FINRA October 2022 disciplinary report: 'between August 2017 and May 2019, Morgan Stanley reported approximately 9.6 million transactions in National Market System (NMS) securities without a required short sale indicator.' Discipline? $250,000 fine.

Good morning r/Superstonk, I hope everyone's day is off to a great start. FINRA released its Disciplinary and Other FINRA Actions reported for October 2022.

If you find this 'discipline' to be 'light', please consider dropping by https://www.reddit.com/r/Superstonk/comments/y2an0w/sec_reopens_comments_for_several_rulemaking/ to learn how you can make sure your voice is heard.

FINRA has taken disciplinary actions against the following firms:Morgan Stanley & Co. LLC

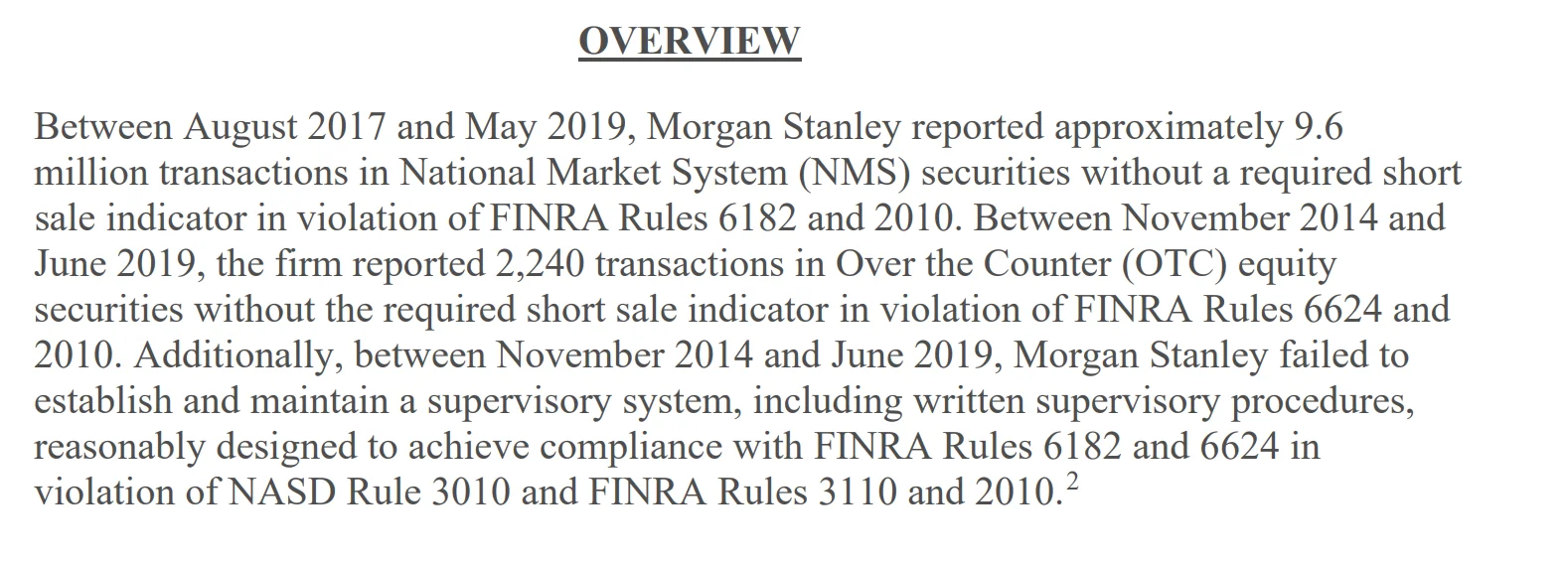

Between August 2017 and May 2019, Morgan Stanley reported approximately 9.6 million transactions in National Market System (NMS) securities without a required short sale indicator. Discipline? $250,000 fine without admitting or denying the findings:

Morgan Stanley & Co. LLC (CRD #8209, New York, New York) August 17, 2022 – An AWC was issued in which the firm was censured and fined $250,000. Without admitting or denying the findings, the firm consented to the sanctions and to the entry of findings that it failed to report the short sale indicator for transactions in National Market System (NMS) securities.

The findings stated that a programming error caused the firm to exclude the short sale indicator when reporting short sale transactions to the New York Stock Exchange (NYSE) Trade Reporting Facility (TRF). The firm learned of the issue in connection with FINRA’s cycle exam and subsequently corrected the programming error. The findings also stated that the firm failed to report the short sale indicator for transactions in OTC equity securities. A similar programming error caused the firm to erroneously exclude the short sale indicator when reporting short sale transactions to the OTC TRF.

The programming error has since been corrected. The findings also included that the firm failed to reasonably supervise trade reporting to the NYSE and OTC TRFs. The firm conducted supervisory reviews of equity trade reporting, but they were not reasonably designed to achieve compliance with FINRA rules with respect to short sale indicator reporting to the NYSE and OTC TRFs. When the firm began reporting to the NYSE and OTC TRF, it reviewed certain test trades, but those reviews did not detect the absence of the short sale indicator. The firm did not conduct any subsequent reviews to determine if the firm was reporting the accurate short sale indicator to the NYSE and OTC TRFs.

Gar Wood Securities, LLC

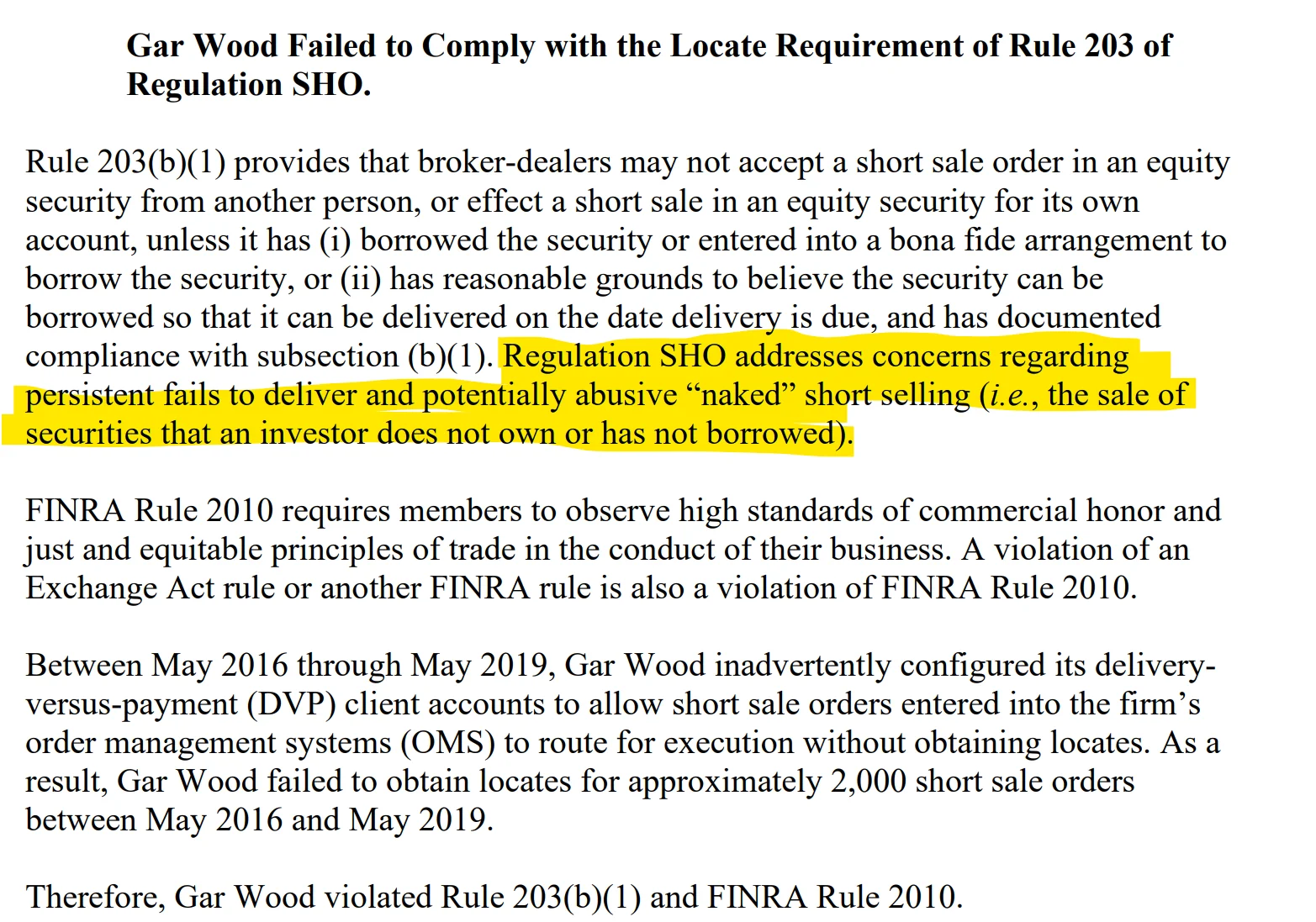

Violated Rule 203(b)(1) by accepting approximately 2,000 short sale orders without obtaining locates between May 2016 and May 2019. Discipline? Fined $100,000 without admitting or denying the findings:

Gar Wood Securities, LLC (CRD #138033, Naperville, Illinois) August 18, 2022 – An AWC was issued in which the firm was censured and fined $100,000. Without admitting or denying the findings, the firm consented to the sanctions and to the entry of findings that it failed to comply with the locate requirement of Rule 203 of Regulation SHO of the Exchange Act. The findings stated that the firm inadvertently configured its delivery-versus-payment (DVP) client accounts to allow short sale orders entered into the firm’s order management systems (OMS) to route for execution without obtaining locates. As a result, the firm failed to obtain locates for short sale orders. The findings also stated that the firm failed to accurately report the capacity symbol for trades.

One of the firm’s OMSs was incorrectly coded to send a principal capacity symbol for client agency orders to the reporting party. As a result, the firm caused transactions to be reported to the FINRA TRF with the incorrect capacity. Subsequently, the firm switched all agency order routing to an OMS that was correctly coded to report the proper capacity symbol. The findings also included that the firm failed to reasonably supervise for compliance with locate and trade reporting requirements. The firm’s supervisory system, including its WSPs, was not reasonably designed to achieve compliance with Rule 203(b) of Regulation SHO.

The firm’s supervisory system required that a review for locate information be performed but it inadvertently failed to include a locate review for short sale orders in the firm’s DVP accounts. Further, the firm conducted a locates supervisory review for custodial accounts, but it incorrectly excluded short sales orders that were accepted for execution but did not execute. In addition, the firm lacked a review to confirm all required trade information, such as capacity, was accurately reported to the FINRA TRF.

SG Americas Securities

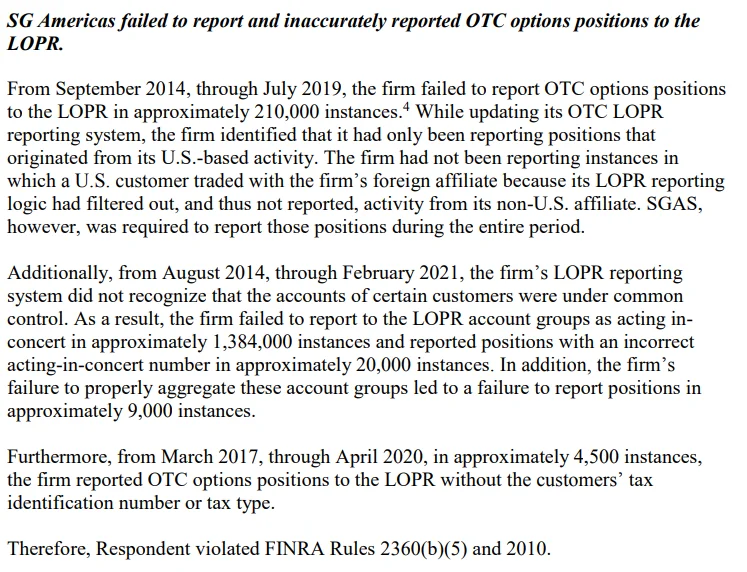

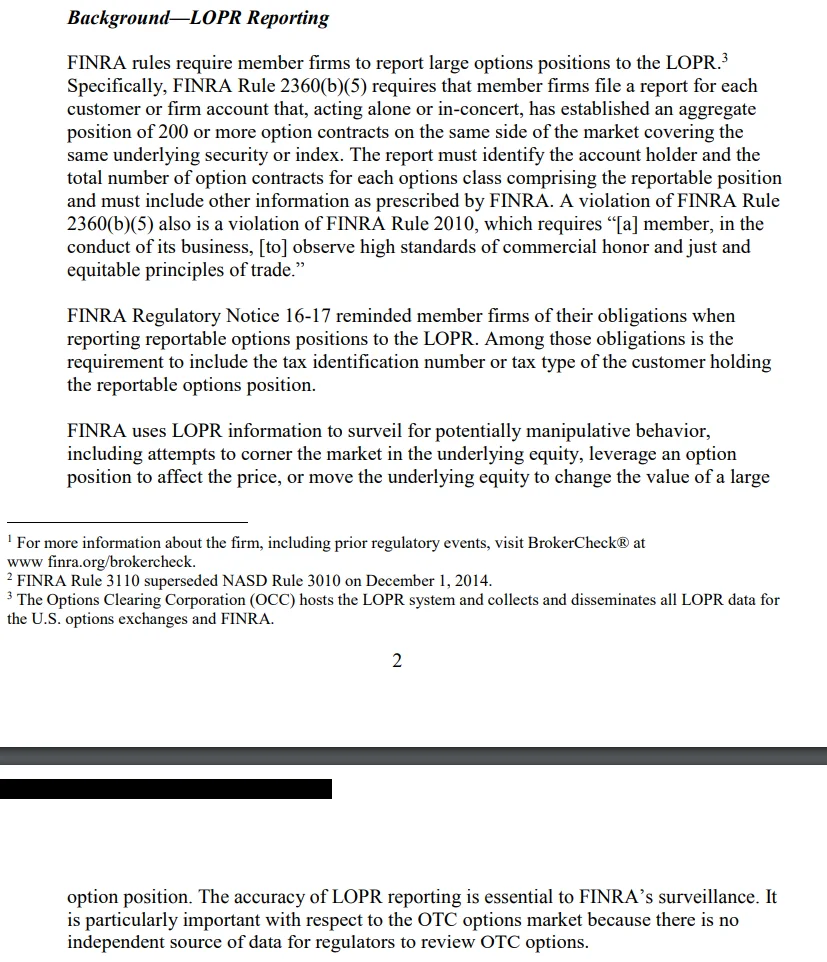

Failed to report and inaccurately reported OTC options positions to the LOPR. Discipline? Censured and fined $325,000. Without admitting or denying the findings.

SG Americas Securities, LLC (CRD #128351, New York, New York) August 10, 2022 – An AWC was issued in which the firm was censured and fined $325,000. Without admitting or denying the findings, the firm consented to the sanctions and to the entry of findings that it failed to report and inaccurately reported over-the-counter (OTC) options positions to the large options positions reporting system (LOPR). The findings stated that while updating its OTC LOPR, the firm identified that it had only been reporting positions that originated from its U.S.- based activity.

The firm had not been reporting instances in which a U.S. customer traded with the firm’s foreign affiliate because its LOPR reporting logic had filtered out, and thus not reported, activity from its non-U.S. affiliate. However, the firm was required to report those positions. The firm’s LOPR also did not recognize that certain customers’ accounts were under common control. As a result, the firm failed to report to the LOPR account groups as acting in-concert and reported positions with an incorrect acting-in-concert number. In addition, the firm’s failure to properly aggregate these account groups led to a failure to report positions. Furthermore, the firm reported OTC options positions to the LOPR without the customers’ tax identification number or tax type. The findings also stated that the firm failed to establish and maintain a supervisory system reasonably designed to comply with its LOPR reporting obligations.

The firm’s supervisory system related to LOPR reporting did not provide for, and the firm did not conduct, a review of its LOPR reporting logic to determine whether its system captured all reportable positions, including those transactions between U.S. customers and a foreign affiliate of the firm that the firm incorrectly excluded from its LOPR reports. Later, the firm removed the filter that prevented it from including reportable positions involving foreign affiliates and also implemented additional controls and reviews designed to identify potential issues with its LOPR reporting. In addition, the firm’s supervisory system for detecting accounts that were acting in-concert was too restrictive to be effective, because it only linked its acting-in-concert accounts that shared an internal legal entity number or were identified in the system as having the same fund manager. The firm has since implemented changes to its system to more precisely identify accounts required to be designated as acting-in-concert.

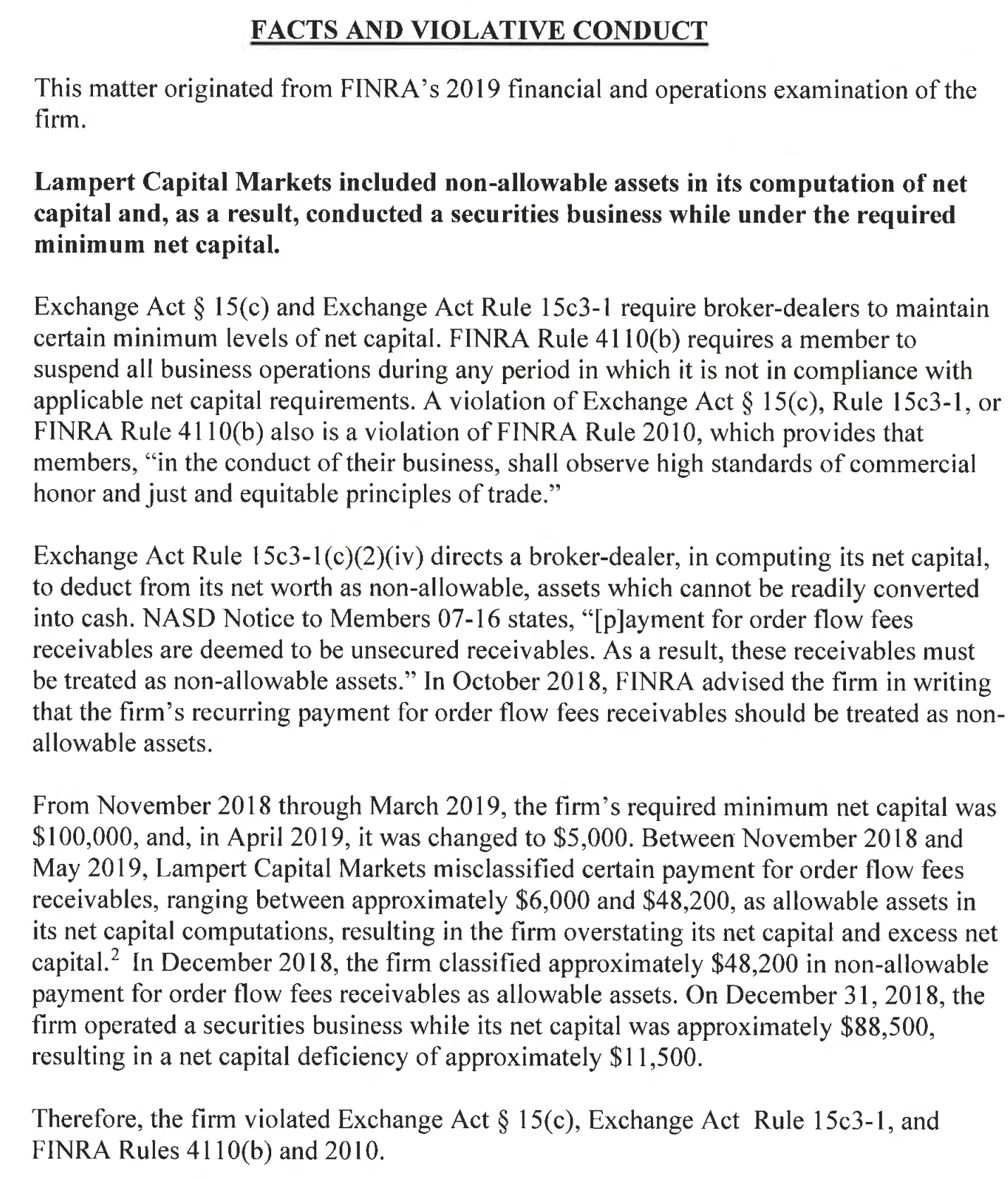

Lampert Capital Markets

Highlights PFOF dangers: 'misclassifying PFOF receivables as allowable assets, the firm overstated its allowable receivables, and overstated its net capital and excess net capital on reports.'

Lampert Capital Markets Inc. (CRD #103725, New York, New York) August 29, 2022 – An AWC was issued in which the firm was censured and fined $10,000. Without admitting or denying the findings, the firm consented to the sanctions and to the entry of findings that it conducted a securities business while under its required minimum net capital by including non-allowable assets in its computation of net capital.

The findings stated that the firm misclassified certain payment for order flow fees receivables, ranging between approximately $6,000 and $48,200, as allowable assets in its net capital computations, resulting in the firm overstating its net capital and excess net capital. The firm classified approximately $48,200 in non-allowable payment for order flow fees receivables as allowable assets. Subsequently, the firm operated a securities business while its net capital was approximately $88,500, resulting in a net capital deficiency of approximately $11,500. The findings also stated that the firm failed to make and keep accurate books and records.

As a consequence of misclassifying payment for order flow fees receivables as allowable assets, the firm overstated its allowable receivables, and overstated its net capital and excess net capital on six month-end FOCUS reports. The findings also included that the firm failed to file required notices. When its net capital was below its minimum requirement, the firm did not file a notice with FINRA or the SEC. In addition, the firm’s net capital fell below 120 percent of its required minimum net capital, but the firm did not file the required notices.