generally accelerate the filing deadlines for Schedule 13G beneficial ownership reports (the filing deadlines differ based on the type of filer); clarify the Schedule 13D disclosure requirements with respect to derivative securities; and require that Schedule 13D and 13G filings be made using a structured, machine-readable data language.

Further, the adopting release provides guidance regarding the current legal standard governing when two or more persons may be considered a group for the purposes of determining whether the beneficial ownership threshold has been met, as well as how, under the current beneficial ownership reporting rules, an investor’s use of certain cash-settled derivative securities may result in the person being treated as a beneficial owner of the class of the reference equity securities.

The adopting release is published on SEC.gov and will be published in the Federal Register, and the amendments will become effective 90 days after publication in the Federal Register. Compliance with the revised Schedule 13G filing deadlines will be required beginning on Sept. 30, 2024. Compliance with the structured data requirement for Schedules 13D and 13G will be required on Dec. 18, 2024. Compliance with the other rule amendments will be required upon their effectiveness.

TLDRS:

SEC Adopts Amendments to Rules Governing Beneficial Ownership Reporting.

The amendments also clarify the disclosure requirements of Schedule 13D with respect to derivative securities.