Hester Peirce: "As burdensome as it would have been for the Commission and commenters to formally re-engage, the consequences of getting this rule wrong loom large enough to warrant one more round of comment. Accordingly, I dissent."

Source: https://www.sec.gov/news/statement/peirce-statement-securitizations-112723

Although not covering as many eras as this year’s most watched concert tour,[1] this rulemaking comes close. Like its musical counterpart, a rule that is more than a decade and multiple iterations in the making should be really good.[2] This rule, with its lingering ambiguities and over-breadth, may not be. It certainly is better than what we proposed, but it is also different enough from the proposal that public comment on the new approach is necessary to ensure that we got it right this time. Even a short comment period on the new rule text would have helped to ensure that the rule prohibits securitization participants from betting against securitizations without stopping risk mitigating hedging, market-making, and other ordinary course transactions. As burdensome as it would have been for the Commission and commenters to formally re-engage, the consequences of getting this rule wrong loom large enough to warrant one more round of comment.[3] Accordingly, I dissent.

Re-proposing this rule would have counteracted a troubling recent pattern from the Commission:[4]

release an expansive, unworkable rule proposal that includes myriad questions;

watch as concerned commenters expend available resources to mount an all-out attack on the most unrealistic and potentially catastrophic provisions in the proposed rule, leaving them with little to no remaining resources to address questions about other, less immediately alarming, yet also concerning provisions in the proposed rule;

trim the rule’s unworkable excesses when finalizing the rule after the comment period has closed; and

cite to the proposal’s myriad questions – both answered and unanswered – to support the contention that the rule is responsive to commenters and a logical outgrowth of the proposal.

Our pattern of proposing unrealistic rules with numerous questions, only to substantively revise the rule text after the comment period closes inhibits our ability to receive and consider comprehensive feedback, and thus write sound final rules. We faced this problem here.[5] Commenters pointed out the rule’s overbreadth and unworkability.[6] The adopting release, recognizing the potential for certain elements of the rule to disrupt the securitization market and the multi-trillion dollar credit market that relies on it,[7] seeks to address some of these elements. I nevertheless continue to have concerns that we have not gotten the substance of the rule right. By “right,” I mean implementing the congressional mandate in a way that stops the types of conflicted transactions that plagued financial crisis era securitizations without placing undue burdens on ordinary course transactions.

Unfortunately, I continue to be concerned that we did not get this right. The rule continues to be broader than necessary. The rule covers, for example, transactions that do not result in the securitization participant’s interests being materially adverse to investors’ interests.[8] The rule instead deems conflicted transactions “with respect to which there is a substantial likelihood that a reasonable investor would consider the transaction important to the investor’s investment decision.”[9] The rule excepts certain activities, but those exceptions are excessively narrow.[10] More generally, the Commission fails to use its exemptive authority to exclude from the rule securitizations for which exemptions might make sense.[11] The excesses in the market which drove the passage of Section 621 of Dodd-Frank are arguably no longer prevalent, so the rule should have been more targeted.[12]

The rule remains ambiguous in certain places. As one example, the starting date of the prohibition begins on the potentially ambiguous date the person agrees to become a securitization participant, which is triggered by “an agreement in principle,” a vague standard which can include “oral agreements and facts and circumstances constituting an agreement.”[13] As another example, the Commission declined to define in the regulatory text the key term “synthetic asset-backed security.”[14] The Commission acknowledges that leaving this ambiguity unaddressed could “impose compliance costs on securitization participants who may seek legal advice and incur other costs” to see if they must comply with the final rule and that the uncertainty could deter the participants “from entering [certain] transactions” at all.[15]

Even as I dissent, I commend the staff’s serious efforts to address problems raised by commenters. The staff’s intense work on a technically difficult topic paid off in the form of a better rule than was proposed. Helpful changes include excluding long investors, narrowing some of the defined terms, clarifying that the rule does not apply to mortgage insurance linked-notes, and striking the proposed carve-out for Fannie Mae and Freddie Mac during conservatorship. I appreciate the work of the team in the Division of Corporation Finance under the capable and engaged leadership of Erik Gerding and Rolaine Bancroft. I also thank the staff in the Division of Economic and Risk Analysis, the Division of Trading and Markets, the Office of General Counsel, Corey Klemmer in the Chair’s office, and others throughout the Commission for their efforts on this multi-year rulemaking. I look forward to working with staff and affected market participants on implementing the rule..

What Hester is mad about:

Fact Sheet:

Press Release:

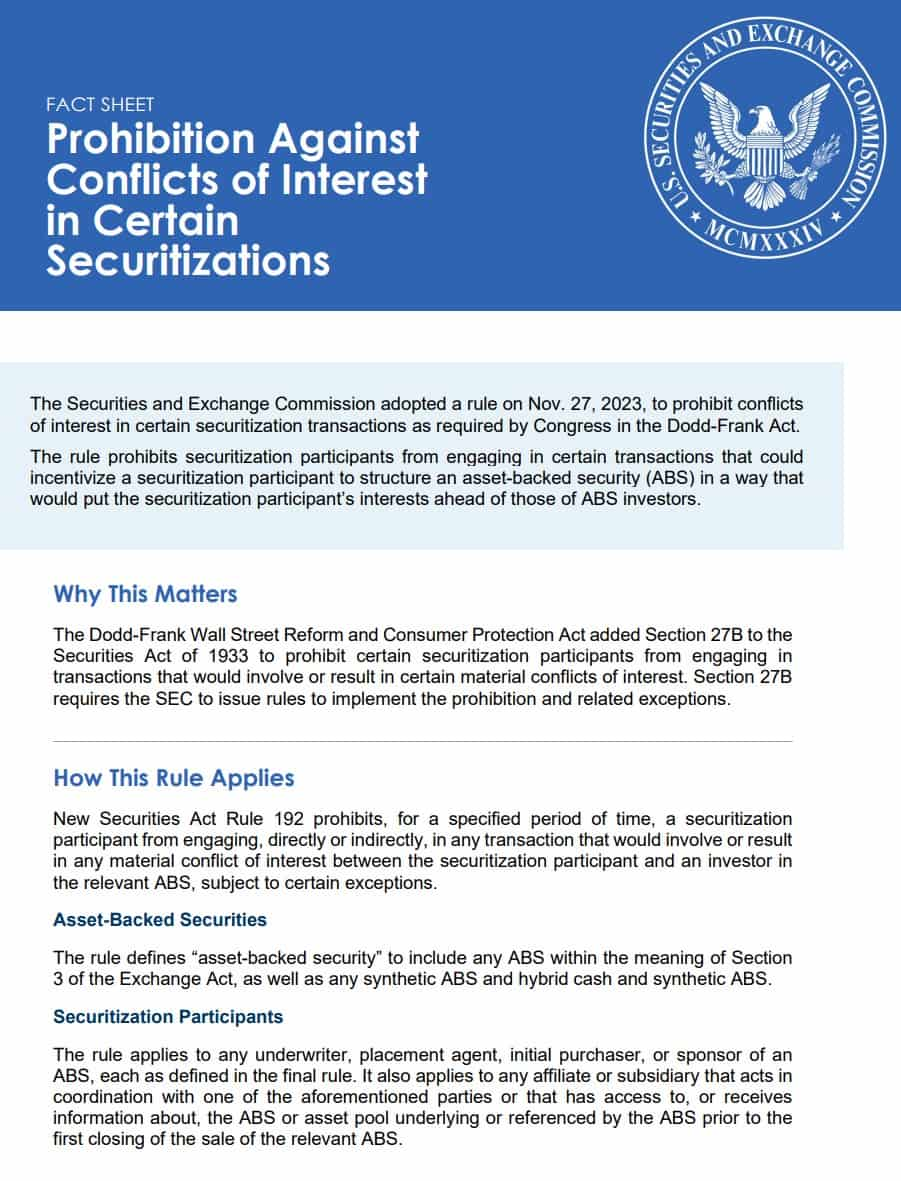

The Securities and Exchange Commission today adopted Securities Act Rule 192 to implement Section 27B of the Securities Act of 1933, a provision added by Section 621 of the Dodd-Frank Act. The rule is intended to prevent the sale of asset-backed securities (ABS) that are tainted by material conflicts of interest. It prohibits a securitization participant, for a specified period of time, from engaging, directly or indirectly, in any transaction that would involve or result in any material conflict of interest between the securitization participant and an investor in the relevant ABS. Under new Rule 192, such transactions would be “conflicted transactions.”

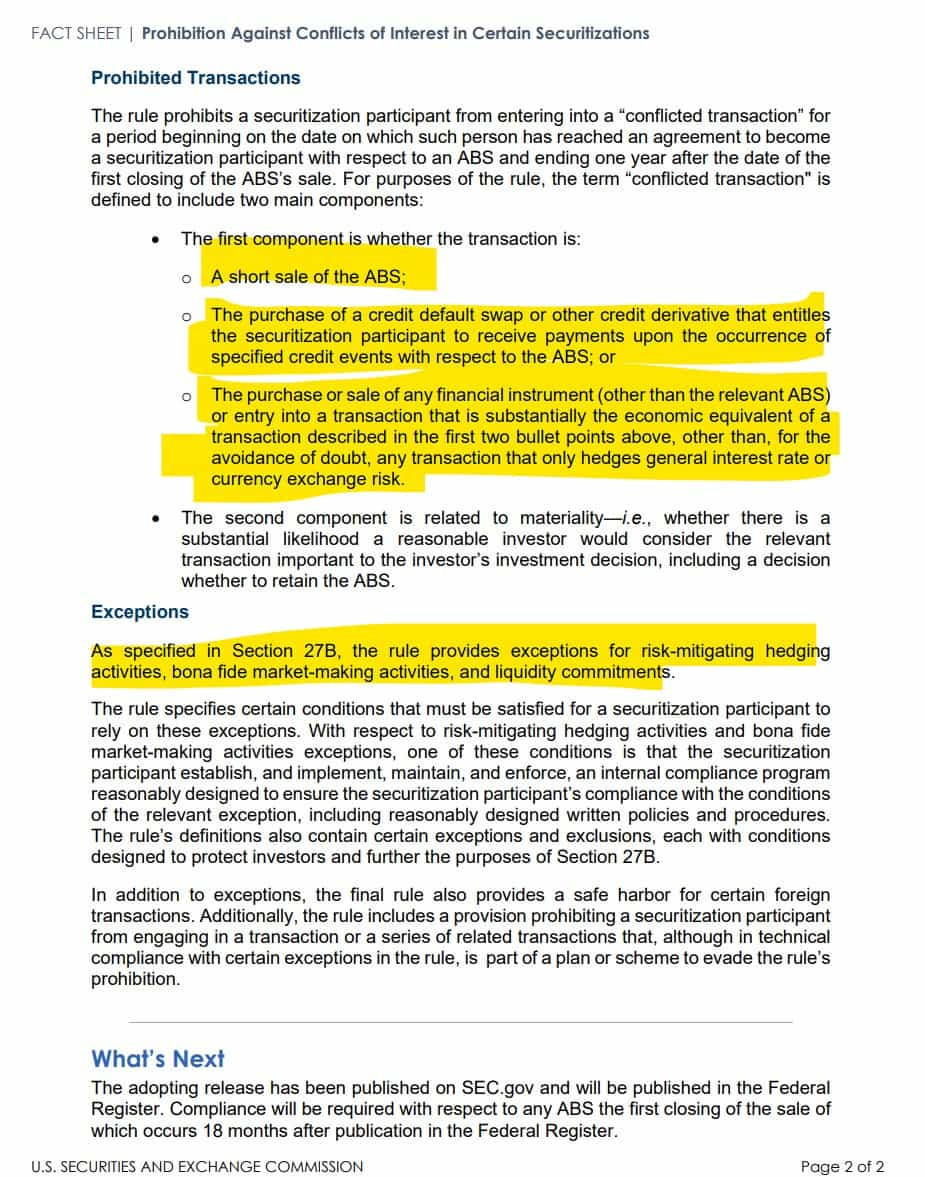

Consistent with the statute, Rule 192 provides exceptions for risk-mitigating hedging activities, liquidity commitments, and bona fide market-making activities of a securitization participant. These exceptions permit certain market activities, subject to satisfaction of the specified conditions, which will allow securitization participants to continue important risk management, liquidity commitment, and market-making activities.

“I am pleased to support this rule as it fulfills Congress’s mandate to address conflicts of interests in the securitization market, a market which was at the center of the 2008 financial crisis,” said SEC Chair Gary Gensler. “As directed by Congress, today’s rule prohibits securitization participants — including those who sell or facilitate the sale of an asset-backed security — from engaging in transactions that involve or result in any material conflict of interest with investors in that ABS. Further, as required by Section 621 of the Dodd-Frank Act, the final rule provides exceptions for risk-mitigating hedging activities, bona fide market making, and certain liquidity commitments. Such a rule benefits investors and issuers alike."

Under new Rule 192, conflicted transactions include a short sale of the relevant ABS, the purchase of a credit default swap or other credit derivative that entitles the securitization participant to receive payments upon the occurrence of specified credit events in respect of the ABS, or a transaction that is substantially the economic equivalent of the aforementioned transactions, other than any transaction that only hedges general interest rate or currency exchange risk.

The adopting release is published on SEC.gov and will be published in the Federal Register. Rule 192 will become effective 60 days after publication in the Federal Register. Compliance with Rule 192 will be required with respect to any ABS the first closing of the sale of which occurs 18 months after the date of publication in the Federal Register.

TLDRS:

- SEC Adopts Rule to Prohibit Conflicts of Interest in Certain Securitizations.

- Hester Peirce on SEC banning conflicts in Asset-Backed Securitizations: "As burdensome as it would have been for the Commission and commenters to formally re-engage, the consequences of getting this rule wrong loom large enough to warrant one more round of comment. Accordingly, I dissent."

What she is upset about:

- This rule aims to prevent material conflicts of interest in the sale of asset-backed securities (ABS).

- It prohibits securitization participants from engaging in transactions that could result in a material conflict of interest with ABS investors for a specified period.

- The rule defines a "conflicted transaction" as one that involves a short sale of the ABS, the purchase of a credit derivative linked to the ABS, or a transaction economically equivalent to these, excluding those that only hedge general interest rate or currency risks.

- The transaction also must be considered materially important by a reasonable investor.

- The rule allows exceptions for risk-mitigating hedging activities, liquidity commitments, and bona fide market-making activities, subject to certain conditions.

- The rule will be effective 60 days after publication in the Federal Register, with compliance required for any ABS whose first sale closing occurs 18 months after this publication.