CFTC Alert! CFTC Seeks Public Comment on Proposed Rule to Amend Capital and Financial Reporting Requirements of Swap Dealers and Major Swap Participants. Comments close on February 13, 2024.

Additional Information:

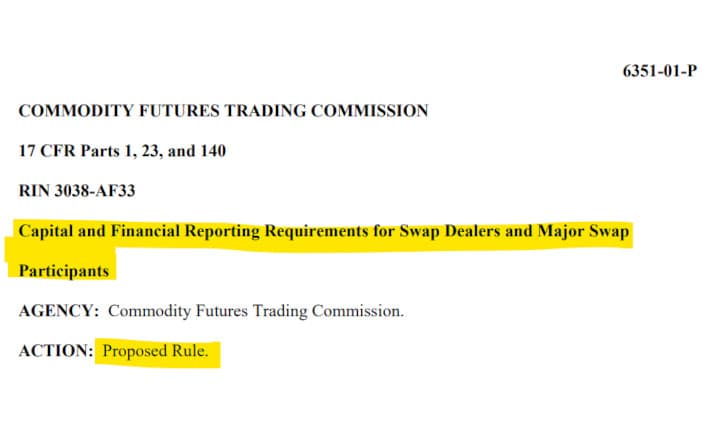

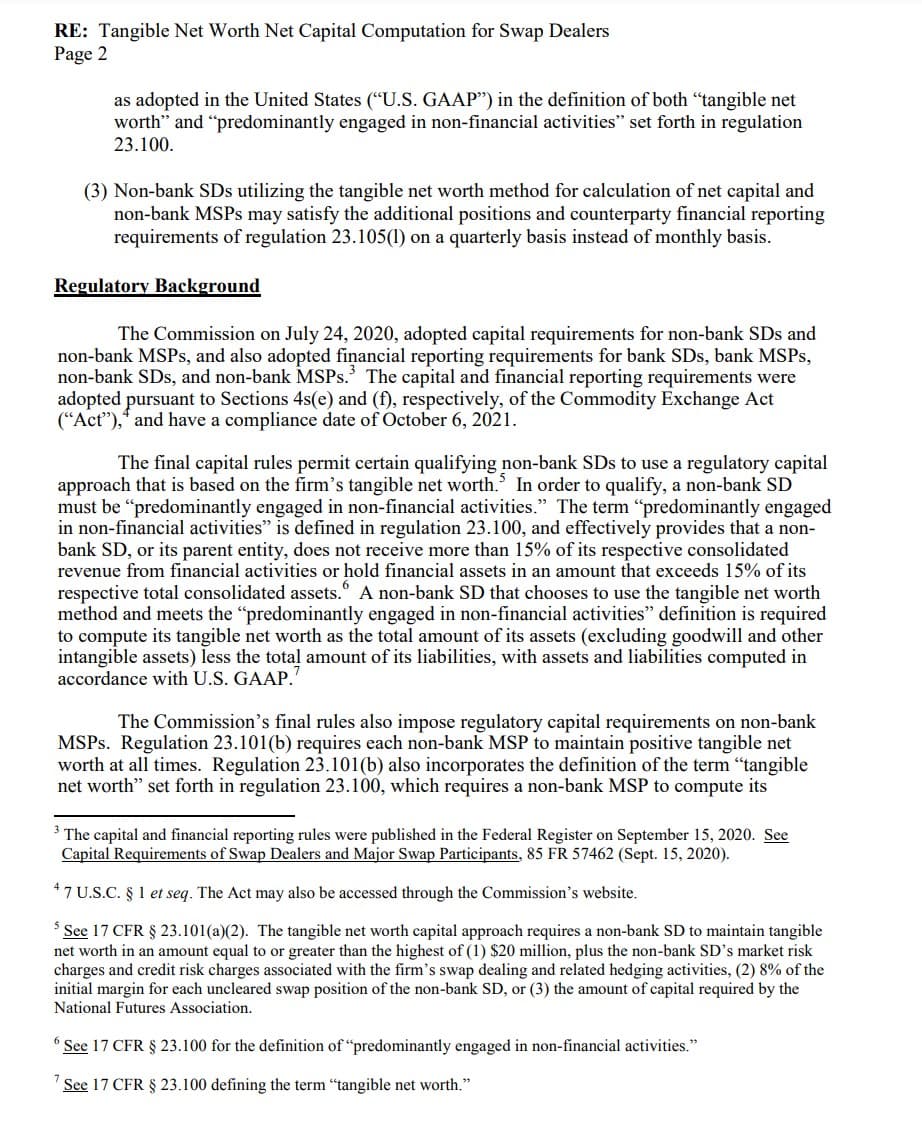

On September 15, 2020, the Commission published in the Federal Register final rules adopting capital and financial reporting requirements for SDs and MSPs. The Final Rules accomplished the Congressional mandate directing the Commission to adopt rules imposing both capital requirements and initial and variation margin requirements on SDs and MSPs that are not subject to a prudential regulator (“nonbank SDs” and “nonbank MSPs”, respectively). The Final Rules included amendments to existing capital rules for futures commission merchants (“FCMs”) to provide explicit additional capital requirements for proprietary positions in swaps and security-based swaps that are not cleared by a clearing organization. The Final Rules also included a detailed capital model application process whereby eligible nonbank SDs and nonbank MSPs could apply to the Commission or a registered futures association (“RFA”) of which they are a member for approval. Further, the Final Rules adopted a capital comparability determination process for certain eligible foreign domiciled nonbank SDs and nonbank MSPs to seek substituted compliance for the Commission’s capital and financial reporting requirements. Finally, the Final Rules adopted detailed financial reporting, recordkeeping and notification requirements, including limited financial reporting requirements for SDs and MSPs subject to the capital requirements of prudential regulators (“bank SDs” and “bank MSPs”, respectively).

The Commission initially proposed capital and financial reporting requirements for nonbank SDs and nonbank MSPs, and financial reporting requirements for bank SDs and bank MSPs, in 2011. After extensive comment, in 2016 the Commission re-proposed the rules for comment. The Commission received numerous comments from a broad spectrum of market participants in response to the re-proposal. In addition, following the 2016 re-proposal, the SEC adopted a final set of capital, margin and financial reporting requirements for security-based swap dealers and major security-based swap participants (“SBSDs” and “MSBSPs,” respectively). In December 2019, the Commission re-opened the proposed rules for comment in light of the SEC’s final rules, and requested commenters to provide detailed data and information regarding several critical areas of the Commission’s proposed approach.

The Final Rules became effective November 16, 2020. To address concerns from commenters that a sufficient period of time would be necessary to develop policies, procedures and systems to implement the new financial reporting requirements and to develop and obtain approval to use capital models, the Commission adopted an extended compliance date of October 6, 2021 (“Extended Compliance Date”). The Extended Compliance Date also corresponded to the SEC’s compliance date for SBSDs and MSBSPs, thus permitting better coordination for dually-registered entities.

The Commission’s overall capital approach in the Final Rules permits nonbank SDs and MSPs to select one of three methods to calculate their capital requirements. Each method is discussed in detail in the Final Rule and determines the frequency and type of financial reporting information to be provided to the Commission by each nonbank SD and nonbank MSP. Bank SDs, which are not subject to the capital requirements of the Commission, are required to provide the Commission and National Futures Association (“NFA”) with limited financial information regarding the capital and swap positions of the firms. Bank SDs are required to file the limited financial information using CFTC forms that were intended to be comparable with forms required by the prudential regulators and consistent with forms adopted by the SEC for SBSDs subject to the capital rules of a prudential regulator. Together, the financial reporting and notice requirements included in the Final Rules serve as the mechanism for the Commission to monitor capital compliance by nonbank SDs.

In the Final Rule, the Commission also recognized the role of NFA as the only RFA under the CEA. NFA is an integral component of the Commission’s registration and oversight program. Specifically, the Commission has authorized NFA to administer the registration process for SDs and MSPs, and to approve the use of capital and initial margin models. NFA also conducts examinations of nonbank SDs and nonbank MSPs to assess compliance with Commission and NFA rules. As such, the Final Rules required that financial reports and notices be filed with both the Commission and the NFA, and explicitly recognized NFA’s ability to adopt standardized forms and processes to carry out the Commission’s financial reporting and notification requirements for SDs.

During the period leading up to the Extended Compliance Date, Commission, NFA, and SEC staff collaborated to develop a process for the collection of financial reports and to respond to inquiries from industry participants regarding compliance with financial reporting and notice obligations. On January 12, 2021, Commission staff approved NFA’s capital model application process. On December 21, 2021, NFA adopted new Financial Requirements Section 18 of its rules, which in addition to including capital rules largely modeled after those adopted by the Commission in the Final Rules, published newly developed standardized financial reporting forms FR-CSE-NLA and FR-CSE-BHC for use by nonbank SDs that are not also registered with the SEC.

Prior to the Extended Compliance Date, Commission staff also received inquiries from market participants regarding compliance with various capital and financial reporting obligations under the Final Rule. In response, Commission staff issued eight no-action and interpretative letters. Two letters, CFTC Letters No. 21-15 and 21-18, are discussed below in detail and inform this proposed rulemaking. In addition, the Commission is proposing several other amendments that are the result of Commission staff’s experience implementing the Final Rule. These amendments are intended to provide technical and other clarifying changes necessary to effectuate the Final Rule’s purpose.

Wut Mean?:

- The Commodity Futures Trading Commission (CFTC) adopted final rules on September 15, 2020, setting capital and financial reporting requirements for Swap Dealers (SDs) and Major Swap Participants (MSPs) that are not subject to a prudential regulator.

- These rules include amendments to existing capital rules for futures commission merchants (FCMs) and introduce a capital model application process for eligible nonbank SDs and MSPs, along with a capital comparability determination process for certain foreign domiciled entities.

- The Final Rules, effective November 16, 2020, were initially proposed in 2011 and re-proposed in 2016.

- The CFTC set an extended compliance date of October 6, 2021, to allow for the development of necessary policies, procedures, and systems, and to align with the SEC’s compliance date for better coordination of dually-registered entities.

- Nonbank SDs and MSPs can choose from three methods to calculate their capital requirements, determining the frequency and type of financial reporting to the CFTC.

- Bank SDs, exempt from CFTC capital requirements, must provide limited financial information on capital and swap positions.

- The National Futures Association (NFA) plays a key role in administering the registration process for SDs and MSPs, approving capital and initial margin models, and conducting compliance examinations.

- Leading up to the Extended Compliance Date, the CFTC, NFA, and SEC staff collaborated on developing financial report collection processes.

- The CFTC staff issued several no-action and interpretative letters to address inquiries from market participants, leading to proposed amendments for technical and clarifying changes in the Final Rule.

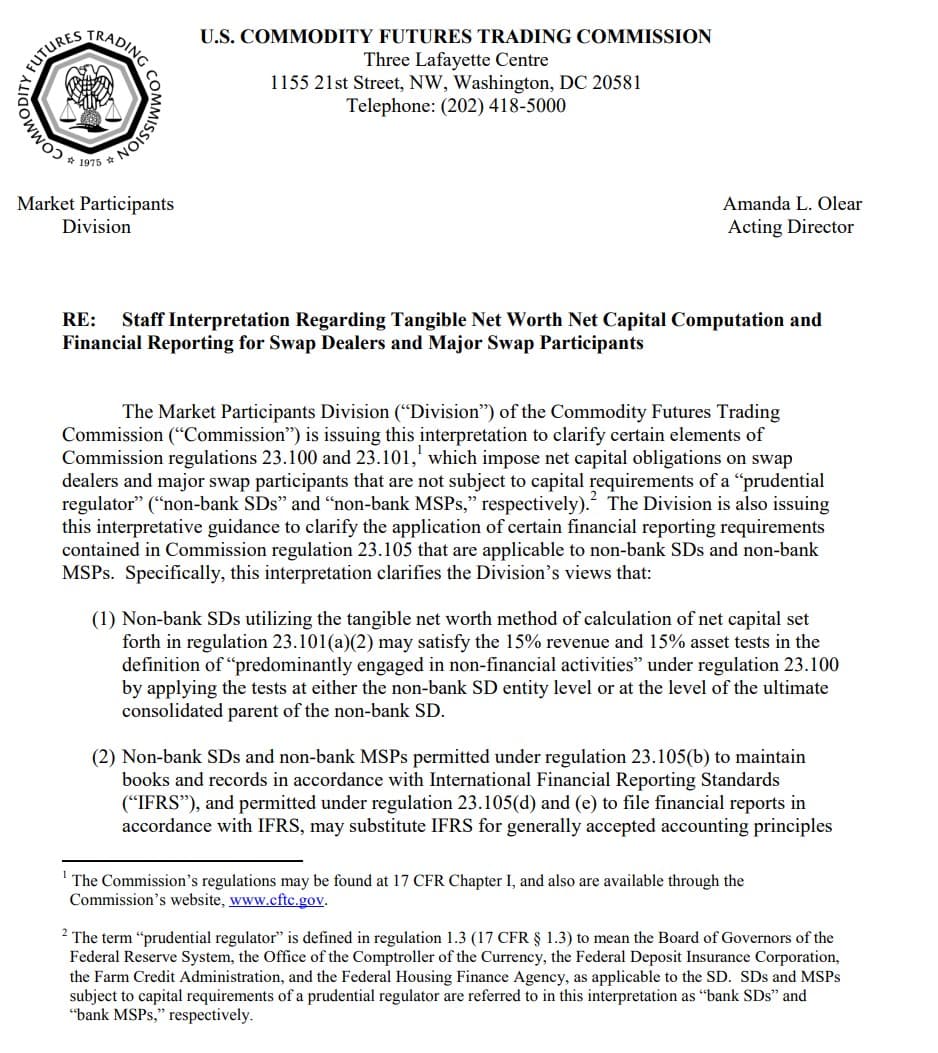

CFTC Staff Letter No. 21-15:

CFTC Staff Letter No. 21-18:

Wut Mean?:

- The Commission recognized that prudential regulators are primarily responsible for imposing capital requirements on Bank Swap Dealers (SDs) and, as such, finalized limited financial reporting requirements for these entities.

- The limited reporting is designed to enable the Commission to monitor the financial condition of Bank SDs due to their role in the swaps market and as counterparties to various market participants.

- The staff interpretation clarifies that non-bank Swap Dealers (SDs) can use the tangible net worth method for net capital calculation and meet the "predominantly engaged in non-financial activities" criteria either at their level or their ultimate consolidated parent's level.

- Non-bank SDs and Major Swap Participants (MSPs) using International Financial Reporting Standards (IFRS) can substitute IFRS for U.S. Generally Accepted Accounting Principles (GAAP) in defining "tangible net worth" and "predominantly engaged in non-financial activities."

- These entities can satisfy additional positions and counterparty financial reporting requirements on a quarterly basis instead of monthly.

- The staff believes that the preamble to the final rules supports the flexibility for certain corporate structures to qualify for the tangible net worth capital approach, without restricting it to non-bank SD’s parent entities meeting the revenue and asset tests.

- Non-bank SDs and MSPs permitted to use IFRS for maintaining current books and records and for financial reporting to the Commission are also allowed to use IFRS in calculating tangible net worth.

- An alternate approach would require maintaining two sets of accounting records, which is nullified by the Commission’s authorization for firms to maintain books and records in IFRS.

- The staff clarifies that non-bank SDs using the tangible net worth capital approach and non-bank MSPs may file financial information required under Appendix B to Subpart E of Part 23 quarterly, instead of monthly.

- This quarterly filing reflects the Commission's decision to require monthly reporting only for non-bank SDs using a capital approach other than the tangible net worth approach.

- The inconsistency in the quarterly financial report filing requirement and the monthly Appendix B filing requirement for these entities was viewed as a 'technical oversight' in the drafting of the final regulations.

- The staff state the Division will not recommend enforcement action against Bank SDs failing to comply with certain Regulation 23.105(p)(2) requirements if specific conditions are met.

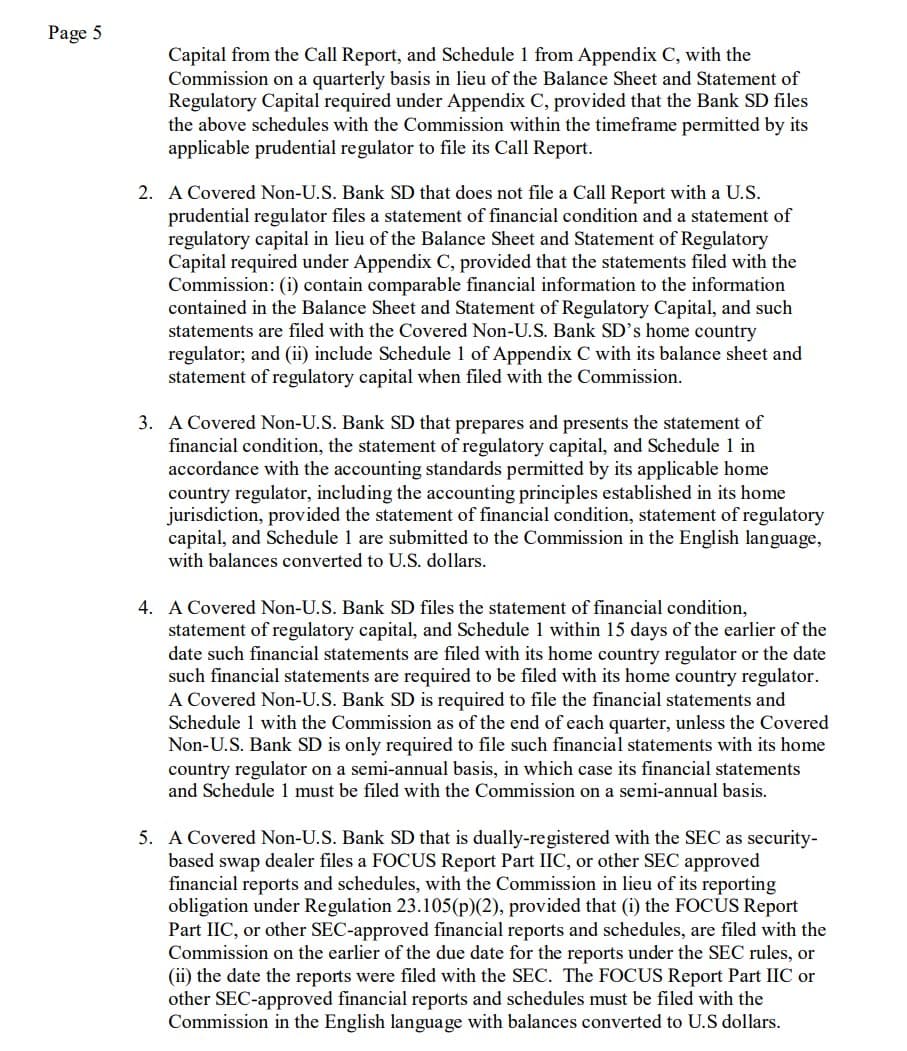

- Bank SDs filing Call Reports with U.S. prudential regulators may file specific schedules from the Call Report with the Commission on a quarterly basis instead of the required Balance Sheet and Statement of Regulatory Capital.

- Covered Non-U.S. Bank SDs not filing Call Reports in the U.S. must file a statement of financial condition and regulatory capital with comparable information, including Schedule 1 of Appendix C.

- These Covered Non-U.S. Bank SDs must prepare financial statements in accordance with their home country's accounting standards, translated into English and converted to U.S. dollars.

- They must file these statements within 15 days of the earlier of the date filed with their home regulator or the required filing date, either quarterly or semi-annually based on home country requirements.

- Covered Non-U.S. Bank SDs that are also registered with the SEC as security-based swap dealers can file a FOCUS Report Part IIC or other SEC-approved reports with the Commission in lieu of Regulation 23.105(p)(2) obligations.

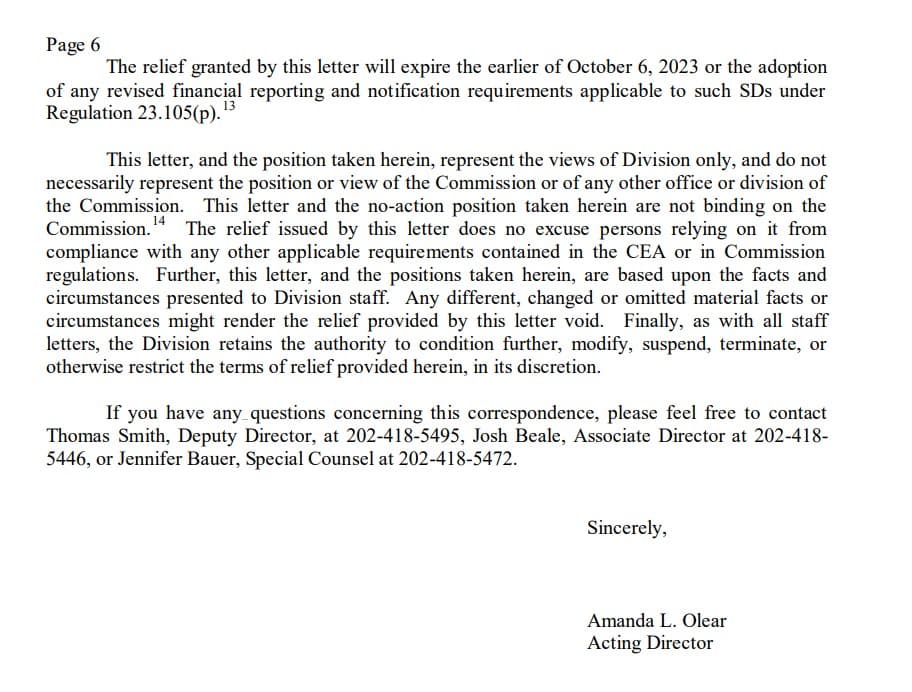

- This relief expired on October 6, 2023, or upon the adoption of any revised financial reporting requirements for SDs under Regulation 23.105(p).

- The Division retains the authority to modify, suspend, or terminate the terms of this relief based on changing circumstances or omitted material facts.

Fact Sheet:

Statement of Chairman Rostin Behnam:

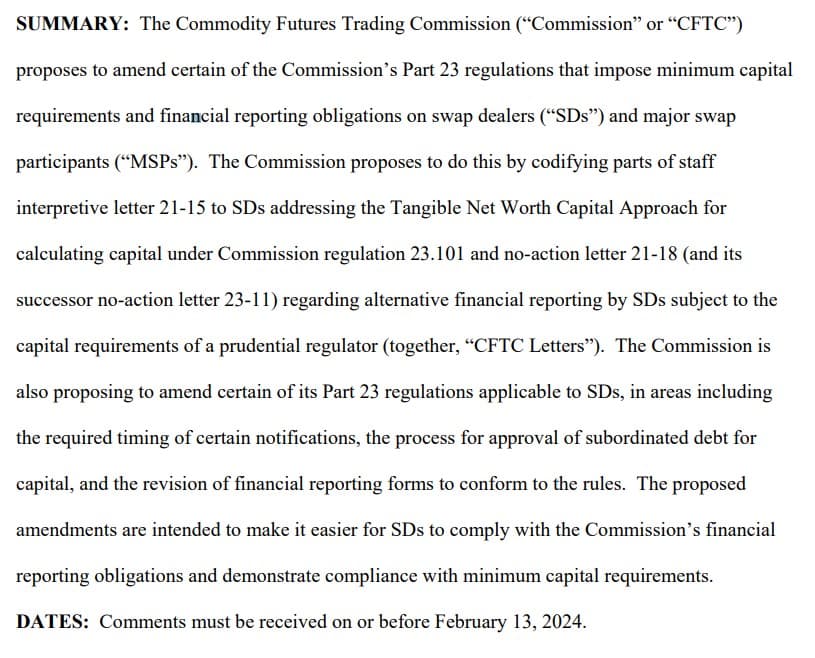

I support the proposed rule to amend certain requirements in Part 23 of the Commission’s regulations to address specific issues identified during the implementation of the Commission’s 2020 final rule on capital and financial reporting requirements for swap dealers (SDs) and major swap participants (MSPs).[1] The proposed rule would codify interpretive CFTC Letter No. 21-15[2] regarding capital and financial reporting requirements for nonbank SDs and nonbank MSPs electing the tangible net worth capital approach;[3] codify the time-limited no-action position in CFTC Letter No. 21-18[4] regarding financial reporting requirements for bank SDs; clarify technical aspects of the reporting requirements; and update an FCM reporting form consistent with net capital requirements previously adopted by the Commission for FCMs. The proposed amendments are not intended to change the Commission’s capital approach.

This proposal is a testament to the commitment I previously made for the Commission to consider the codification of various forms of relief previously provided by CFTC Division staff through no-action position letters.[5] As staff letters only bind the staff of the issuing Division with respect to the specific facts, situations, and persons addressed by the respective staff letters,[6] it is good government for the Commission to clean-up its rule set where the Commission determines that compliance with certain regulations is impossible. Such Commission action not only provides regulatory certainty and clarity to our registrants with the benefit of notice and public comment, but also ensures the efficient use of staff resources to fix an issue once instead of allocating time to a series of no-action positions for the same matter.

I look forward to hearing the public's comments on the proposed amendments to the regulations and the relevant appendices in Part 23 of the Commission’s regulations. I thank staff in the Market Participants Division, Office of the General Counsel, and the Office of the Chief Economist for all of their work on the proposal.

Statement of Commissioner Kristin N. Johnson:

The Commodity Futures Trading Commission (Commission or CFTC) adopted a proposal to amend certain of the Commission’s Part 23 regulations that impose minimum capital requirements and financial reporting obligations on swap dealers (SDs) and major swap participants (MSPs) (Proposed Amendments).[1] I support the amendments advanced by the Market Participants Division (MPD).

Minimum capital requirements serve as a cushion during times of severe market stress to ensure our registrants’ safety and soundness, protect the financial stability of our financial system, and prevent a run on our financial institutions. Financial condition reporting provides the Commission with visibility and insight into the business and financial health of our registrants and enables us to require corrective action and prevent a failure of a single entity or group of entities or segment of the derivatives market, which could raise system risk concerns.

Dodd-Frank Act Reforms

The Commission introduced new capital and financial reporting requirements for SDs in 2020, as mandated by the Dodd-Frank Act (2020 Capital Rule).[2] Title VII of the Dodd-Frank Act amended the Commodity Exchange Act (CEA) to establish a new regulatory framework for swaps, regulated by the Commission, and security-based swaps, regulated by the Securities and Exchange Commission (SEC), to reduce risk, increase transparency, and promote market integrity within the financial system. Section 4s(e) of the CEA introduced minimum capital requirements for SDs,[3] and Section 4s(f) of the CEA created financial reporting and recordkeeping requirements for all SDs.[4]

In the United States, the capital framework is divided into three parallel regimes. SDs subject to regulation by a prudential regulator are required to comply with the minimum capital requirements adopted by the applicable prudential regulator,[5] while SDs not subject to regulation by a prudential regulator are required to meet the minimum capital requirements of the Commission, and security-based swap dealers (SBSDs) and major security-based swap participants (MSBSP) that do not have a prudential regulator are required to comply with the minimum capital requirements of the SEC.[6] The prudential regulators or banking agencies and the SEC have adopted capital rules for swaps and security-based swaps.

In the adopting release for the 2020 Capital Rule, the Commission indicated that it would consult with the prudential regulators and the SEC to assess the capital adequacy of SDs, MSPs, SBSDs, and MSBSPs, monitor the implementation of the rule and data, and consider modifications to the capital and financial reporting requirements.[7]

With the Proposed Amendments, the Commission seeks to make surgical changes to the 2020 Capital Rule, including a number of technical corrections, based on consultation with the prudential regulators and SEC, and based on market feedback on the adoption and implementation of the 2020 Capital Rule. While the Proposed Amendments are not adjusting the capital components of the 2020 Capital Rule, all regulations designed to mitigate known systemic risk concerns in the swaps market must be subject to careful evaluation.

I commend the Commission for taking formal steps to engage in a rulemaking process that invites Commission discussion and public notice and comment on these regulations, which ensure compliance with the Dodd-Frank Act while remaining practical and solutions-oriented. I strongly encourage the Commission, however, to begin a formal rulemaking process to address several unresolved issues necessary to ensure compliance with the Dodd-Frank Act and these requirements.

Clarifying Capital Requirements for Commercials

The Proposed Amendments codify Interpretive Letter 21-15, which applies to commercial non-bank SDs—typically entities that primarily engage in agricultural and energy swaps and provide services that are important to the U.S. economy. The Commission’s overall capital approach permits non-bank SDs to select one of three methods to calculate their capital requirements, as permitted under the rule: the net liquid assets capital approach;[8] the bank-based capital requirements;[9] or the tangible net worth capital approach.[10]

The Commission proposes to revise the 2020 Capital Rule so that the test to determine tangible net worth may be applied at the entity level or ultimate consolidated parent level; so that International Financial Reporting Standards (IFRS) accounting standards or GAAP may be used; and so that position and financial exposure reporting occur at the same frequency as financial reporting, which for SDs is quarterly.

The Proposed Rule minimizes disruption, and clarifies the interpretation and implementation of the tangible net worth test for commercial non-bank SDs.

Refining Financial Reporting Requirements

The Proposed Amendments address issues presented in No-Action Letter (NAL) 21-18, which was extended under NAL 23-11 and applies to bank SDs, including non-U.S. bank SDs. Non-U.S. bank SDs can file the applicable financial reporting within 90 days of the end of the financial reporting period and the same forms (e.g., relating to balance sheet and regulatory capital schedules) in the same format as provided to home country regulators (but in English and U.S. dollars). Additionally, U.S. bank SDs can file the same forms (e.g., relating to balance sheet and regulatory capital schedules) under bank regulators’ Call Report and within the same timeframe as when filing with their prudential regulator.

The Proposed Amendments allow the Commission to collect information from bank SDs as a comparative tool. Also, all SDs must use Schedule 1 for position information, which is similar to the SEC’s FOCUS report—duplicative forms are eliminated.

MPD has demonstrated collaboration working with the prudential regulators and the SEC in developing and harmonizing processes, procedures, and forms for financial reports and notifications—some of which are adopted the Proposed Amendments. Further, the 2020 Capital Rule was an important initiative that demonstrated the Commission’s recognition of the complexity and interconnectedness of the derivatives market.

Technical Corrections

SD Exposure Reporting

The Proposed Amendments amend Commission regulation to clarify that certain supplemental schedules used to report SD exposure are intended to be provided by all non-bank SDs. These amendments are necessary to align the reporting of similar information collected by the SEC from SBSDs and to provide the Commission and National Futures Association with important information regarding SD exposure across several geographical locations and counterparties. This information provides valuable insight into the risk exposure of non-bank SDs, which is essential to performing regulatory oversight of SDs.

Notice Requirements for Substantial Reduction in Capital

The Commission should begin to review notice requirements comprehensively in light of greater, faster capabilities to comply, notwithstanding the potential existence of challenges for non-U.S. SDs in light of time zone differences. The Proposed Amendments require notification of a substantial reduction of capital within two business days. The 2020 Capital Rule did not specify a timeframe, and the Proposed Amendments are consistent with the timeframe applicable to FCMs.

Conclusion

In order to prevent the market instability witnessed during the period when swaps traded in bespoke, bilateral markets, the Commission imposes capital requirements on non-bank SDs, and imposes financial reporting requirements on bank SDs as well as non-bank SDs. These regulations are critical to the oversight of the swaps market.

I want to thank the Market Participants Division and Office of the Chief Economist for their excellent work bringing forth this proposed rulemaking, in particular Jennifer Bauer, Maria Aguilar-Rocha, Andrew Pai, Joshua Beale, Thomas Smith, and Amanda L. Olear of MPD, and Lihong McPhail of OCE.

Supporting Statement of Commissioner Summer K. Mersinger:

I am pleased to support the Commission’s notice of proposed rulemaking (“NPRM”) to codify in the agency’s rules previously-issued Staff relief regarding capital and financial reporting requirements for registered swap dealers (“SDs”).[1]

Staff relief such as no-action and interpretative letters[2] are useful tools in appropriate circumstances. But when there is an issue or problem with our rules, a notice-and-comment rulemaking process is the gold standard. On several occasions when no-action relief has been repeatedly extended over lengthy periods of time, I have encouraged the Commission to instead undertake rulemaking to hear from stakeholders, craft solutions, and provide certainty.[3]

Here, during the course of implementing the Commission’s rules imposing minimum capital requirements and financial reporting obligations on SDs,[4] our Staff received several inquiries about the application of the rules from market participants seeking to come into compliance. This was not surprising, given the complexity of these rules and the efforts to harmonize them with requirements being imposed by prudential bank regulators and the SEC.

In response, Staff issued several no-action and interpretative letters, and today, the Commission is proposing to codify parts of two of them into our rulebook.[5] In addition, based on experience implementing the SD capital and financial reporting rules, the Commission also is proposing other amendments intended to provide technical and clarifying changes to effectuate the purposes of the rules.

I commend the Staff of our Market Participants Division for issuing appropriate no-action and interpretative letters when it was necessary to address legitimate inquiries raised by market participants, and for preparing this proposal to make portions of those letters a permanent part of our rule set. I look forward to public comment on whether we have gotten these proposed amendments right.

Statement of Commissioner Caroline D. Pham:

I support the Notice of Proposed Rulemaking on Capital and Financial Reporting Requirements for Swap Dealers and Major Swap Participants (Proposal) because it addresses issues left outstanding from implementing a rule by offering pragmatic solutions that not only rectify the problem at hand, but do so without imposing unnecessary burdens or complications. I would like to thank Andrew Pai, Maria Aguilar-Rocha, Josh Beale, Tom Smith, and Amanda Olear in the Market Participants Division for their work on the Proposal. I greatly appreciate the time staff took to discuss my questions and concerns.

It is important to remember that most of the CFTC’s provisionally-registered swap dealers are subject to three or more regulatory regimes.[1] Of the CFTC’s 106 currently provisionally registered swap dealers, most are also registered with and supervised by another agency or authority, such as a prudential, functional, or market regulator. This awareness must inform the Commission’s approach when considering any rule impacting swap dealers.[2] Otherwise, we risk missing the nuances associated with the complex interplay or conflict that arises between the various regulations.

Capital, the subject of today’s Proposal, is one area in which the CFTC’s provisionally-registered swap dealers are subject to multiple regulatory regimes. By this point, we know that the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) mandated the Commission establish capital requirements for swap dealers and major swap participants,[3] and that the Commission adopted capital requirements for nonbank swap dealers and major swap participants,[4] as well as financial reporting requirements for bank swap dealers and major swap participants, together with nonbank swap dealers and major swap participants.[5]

Therefore, when considering solutions to challenges that have arisen while implementing the capital rules, we must remember that we are not a prudential banking regulator like the Fed, OCC, or FDIC, nor are we a primarily disclosures-based market regulator like the SEC.[6] Today’s proposal offers a pragmatic solution to challenges faced by our market participants that respects the differences among the financial regulators.

The extent of capitalization and reach of financial reporting were decided years ago and are not the subject of today’s Proposal. Rather, today we consider, primarily, fixing issues that arose when implementing the capital and financial reporting rules,[7] and secondarily, miscellaneous technical changes to make the rules more workable.

I support the entire Proposal, but will focus my comments on the codification of: (1) CFTC Staff Interpretative Letter No. 21-15 for commercial swap dealers and major swap participants electing the Tangible Net Worth Capital Approach;[8] and (2) the time-limited, no-action relief in CFTC Letter No. 21-18[9] regarding financial reporting requirements for bank swap dealers and major swap participants.[10]

Before I begin, I want to draw attention to a bigger issue relating to capital for the coming year. The broad impacts of the Basel III Endgame are being widely reported and discussed,[11] including impact to CFTC swap dealers and major swap participants.[12] I am deeply concerned about this issue for our markets, which is why I expect that under my sponsorship, the Global Markets Advisory Committee (GMAC) will work on offering actionable recommendations for the Commission in this area. I encourage everyone to watch the presentation made on the subject at the recent November 6th meeting via the meeting’s archived webcast,[13] and look forward to working with the GMAC and all of you on the issue in 2024.

A. Codifying CFTC Letter No. 21-15

Nonbank swap dealers and major swap participants can elect one of three approaches to calculating their regulatory capital.[14] One option allows certain qualifying nonbank swap dealers and major swap participants to use a regulatory capital approach that is based on the firm’s tangible net worth.[15] Generally, these nonbank swap dealers and major swap participants have to be “predominantly engaged in non-financial activities” and maintain positive tangible net worth according to U.S. generally accepted accounting practices (GAAP) at all times.[16]

When the rules were being implemented, nonbank swap dealers identified three problems: (1) the rule’s preamble expanded the definition of “predominantly engaged in financial activities” to permit these nonbank swap dealers and major swap participants to meet the regulation’s tangible net worth test directly or through its ultimate consolidated parent entity, but the text of Regulation 23.100 was unclear about it; (2) Regulation 23.105(b) allowed books and records to be maintained in accordance with International Financial Reporting Standards (IFRS) but the “tangible net worth” definition in Regulation 23.100 only referenced U.S. GAAP; and (3) there was an inconsistency in the timelines of certain financial reports required by Regulation 23.105(l).[17]

To fix these issues, the Commission is proposing to adopt the remedies provided in Letter No. 21-15: revise the definitions of “tangible net worth” and “predominantly engaged in non-financial activities” and Regulation 23.105 to clarify the test can be applied at the parent or entity level, as well as using U.S. GAAP or IFRS; and amend Regulation 23.105(l) to clarify that position and other related exposure reporting must be made at the same frequency as financial reporting, which in this instance is quarterly.

B. Codifying CFTC Letter No. 21-18

Bank swap dealers and major swap participants must file unaudited quarterly financial information with the CFTC within 30 calendar days of the end of their fiscal quarter.[18] The information should be submitted via the specific forms in Appendix C to Subpart E of Part 23. The Commission intended that these forms would be identical to those filed by banks with their prudential regulator. However, when the capital and financial reporting rules were being implemented, it became evident that there were some differences in the forms, as well as with the timelines for filing.

Therefore, CFTC Letter No. 21-18 let bank swap dealers and major swap participants provide home country regulator reports and comparable schedules on the prudential regulators’ timeline; foreign bank swap dealers and major swap participants provide home country regulator balance sheets and statements of regulatory capital information as long as they are in English, USD, and within 15 days of filing with home country regulator; and SEC dually-registered foreign bank swap dealers and major swap participants file comparable SEC approved financial reports and schedules.

To fix these issues, the Commission is proposing to adopt the remedies provided in CFTC Letter No. 21-18: amend Regulation 23.105(p) to allow foreign bank swap dealers and major swap participants to file the applicable financial reporting within 90 days of the end of the financial reporting period; accept balance sheet and regulatory capital schedules under prudential regulator reports for U.S. bank swap dealers and major swap participants; and to accept the filing of such schedules at the same time as filed with prudential regulators. For foreign swap dealers, the Commission is proposing to permit the filing of a balance sheet and statement of regulatory capital schedules in the format provided to their home country regulator, as long as they are in English and converted to USD, and filed no later than 90 days following the reporting period end date.

I support this rule because codifying well-tailored relief helps provide market certainty while avoiding imposing unnecessary burdens and creating compliance complications. I also support this rule because the Commission does so while also continuing to respect the differences between our rules and those of the other regulators overseeing swap dealers on capital. It is a laudable achievement. I again commend staff in the Market Participants Division for their hard work on this rule, and look forward to reviewing the comments.

How to comment:

- Comments may be submitted electronically through the CFTC Comments online process.

- All comments received will be posted on CFTC.gov.

- The comment period will be open for 60 days after publication on CFTC.gov, and close on February 13, 2024.

TLDRS:

- The Commodity Futures Trading Commission (CFTC) is proposing amendments to regulations regarding capital and financial reporting requirements for swap dealers (SDs) and major swap participants (MSPs).

- The proposal aims to codify relief provided in CFTC Letters No. 21-15 and 21-18, which pertain to the tangible net worth capital approach for nonbank SDs and MSPs, and the financial reporting requirements for bank SDs, respectively.

- The amendments will clarify the general applicability of reporting schedules, the approval process for subordinated debt, notification timeframes for significant capital reductions, material differences between audited and unaudited financial reports, and public disclosure formats for regulatory capital.

- The proposal includes changes to the Commission’s Form 1-FR-FCM to reflect previous modifications to FCM net capital requirements related to swaps.

- The changes will allow nonbank SDs and MSPs to use either U.S. Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS) in calculating "tangible net worth."

- The amendments will enable nonbank SDs using the tangible net worth capital approach and nonbank MSPs to file required financial information quarterly instead of monthly.

- Bank SDs can file specific schedules from their Call Reports in lieu of current forms, and non-U.S. domiciled bank SDs can file financial statements in the format provided to their home country regulator.

- Subordinated debt qualifying for net capital will be subject to a determination by the Commission or the National Futures Association (NFA).

- The amendments will clarify market and credit risk charges for SDs using internal models under the Bank-Based Capital Approach and those not using internal models.

- Financial reporting requirements will be adjusted for SDs also registered with the SEC as broker-dealers or security-based swap dealers, and audited financial report requirements will include statements on material inadequacies.

- Public disclosure of SD unaudited statement of financial condition information will now include footnote disclosures, and the format for public disclosure of regulatory capital information will be more flexible.

- Chairman Rostin Behnam: "I support the proposed rule to amend certain requirements in Part 23 of the Commission’s regulations to address specific issues identified during the implementation of the Commission’s 2020 final rule on capital and financial reporting requirements for swap dealers (SDs) and major swap participants (MSPs)."

- Commissioner Kristin N. Johnson: "I commend the Commission for taking formal steps to engage in a rulemaking process that invites Commission discussion and public notice and comment on these regulations, which ensure compliance with the Dodd-Frank Act while remaining practical and solutions-oriented. I strongly encourage the Commission, however, to begin a formal rulemaking process to address several unresolved issues necessary to ensure compliance with the Dodd-Frank Act and these requirements."

- "In order to prevent the market instability witnessed during the period when swaps traded in bespoke, bilateral markets, the Commission imposes capital requirements on non-bank SDs, and imposes financial reporting requirements on bank SDs as well as non-bank SDs. These regulations are critical to the oversight of the swaps market."

- Commissioner Summer K. Mersinger: "I am pleased to support the Commission’s notice of proposed rulemaking (“NPRM”) to codify in the agency’s rules previously-issued Staff relief regarding capital and financial reporting requirements for registered swap dealers (“SDs”)."

- Commissioner Caroline D. Pham: "I want to draw attention to a bigger issue relating to capital for the coming year. The broad impacts of the Basel III Endgame are being widely reported and discussed, including impact to CFTC swap dealers and major swap participants. I am deeply concerned about this issue for our markets, which is why I expect that under my sponsorship, the Global Markets Advisory Committee (GMAC) will work on offering actionable recommendations for the Commission in this area."

- "I support this rule because codifying well-tailored relief helps provide market certainty while avoiding imposing unnecessary burdens and creating compliance complications. I also support this rule because the Commission does so while also continuing to respect the differences between our rules and those of the other regulators overseeing swap dealers on capital."