NSCC proposes updating MLA charge by moving all exchange traded products (other than those deemed to be Illiquid Securities) into the equities asset group & calculating impact cost at the security level along with ETF tweaks.

Purpose:

Wut Mean?:

These proposed changes aim to make the calculation of the MLA charge more accurate, particularly in the context of liquidating exchange-traded products and equity ETFs.

Refinement of Calculation:

- The proposal includes refining how the MLA (Market Liquidity Adjustment) charge is calculated for liquidating securities or portfolios.

Changes to Exchange Traded Products (ETPs):

- All ETPs, except those classified as Illiquid Securities, will be moved into the equities asset group.

- The impact cost will now be calculated at the individual security level, instead of at the subgroup level for equity asset subgroups.

Improvements for Exchange Traded Funds (ETFs):

- The proposal includes new calculations for latent liquidity, specifically for equity ETFs that have in-kind baskets.

Results from the Impact Study:

- The impact study, using data from January 3, 2022, to June 30, 2023, showed that if these changes had been applied during this period:

- There would have been an approximate $62 million daily average increase in the MLA charge.

- This increase represents about 0.52% of the daily total Clearing Fund during that time.

- Currently, the daily MLA charge is around 3.54% of the daily total Clearing Fund.

- With the proposed changes, it would have been about 4.06% of the daily total Clearing Fund.

Overview of Required Fund Deposit and MLA Charge:

Wut Mean?:

This system is designed to protect the NSCC...

Credit Exposure Management:

- The NSCC manages its credit exposure to members by setting and monitoring Required Fund Deposits to the Clearing Fund, as outlined in its rules.

Purpose of Required Fund Deposit:

- Each member’s Required Fund Deposit acts as their margin.

- The primary goal of this deposit is to mitigate potential losses that the NSCC might incur in liquidating a member’s portfolio in case the member defaults.

Clearing Fund Composition:

- The total of all members' Required Fund Deposits constitutes the NSCC’s Clearing Fund.

Use of Clearing Fund in Defaults:

- In the event of a member’s default, the NSCC would first use the defaulting member’s own Required Fund Deposit to cover losses.

- If a defaulting member’s Required Fund Deposit is insufficient to cover the losses incurred from liquidating their portfolio, the NSCC would then access the Clearing Fund to cover the remaining losses.

Volatility Charge:

- The volatility charge is a key component of each member's Required Fund Deposit, as specified in Procedure XV of the NSCC Rules.

- It generally forms the largest part of the Required Fund Deposits.

Purpose of the Volatility Charge:

- The charge is designed to address the market price risk associated with each member’s portfolio.

- It aims to capture this risk at a 99th percentile level of confidence.

Methodologies for Calculation:

- NSCC uses two primary methodologies to calculate the volatility charge:

- Value at Risk (VaR) Model:

- For most Net Unsettled Positions, the volatility charge is calculated as the sum of:

- The greater of:

- A parametric VaR model calculation, or

- A portfolio margin floor calculation based on market values of long and short positions.

- Plus, a gap risk measure calculation, which focuses on the concentration threshold of the two largest non-diversified positions in a portfolio.

- The greater of:

- For most Net Unsettled Positions, the volatility charge is calculated as the sum of:

- Haircut-Based Method:

- Certain Net Unsettled Positions are excluded from the VaR Charge calculation.

- For these, a haircut-based volatility charge is applied, calculated by multiplying the absolute value of these positions by a set percentage.

- Value at Risk (VaR) Model:

MLA Charge:

- The MLA charge addresses situations where the market impact costs of liquidating a defaulted member's portfolio might exceed the volatility charge.

- It is designed to cover the market impact costs associated with large Net Unsettled Positions in specific asset groups or securities with a similar risk profile.

Why MLA Charge is Needed:

- Large Net Unsettled Positions in a particular asset group or type can be challenging to liquidate if a member defaults.

- A concentration in certain securities or asset types may reduce their marketability, increasing the market impact cost for NSCC during liquidation.

Risk Mitigation:

- The MLA charge aims to mitigate the risk of increased market impact costs associated with these concentrated positions.

Calculation of MLA Charge:

- It is calculated differently for various asset groups.

- The calculation compares the total market value of a Net Unsettled Position in an asset group against the available trading volume of that group in the market.

- The goal is to assess sufficient margin to offset the increased market impact cost risk.

How things are done currently:

Wut Mean?:

NSCC categorizes securities into separate asset groups with similar risk profiles:

- Equities (excluding those defined as Illiquid Securities).

- Illiquid Securities.

- Unit Investment Trusts (UITs).

- Municipal Bonds (including municipal bond ETPs).

- Corporate Bonds (including corporate bond ETPs).

Within the equities asset group, further segmentation is done into subgroups:

- Micro-capitalization equities.

- Small capitalization equities.

- Medium capitalization equities.

- Large capitalization equities.

- Treasury Exchange-Traded Products (ETPs).

- All other ETPs.

NSCC calculates the market impact cost for each asset group and equities asset subgroup where a Member has Net Unsettled Positions.

The MLA charge calculation is designed to estimate the potential additional market impact cost to NSCC of closing out large Net Unsettled Positions in specific asset groups or equities subgroups.

Market Impact Cost Calculation for Market Capitalization Subgroups of Equities Asset Group:

The market impact cost for Net Unsettled Positions in each market capitalization subgroup is calculated using four components:

- Impact Cost Coefficient:

- This is based on a multiple of the one-day market volatility of the subgroup.

- It is intended to measure the impact costs.

- Gross Market Value (Component 1):

- The gross market value of the Net Unsettled Position in that subgroup.

- Gross Market Value (Component 2):

- The square root of the gross market value of the Net Unsettled Position divided by an assumed percentage of the average daily trading volume of that subgroup.

- Concentration Measurement:

- A measurement of the concentration of the Net Unsettled Position within the subgroup in the portfolio.

Estimation at Portfolio Level:

- Rather than calculating the market impact cost for each individual security, NSCC estimates this cost at the portfolio level using aggregated volume data.

Measuring Concentration:

- The concentration of the Net Unsettled Position is assessed by aggregating the relative weight of each security in the Net Unsettled Position compared to its weight in the subgroup.

- Portfolios with fewer positions in a subgroup would have a higher measure of concentration for that subgroup

Market Impact Cost Calculation for Other Asset Groups and Equities Asset Subgroups:

This calculation method is used by NSCC to assess the potential market impact costs associated with liquidating large positions in various bond categories, Illiquid Securities, UITs, and ETPs.

- The calculation applies to Net Unsettled Positions in:

- Municipal bond asset group.

- Corporate bond asset group.

- Illiquid Securities asset group.

- Unit Investment Trusts (UITs) asset group.

- Treasury Exchange-Traded Products (ETP) subgroup.

- Other ETP subgroups within the equities asset group.

Components of Calculation:

The market impact cost is calculated by multiplying three components:

- Impact Cost Coefficient:

- This is based on a multiple of the one-day market volatility of the specific asset group or subgroup.

- Gross Market Value (Component 1):

- The gross market value of the Net Unsettled Position in the respective asset group or subgroup.

- Gross Market Value (Component 2):

- The square root of the gross market value of the Net Unsettled Position divided by an assumed percentage of the average daily trading volume of that asset group or subgroup.

Total MLA Charge Calculation for Each Portfolio:

Comparison with Volatility Charge:

- NSCC compares the calculated market impact cost for each asset group or subgroup to a portion of the volatility charge allocated to Net Unsettled Positions in that group or subgroup.

Threshold for Applying MLA Charge:

- If the ratio of the calculated market impact cost to the applicable 1-day volatility charge is greater than a set threshold, an MLA charge is applied to that asset group or subgroup.

- If the ratio is equal to or less than the threshold, no MLA charge is applied.

Threshold Basis:

- The threshold is based on an estimate of the market impact cost already included in the 1-day volatility charge calculation.

Calculation of MLA Charge:

- The MLA charge for each applicable group or subgroup is calculated as a proportion of:

- The amount by which the ratio of market impact cost to 1-day volatility charge exceeds the threshold.

- The 1-day volatility charge allocated to that group or subgroup.

Total MLA Charge for Member Portfolios:

- NSCC adds the MLA charges for Net Unsettled Positions across all subgroups and asset groups to determine the total MLA charge for a member.

Adjustment Based on Ratio:

- The ratio of market impact cost to 1-day volatility charge also determines if a downward adjustment is applied to the total MLA charge.

- A higher ratio may lead to a larger adjustment, assuming NSCC could liquidate the position over a longer timeframe than the assumed margin period of risk.

Final MLA Charge Calculation:

- The final MLA charge is calculated daily and included in Members’ Required Fund Deposits when applicable.

Proposed Refinements:

- NSCC proposes to refine the equity asset group calculation by:

- Moving all Exchange Traded Products (ETPs), excluding Illiquid Securities, into the equities asset group and calculating impact costs at the security level.

- Adding a calculation for latent liquidity for equity ETFs with in-kind baskets.

Move Liquid ETPs into Equities Asset Group and Provide Security Level Market Impact Cost Calculations:

Reclassification of ETPs:

- NSCC proposes moving all ETPs, except those deemed Illiquid Securities, into the equities asset group.

- Currently, corporate bond ETPs and municipal bond ETPs are categorized under corporate bonds and municipal bonds, respectively.

Rationale for ETP Reclassification:

- ETPs, being traded on exchanges, have equity-like properties, such as security-level trading volume data.

- The impact costs of liquidating ETPs can be estimated similarly to other securities in the equities asset subgroups.

Illiquid Securities Treatment:

- ETPs classified as Illiquid Securities will remain in the Illiquid Securities category.

Revision of Market Impact Cost Calculation:

- NSCC plans to revise the calculation for the equities asset group and subgroups to estimate impact costs at the security level, not the subgroup level.

- This change is due to observed disparities in trading volumes and impact costs that are more security-specific within subgroups.

Elimination of Concentration Measurement:

- Currently, the MLA charge calculation includes measuring the concentration of Net Unsettled Positions in a subgroup.

- With the new approach, this measurement, based on subgroup concentration, will be removed.

Comparison with Volatility Charge:

- Currently, NSCC compares the market impact cost with a portion of the volatility charge allocated to Net Unsettled Positions in the same asset group or subgroup.

- With the new method, this comparison will be made at the asset group level for all groups, including equities, and will no longer be done at the subgroup level.

Proposed Improvements to ETF Calculations:

Objective of the Proposal:

- NSCC aims to refine the impact cost calculations for ETFs to better account for their market impact.

- This proposal is a response to regulatory feedback on NSCC’s margin methodologies.

Incorporation of "Latent" Liquidity:

- The proposed method intends to incorporate “latent” liquidity into the calculations to more accurately reflect the market liquidity of ETFs.

Nature of ETFs:

- ETFs are exchange-traded securities that track underlying assets like equities, corporate and municipal bonds, and treasury instruments.

- Unlike mutual funds, ETFs are created and redeemed with the help of authorized participants (APs), often financial institutions like banks.

Creation and Redemption of ETF Shares:

- APs can create ETF shares by delivering a pre-specified bundle of underlying securities (an "in-kind basket") or cash equivalent to the value of these securities.

- For redemption, APs exchange ETF shares for the in-kind basket of underlying securities or a cash equivalent.

Market Mechanics of ETFs:

- APs continuously create and redeem ETF shares based on market conditions and arbitrage opportunities.

- This mechanism helps ETFs to trade close to the value of their underlying securities.

Arbitrage and Market Price Alignment:

- If the ETF’s market price is above the value of its underlying securities, APs can profit by purchasing the underlying securities at a lower price and exchanging them for new ETF shares.

- Conversely, if the ETF’s market price is below the value of its underlying securities, APs can buy ETF shares on the market and redeem them for the underlying securities.

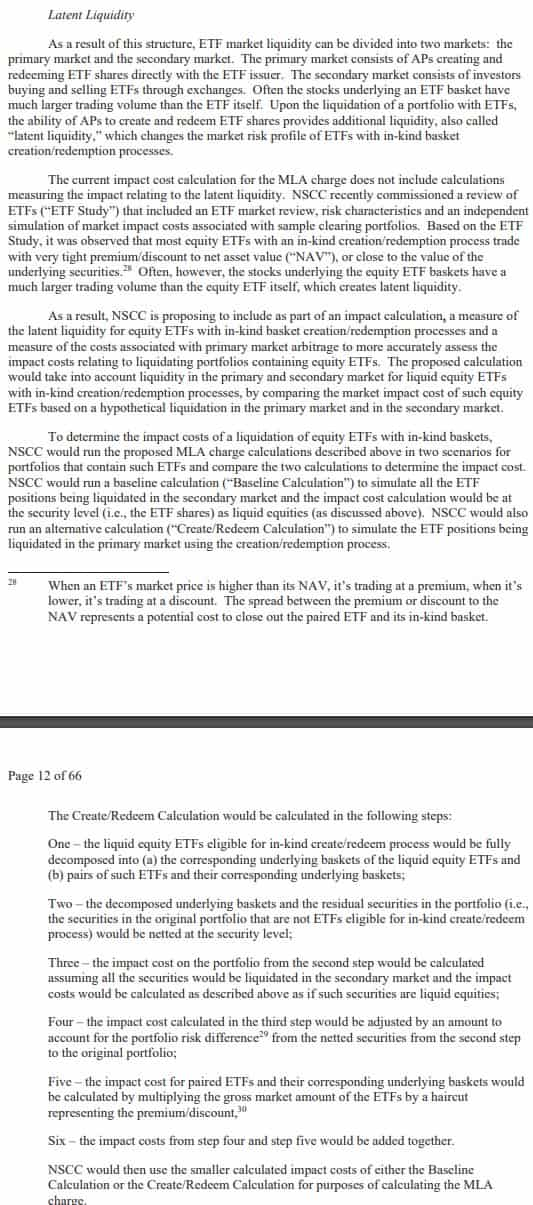

Latent liquidity:

Two Markets for ETF Liquidity:

- ETF market liquidity is divided into the primary market (APs creating and redeeming shares with the issuer) and the secondary market (investors trading ETFs on exchanges).

Latent Liquidity in ETFs:

- Due to the ability of APs to create and redeem ETF shares, there's additional liquidity, known as “latent liquidity,” in ETFs with in-kind basket creation/redemption processes.

- This latent liquidity alters the market risk profile of these ETFs.

Current Calculation Limitations:

- The current MLA charge impact cost calculation does not factor in the latent liquidity related to ETFs.

Findings from the ETF Study:

- Most equity ETFs with in-kind processes trade close to the net asset value (NAV) of their underlying securities.

- Stocks in equity ETF baskets often have larger trading volumes than the ETFs themselves, contributing to latent liquidity.

Proposed Calculation Inclusions:

- NSCC proposes including measures of latent liquidity and primary market arbitrage costs in the impact cost calculation for equity ETFs.

- The calculation would consider liquidity in both the primary and secondary markets for these ETFs.

Determining Impact Costs:

- NSCC would run two scenarios for portfolios containing such ETFs and compare calculations to determine impact costs:

- Baseline Calculation:

- Simulate ETF positions being liquidated in the secondary market.

- The impact cost is calculated at the security level as liquid equities.

- Create/Redeem Calculation:

- Simulate ETF positions being liquidated in the primary market.

- Involves decomposing ETFs into underlying baskets, netting securities, calculating impact costs, and adjusting for portfolio risk differences.

- Includes calculating impact costs for paired ETFs and their underlying baskets, with a haircut representing premium/discount.

- Baseline Calculation:

Choosing the Lesser Impact Cost:

- NSCC would use the smaller calculated impact cost from either the Baseline or Create/Redeem Calculation for the MLA charge.

Proposed Changes to MLA Charge Description with Respect to SFT Positions:

Wut Mean?:

Updating Rule 56 for MLA Charge Clarification:

- The proposed change aims to update the language in Rule 56, which describes the SFT Clearing Service.

Categorization of SFT Positions:

- NSCC will clarify that SFT Positions are categorized in the same asset groups or subgroups as the underlying SFT Securities.

- This replaces the previous language that stated SFT Positions were “aggregated with” Net Unsettled Positions in the same group or subgroup.

Clarification on Added Calculation for SFT Positions:

- The rule change will clarify calculations when a Member’s portfolio contains both SFT Positions and either Net Unsettled Positions or Net Balance Order Unsettled Positions.

- The current language does not explicitly reference Net Balance Order Unsettled Positions, which are treated similarly to Net Unsettled Positions in these calculations.

- The proposed language will include a reference to Net Balance Order Unsettled Positions.

Nature of the Clarifications:

- These clarifications will not change how NSCC calculates the MLA charge for SFT positions but are intended to improve clarity and understanding.

Additional Sentence in Procedure XV:

- NSCC proposes to add a sentence in Sections I(A)(1)(g) and I(A)(2)(f) of Procedure XV.

- This sentence will clarify that if a Member’s portfolio includes both SFT Positions and either Net Unsettled Positions or Net Balance Order Unsettled Positions, the MLA charge calculation will follow the stipulations set forth in Rule 56.

Proposed Changes to NSCC Rules:

Wut Mean?:

Implementation into Procedure XV:

- The proposal will be incorporated into Sections I(A)(1)(g) and I(A)(2)(f) of Procedure XV of the Rules.

- These sections will be amended to reclassify all ETPs (except Illiquid Securities) as subgroups within the equities asset group.

Footnote for Clarification:

- A footnote will clarify the categorization of ETPs with underlying securities in specific equities asset subgroups and the treatment of ETPs deemed Illiquid Securities.

Amendments for ETFs with In-Kind Baskets:

- Language will be added to indicate that impact cost calculations for ETFs with in-kind baskets will compare costs in both the secondary and primary markets.

- Two scenarios for impact cost calculations:

- Baseline Calculation: Simulating ETFs being liquidated in the secondary market at the security level.

- Create/Redeem Calculation: Simulating liquidation in the primary market using the creation/redemption process.

Restructuring of Impact Cost Calculations:

- The market impact calculation for securities in the equities asset group will shift from the subgroup level to the security level.

- The component measuring the concentration of Net Unsettled Positions in a subgroup will be removed.

Removal of Subgroup References:

- References to subgroup calculations, including comparisons with the volatility charge and MLA charges at the subgroup level, will be removed.

- Treasury ETP and other ETP subgroup references will also be removed, as they will be included in the equities asset group.

Total MLA Charge Calculation:

- Language will be added to clarify that all MLA charges for each asset group will be aggregated to determine the total MLA charge for each member.

Implementation Timeframe:

Oh yeah, a bunch of confidential exhibits:

How to comment:

Interested persons are invited to submit written data, views and arguments concerning the foregoing, including whether the proposed rule change is consistent with the Act. Comments may be submitted by any of the following methods:

Electronic Comments:

- Use the Commission’s Internet Comment Form:

- Access the form at http://www.sec.gov/rules/sro.shtml.

- Fill in the required details and submit your comment.

- Send an Email:

- Address your email to [email protected].

- Be sure you include "File Number SR-NSCC-2023-011" in the subject line of your email.

Paper Comments:

- Mail Comments in Triplicate:

- Send your comments (three copies) to the following address:

Secretary, Securities and Exchange Commission,

100 F Street, NE,

Washington, DC 20549. - Mention "File Number SR-NSCC-2023-011" in your submission.

- Send your comments (three copies) to the following address:

Avoid including personal identifiable information as submissions are made public. Comments due 21 days after being published in the Federal Register.

TLDRS:

- NSCC proposes updating MLA charge by moving all exchange traded products (other than those deemed to be Illiquid Securities) into the equities asset group & calculating impact cost at the security level along with ETF tweaks.

- The proposal seeks to refine how the MLA charge is calculated for liquidating securities or portfolios, particularly for exchange-traded products (ETPs) and equity ETFs.

- All ETPs, except those deemed Illiquid Securities, will be reclassified into the equities asset group.

- The impact cost for ETPs will be calculated at the individual security level, rather than at the subgroup level.

- For equity ETFs, particularly those with in-kind baskets, new calculations will include latent liquidity to better reflect market liquidity.

- An impact study indicated that these changes would have resulted in an approximate $62 million daily average increase in the MLA charge, accounting for about 0.52% of the daily total Clearing Fund.

- NSCC will compare the calculated market impact cost to the allocated portion of the volatility charge for each asset group or subgroup.

- An MLA charge will be applied if the ratio of market impact cost to the 1-day volatility charge exceeds a set threshold.

- The proposal includes running two scenarios (Baseline and Create/Redeem Calculations) to determine the impact costs for portfolios containing ETFs, with the smaller impact cost being used for the MLA charge calculation.

- The proposed changes aim to update Rule 56 to clarify the categorization and calculation of the Market Liquidity Adjustment (MLA) charge for Securities Financing Transactions (SFT) Positions.

- SFT Positions will be categorized in the same asset groups or subgroups as their underlying SFT Securities, replacing the previous aggregation language.

- The rule change will include clarifications for calculating the MLA charge when a member’s portfolio contains both SFT Positions and either Net Unsettled Positions or Net Balance Order Unsettled Positions.

- For ETFs with in-kind baskets, impact cost calculations will include comparisons of costs in both secondary and primary markets, involving Baseline and Create/Redeem Calculations.

- The market impact calculations for securities in the equities asset group will move from the subgroup level to the security level, and subgroup references will be removed.

- Clarifying language will be added to ensure that all MLA charges across asset groups are aggregated to determine the total MLA charge for each member.

- Open for comment!