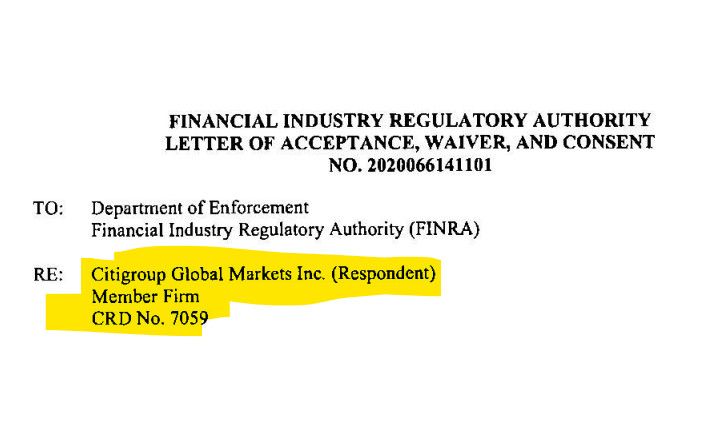

FINRA 'discipline' Alert! Between November 2017 and August 2022, Citigroup violated the "Short Tender Rule". Penalty? Censure, $2.5M fine, no admission of wrongdoing.

Hello and happy Tuesday, I hope everyone is off to a great start of the week!

I would like to share some more FINRA 'discipline' with y'all, this time it's Citigroup again!

As these releases convey a ton of information, I hope this format makes sense:

- I am going to outline what Citigroup did from points from the filing.

- I am going to pull the rules they broke and attempt to provide wut mean definitions while breaking each section against Citigroup down a bit further.

- I will talk about the penalty levied.

- I will discuss how the nefarious behavior could impact GameStop.

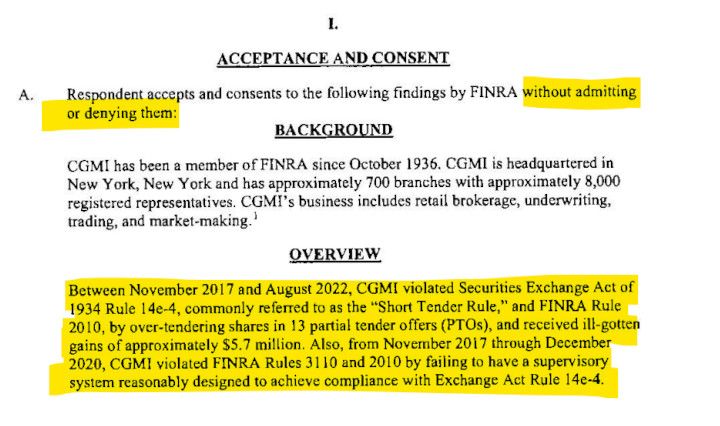

What Citigroup did (without admitting or denying):

Wut Mean?

- Between November 2017 and August 2022, CGMI violated Securities Exchange Act of 1934 Rule l 4e-4, commonly referred to as the "Short Tender Rule," and FINRA Rule 2010, by overtendering shares in 13 partial tender offers (PTOs), and received illgotten gains of approximately $5.7 million.

- Also, from November 2017 through December 2020, CGMI violated FINRA Rules 3110 and 2010 by failing to have a supervisory system reasonably designed to achieve compliance with Exchange Act Rule 14e-4.

- Short Tender Rule (Rule 14e-4): This is like promising more cookies than you have in your lunchbox. The rule says this is not allowed because it’s not fair to the other kids who are trading.

- Partial Tender Offers (PTOs): This is like a situation where a kid (company) offers to trade some, but not all, of their cookies for something else. The way they decide how many cookies to trade with each kid is like drawing names from a hat (by lot) or sharing equally (pro rata).

- Over-tendering: This is like a player taking more cookies. Citigroup did this 13 times and gained $5.7 million unfairly.

- FINRA Rules 3110 and 2010: These are other rules in the game. Rule 2010 is about playing fairly and nicely. Rule 3110 is like having a coach (supervisory system) who makes sure the players (companies) follow the rules.

- Violating FINRA Rules 3110 and 2010: CGMI didn’t have a good enough coach (supervisory system) to make sure they were following the Short Tender Rule from November 2017 to December 2020.

FACTS AND VIOLATIVE CONDUCT:

Wut Mean?

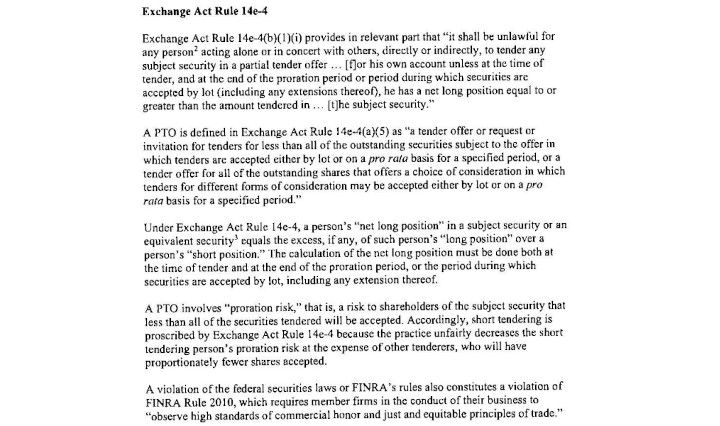

- Exchange Act Rule 14e-4(b)(1)(i): This rule is like saying, if you want to trade your cookies (securities) during lunch, you have to actually have cookies to trade. You can’t promise more cookies than you have in your lunchbox.

- Partial Tender Offer (PTO): This is like a situation where a kid (company) offers to trade some, but not all, of their cookies for something else. The way they decide how many cookies to trade with each kid is like drawing names from a hat (by lot) or sharing equally (pro rata).

- Net Long Position: This is like counting how many cookies you actually have in your lunchbox, minus any you’ve promised to others. You need to count your cookies when you offer them and again when you’re actually trading to make sure you still have enough.

- Proration Risk: This is the chance that not everyone will get to trade cookies because there aren’t enough to go around. If someone promises more cookies than they have, it’s not fair because it means other kids might get fewer cookies.

- Short Tendering: This is like promising more cookies than you have in your lunchbox. The rule says this is not allowed because it’s not fair to the other kids who are trading.

- FINRA Rule 2010: This is a rule that says everyone has to trade fairly and nicely during lunch. If you break this rule, or any other trading rule, you’re in trouble.

CGMI Violated Exchange Act Rule 14e-4:

Wut Mean?

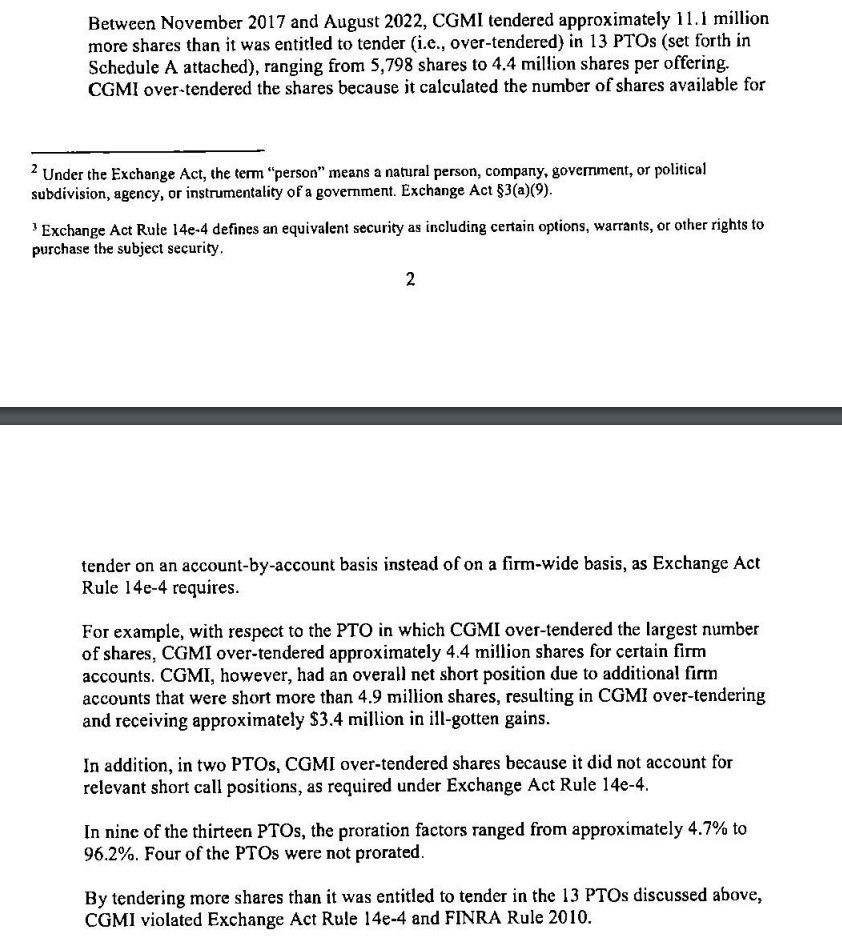

- Citigroup and Cookies (Shares): Citigroup is like a kid in school who has a bunch of cookies (shares) to trade with other kids. Between November 2017 and August 2022, Citigroup traded about 11.1 million more cookies than they were supposed to in 13 different trading sessions (PTOs).

- Counting Cookies Wrongly: Citigroup was supposed to count all their cookies together before trading (firm-wide basis), but they counted them separately (account-by-account basis). This is like counting cookies in each packs separately and forgetting that all the packs are part of the same package of cookies!

- Biggest Mistake: In one trading session, Citigroup traded about 4.4 million more stickers than they had. They forgot that they had already promised 4.9 million cookies to other kids, so they ended up getting $3.4 million in extra trades (ill-gotten gains) that they weren’t supposed to get.

- Other Mistakes: In two trading sessions, Citigroup forgot to consider some promised trades (short call positions) when counting their cookies. In nine trading sessions, the number of cookies each kid could trade varied a lot (proration factors ranged from 4.7% to 96.2%). Four trading sessions didn’t have this variation (were not prorated).

- Breaking Rules: By trading more cookies than they were supposed to, CGMI broke the school rules (Exchange Act Rule 14e-4) and the general rule of playing fair and nice (FINRA Rule 2010).

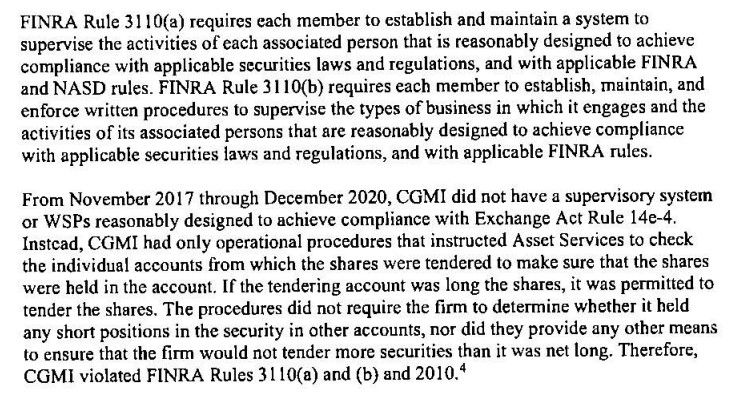

CGMI did not have a supervisory system reasonably designed for achieving compliance with Exchange Act Rule 14e-4:

Wut Mean?

- FINRA Rule 3110(a) & (b): These rules are like the school’s guidelines for students. They say that each student (member) must have a system and written rules (procedures) to watch over their cookie trading and to make sure everyone is trading cookies fairly according to the school and classroom rules (securities laws and regulations, and FINRA and NASO rules).

- Citigroup's Mistake: From November 2017 to December 2020, Citigroup was like a student who didn’t have a good system or clear written rules to make sure they were trading fairly according to one specific school rule (Exchange Act Rule 14e-4).

- What Citigroup Did: Citigroup only had basic rules that told the students to check their own cookie collections (individual accounts) before trading. If a student had enough cookies (was long the shares), they were allowed to trade. But, Citigroup's rules didn’t make sure the students checked if they had promised cookies to others (held any short positions) in different collections (other accounts).

- Result: Because Citigroup didn’t have a good system or clear rules to make sure everyone was trading fairly, they broke the school’s guidelines (violated FINRA Rules 3110(a) and (b)) and the general rule of playing fair and nice (FINRA Rule 2010).

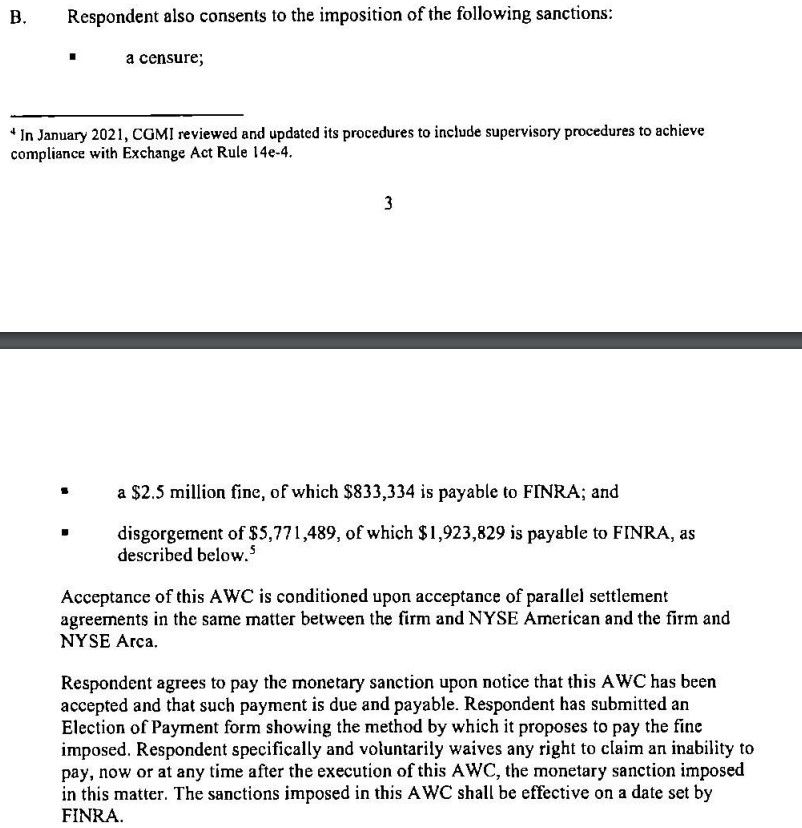

Penalty?

How could this impact GameStop?

Citigroup over-tendered shares, meaning they offered more shares than they actually had in certain deals.

- Market Integrity: Actions like over-tendering can shake your trust in the market’s fairness and transparency. If firms can misrepresent share ownership, it might make you wonder about the prevalence of other manipulative practices like naked shorting...

- Stock Price: Abusive practices can artificially affect a stock’s supply and demand, potentially leading to price distortions.

TLDRS:

- Between November 2017 and August 2022, CGMI violated Securities Exchange Act of 1934 Rule l 4e-4, commonly referred to as the "Short Tender Rule," and FINRA Rule 2010, by overtendering shares in 13 partial tender offers (PTOs), and received ill-gotten gains of approximately $5.7 million.

- Also, from November 2017 through December 2020, CGMI violated FINRA Rules 3110 and 2010 by failing to have a supervisory system reasonably designed to achieve compliance with Exchange Act Rule 14e-4.

- Penalty? Without admitting or denying anything, a censure, and $2.5 million fine...

- disgorgement of $5,771,489, of which $1,923,829 is payable to FlNRA.